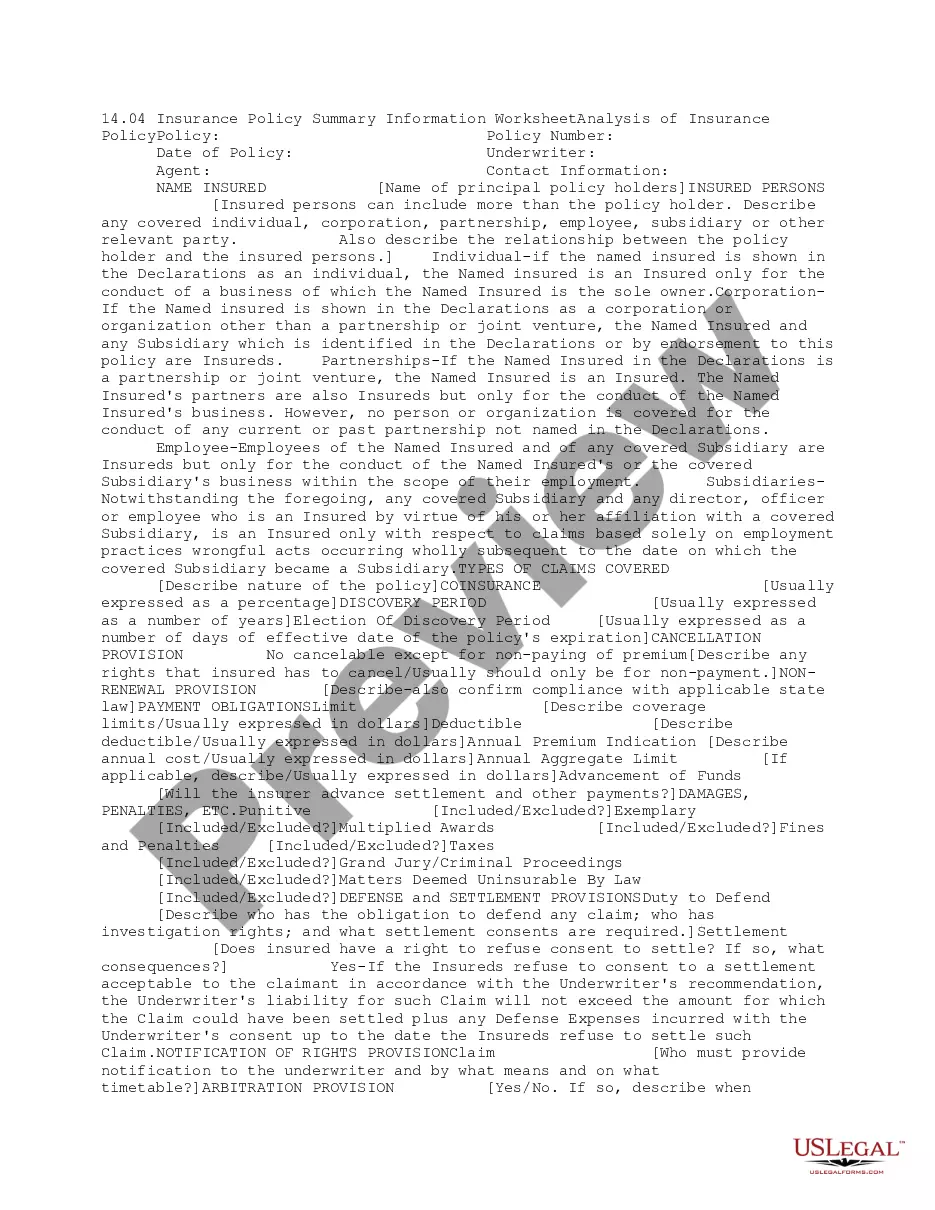

This due diligence form is a summary of insurance coverage analysis for directors and officers in a company.

North Carolina Executive Summary Director and Officer Insurance Coverage Analysis

Category:

State:

Multi-State

Control #:

US-DD01409

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out Executive Summary Director And Officer Insurance Coverage Analysis?

You can spend time online attempting to locate the authentic document template that meets the state and federal requirements you need.

US Legal Forms offers thousands of authentic forms that can be evaluated by professionals.

You are able to download or print the North Carolina Executive Summary Director and Officer Insurance Coverage Analysis from our service.

If available, utilize the Review option to preview the document template as well.

- If you already have a US Legal Forms account, you can Log In and then click the Obtain option.

- Subsequently, you can complete, modify, print, or sign the North Carolina Executive Summary Director and Officer Insurance Coverage Analysis.

- Every authentic document template you purchase is yours indefinitely.

- To obtain another copy of any purchased form, proceed to the My documents tab and click on the relevant option.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for your county/city of choice.

- Review the form details to make certain you have chosen the right one.

Form popularity

FAQ

D&O policies include an exclusion for losses related to criminal or deliberately fraudulent activities. Additionally, if an individual insured receives illegal profits or remuneration to which they were not legally entitled, they will not be covered if a lawsuit is brought forward due to this.

Directors & Officers (D&O) Liability insurance is designed to protect the people who serve as directors or officers of a company from personal losses if they are sued by the organization's employees, vendors, customers or other parties.

Directors & Officers (D&O) Liability insurance is designed to protect the people who serve as directors or officers of a company from personal losses if they are sued by the organization's employees, vendors, customers or other parties.

D&O insurance specifically covers members on a board of directors and officers. Professional liability insurance, on the other hand, covers professionals (of nearly any position within a company) that offer specialized services.

Key Takeaways. Directors and officers (D&O) liability insurance covers directors and officers or their company or organization if sued (most policies exclude fraud and criminal offenses). D&O insurance claims are paid to cover losses associated with the lawsuit, including legal defense fees.

Directors and officers (D&O) liability insurance protects the personal assets of corporate directors and officers, and their spouses, in the event they are personally sued by employees, vendors, competitors, investors, customers, or other parties, for actual or alleged wrongful acts in managing a company.

Directors and officers (D&O) liability insurance protects the personal assets of corporate directors and officers, and their spouses, in the event they are personally sued by employees, vendors, competitors, investors, customers, or other parties, for actual or alleged wrongful acts in managing a company.

Directors and Officers InsuranceD&O is there to protect high-level decision makers when someone asserts they were negligent in their duties as an officer or board member. E&O, on the other hand, covers acts, errors, and omissions committed by employees of the company.

Malpractice insurance is another name for professional liability insurance for legal or medical professionals. No matter what it's called, professional liability policies offer coverage if you make a mistake in your professional service. If a client sues you, these coverages will help pay for your legal defense.

The main difference between both insurance policies is that the first is designed to financially help senior executives in the event their company is subject to legal costs resulting from a lawsuit, while the latter protects mistakes made by a business, negatively impacting its clients.