North Carolina Installments Fixed Rate Promissory Note Secured by Personal Property

Understanding this form

The North Carolina Installments Fixed Rate Promissory Note Secured by Personal Property is a legal document whereby a borrower pledges personal property as security for a loan. This form outlines the borrower's promise to repay the loan amount, including interest, in fixed installments. It differs from unsecured promissory notes, as the lender has a legal claim on the personal property should the borrower default on the loan.

Main sections of this form

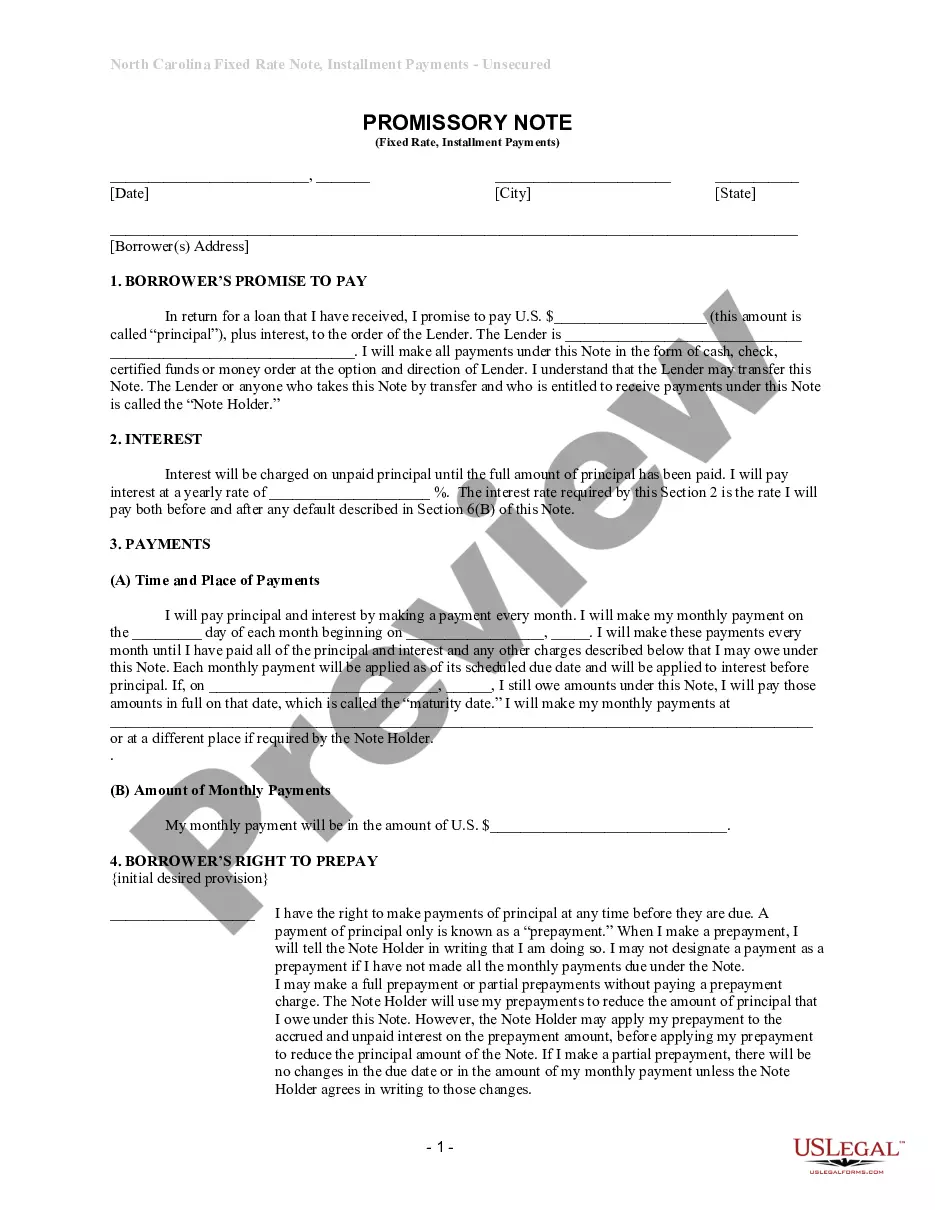

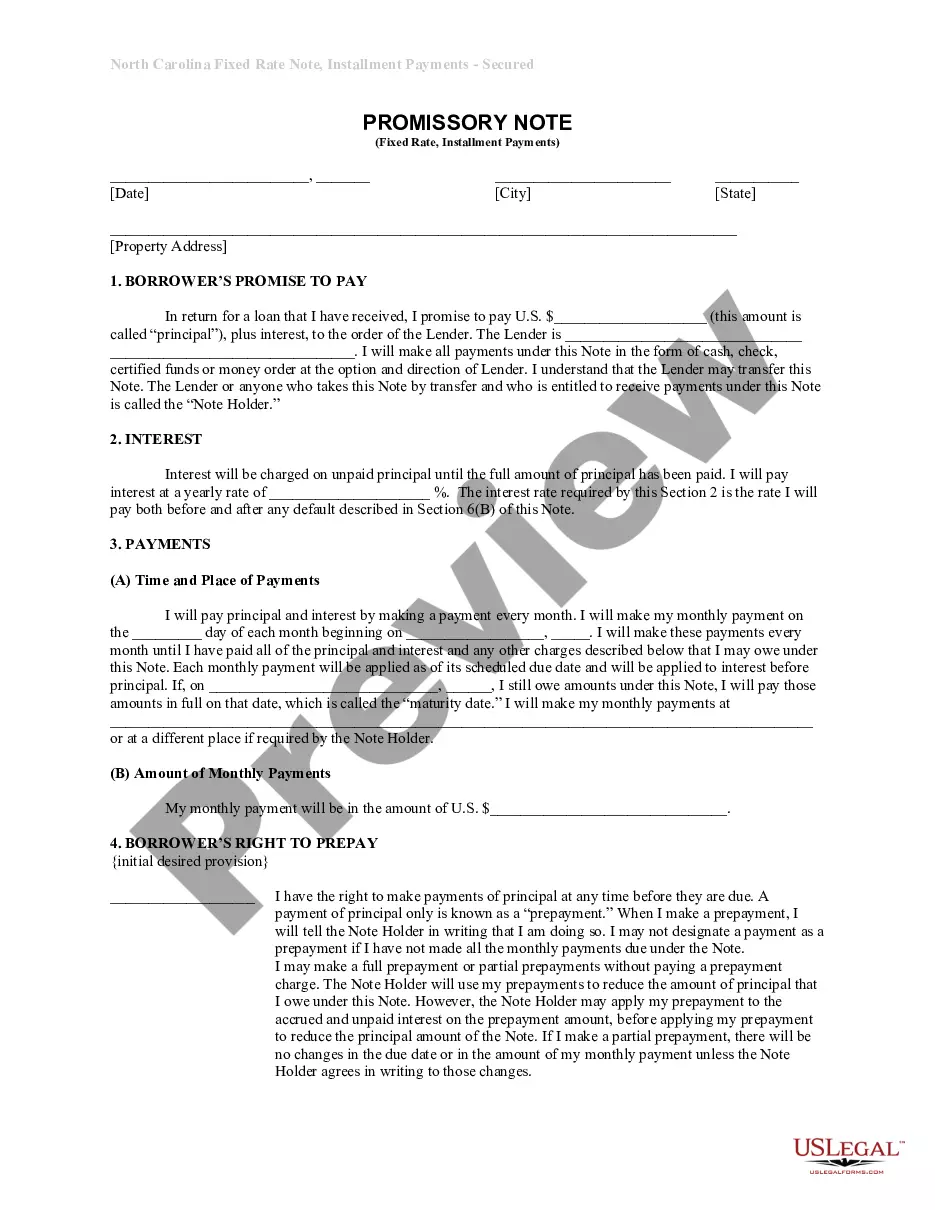

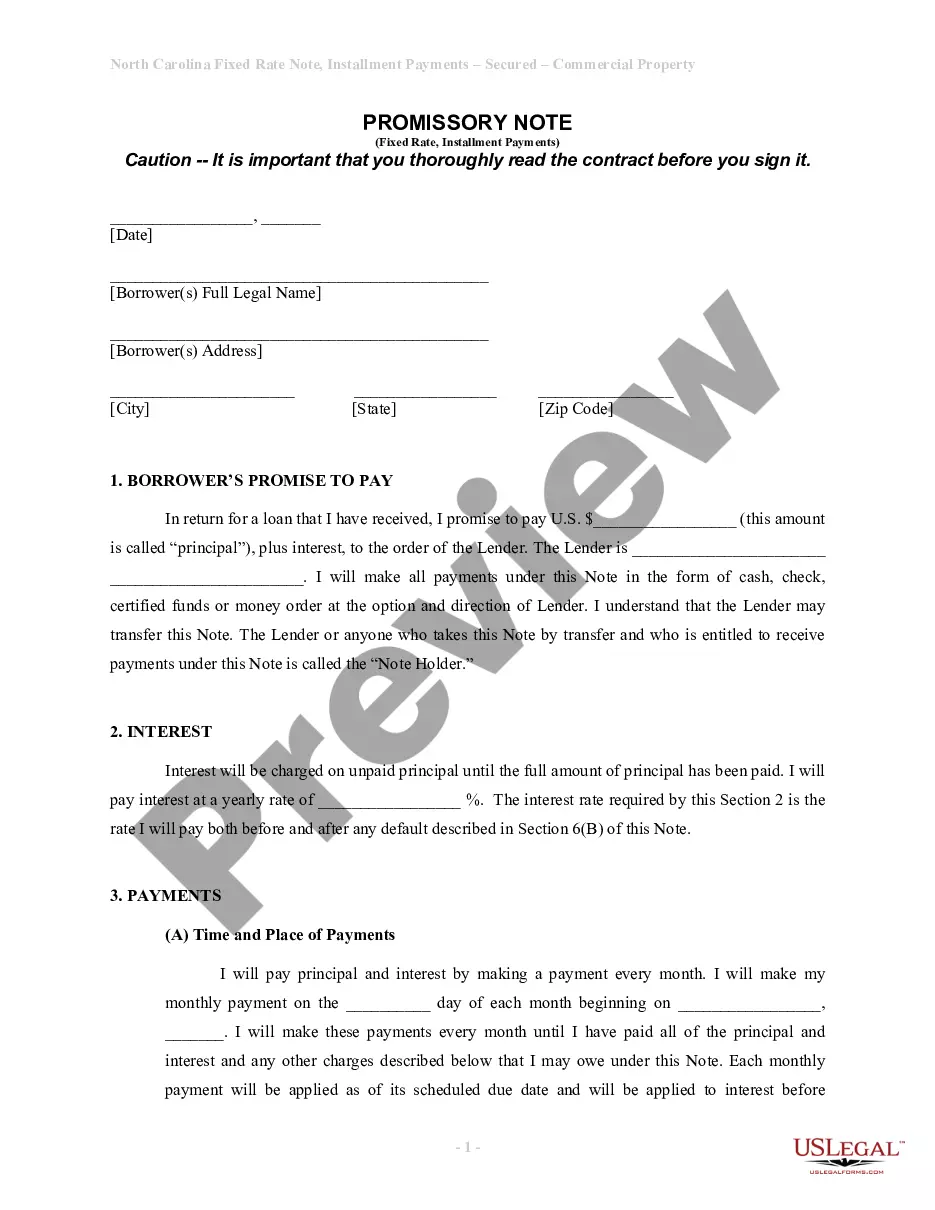

- Borrower's promise to pay the principal amount and interest.

- Details on the interest rate and how it is calculated.

- Payment schedule, including monthly payment amounts and due dates.

- Borrower's right to prepay the loan, with or without penalties.

- Consequences of late payments and default.

- Details regarding the secured personal property.

Common use cases

This form should be used when an individual or entity intends to borrow money and is willing to offer personal property as collateral. It is suitable for various situations, such as personal loans, small business financing, or any agreement where the lender requires a guarantee against the borrower's repayment obligations.

Who should use this form

- Borrowers seeking to secure a loan using personal property.

- Lenders looking to formalize a loan agreement with secured collateral.

- Individuals or entities needing clarity on loan repayment terms.

- People with limited experience in legal agreements who want a straightforward, reliable document.

How to prepare this document

- Identify the parties involved: the borrower and the lender.

- Enter the loan amount as the principal to be repaid.

- Specify the interest rate and the schedule for monthly payments.

- Clearly describe the personal property being used as collateral.

- Sign and date the document in the presence of a witness if required.

Does this form need to be notarized?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to accurately state the personal property used as security.

- Not specifying the correct monthly payment amounts or due dates.

- Omitting the interest rate or not clearly understanding how it is calculated.

- Not completing the document fully before signing.

Why complete this form online

- Convenient download and completion from anywhere.

- Edit and customize the form to fit specific lending conditions.

- Access to legal templates reviewed by licensed attorneys.

Legal use & context

- This form serves as an enforceable agreement between the borrower and lender, protecting both parties' interests.

- The collateralization of the loan helps assure the lender of repayment, reducing the risk associated with lending.

- Ensuring compliance with North Carolina laws regarding promissory notes is crucial for the document's validity and enforceability.

Summary of main points

- This promissory note is essential for documenting loans secured by personal property in North Carolina.

- Understanding the terms is crucial to avoid default and legal complications.

- This form provides both borrowers and lenders with a clear outline of obligations and rights.

Looking for another form?

Form popularity

FAQ

Date. The promissory note should include the date it was created at the top of the page. Amount. Loan terms. Interest rate. Collateral. Lender and borrower information. Signatures.

To write a promissory note for a personal loan, you will need to include the names of both parties, the principal balance, the APR, and any fees that are part of the agreement. The promissory note should also clearly explain what will happen if the borrower pays late or does not pay the loan back at all.

What Is a Promissory Note? A promissory note is a financial instrument that contains a written promise by one party (the note's issuer or maker) to pay another party (the note's payee) a definite sum of money, either on demand or at a specified future date.

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

The individual who promises to pay is the maker, and the person to whom payment is promised is called the payee or holder. If signed by the maker, a promissory note is a negotiable instrument.

A promissory note can be secured with a pledge of collateral, which is something of value that can be seized if a borrower defaults.

When a loan changes hands, the promissory note is endorsed (signed over) to the new owner of the loan. In some cases, the note is endorsed in blank which makes it a bearer instrument under Article 3 of the Uniform Commercial Code. So, any party that possesses the note has the legal authority to enforce it.

The lender holds the promissory note while the loan is being repaid, then the note is marked as paid and returned to the borrower when the loan is satisfied. Promissory notes aren't the same as mortgages, but the two often go hand in hand when someone is buying a home.

What is the difference between a Promissory Note and a Loan Agreement? Both contracts evidence a debt owed from the Borrower to the Lender, but the Loan Agreement contains more extensive clauses than the Promissory Note. Further, only the Borrower signs the promissory note while both parties sign a loan agreement.