North Carolina Request that Contracting Body Provide Copy of Payment Bond and Contract Covered by Bond - Corporation

Overview of this form

The Request that Contracting Body Provide Copy of Payment Bond and Contract Covered by Bond is a legal form used by corporations. This form allows a corporation entitled to bring an action or that is a defendant in an action on a payment bond to formally request a copy of the payment bond and the associated construction contract from the contracting body. This request must be made within a specified timeframe, differentiating it from other related forms which may not have the same urgency or legal stipulations.

What’s included in this form

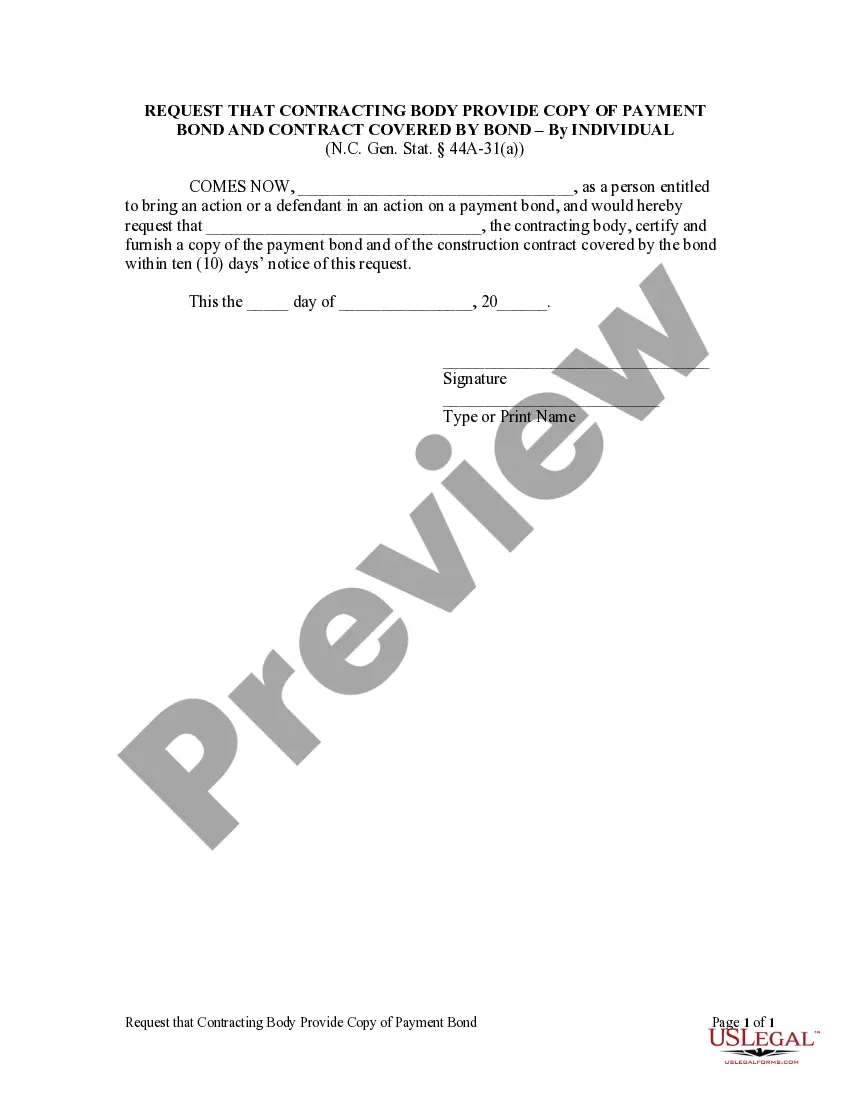

- Identifies the requesting corporation and its representative.

- Requests the contracting body to provide a certified copy of the payment bond and construction contract.

- Specifies a ten-day response period for the contracting body.

- Includes a space for the date, signature, and printed name of the representative.

- Captures the title of the representative and the corporation's identification.

Common use cases

This form is typically used when a corporation needs to retrieve a copy of a payment bond and the construction contract associated with it. This situation often arises when there is a dispute regarding payment or performance under a construction contract where a payment bond is in place. By using this form, corporations can ensure they are following the correct legal protocol to obtain necessary documentation swiftly.

Intended users of this form

Eligible users include:

- Corporations involved in construction projects that require a payment bond.

- Representatives of corporations acting on behalf of the entity in legal matters related to payment bonds.

- Defendants in legal actions where a payment bond is being contested.

Steps to complete this form

Steps to complete this form:

- Identify the requesting corporation and its representative information.

- Clearly state the name of the contracting body from which the request is made.

- Specify the request to certify and furnish a copy of the payment bond and the construction contract.

- Enter the date of the request in the designated field.

- Ensure the representative signs and prints their name in the appropriate sections.

- Include the title of the representative and the name of the corporation.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. It is advisable to check state regulations or specific contract terms to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

Common mistakes to avoid:

- Failing to provide all necessary identification details for the corporation and its representative.

- Not specifying the requesting corporation's entitlement to the request.

- Missing the ten-day deadline for the contracting body to respond.

- Neglecting to sign the form or leaving the signature field blank.

Benefits of completing this form online

Benefits of using this form online:

- Conveniently complete and download the form from any location.

- Easily edit the form to include specific details relevant to the situation.

- Reliability from legally drafted templates that comply with state laws.

Legal use & context:

- This form is legally recognized under North Carolina General Statutes.

- It serves as an official record of the request for documentation relating to the payment bond.

- It establishes a timeline for action by the contracting body, which is crucial in legal disputes.

Key takeaways

Key takeaways:

- This form is essential for corporations needing documentation related to a payment bond.

- Timeliness is critical; the contracting body must respond within ten days.

- It is important to complete the form accurately to avoid legal complications.

Looking for another form?

Form popularity

FAQ

A surety bond is a three-party contract by which one party (the surety) guarantees the performance of a second party (the principal) to a third party (the obligee). Surety bonds that are written for construction projects are called contract surety bonds.

A Miller Act Claim is similar to a bond claim or mechanics lien for contractors working on a federal construction project. It is a mechanism that encourages the general contractor to pay promptly and resolve payment issues that may exist between you and your contractor.

Write the name of the obligor, or project owner, on the line preceded or followed by are held and firmly bonded to. Write the amount of money at issue in the bond on the line designated for the bond amount. Sign the bond in the presence of a notary public and have the bond notarized.

California contractors are required to maintain an active $15,000 license bond (or cash equivalent) on file with the CSLB as a condition of being licensed.

The performance bond guarantees that the contractor will complete the project in accordance with the contract and specifications. The performance bond protects the obligee from being left with incomplete or inaccurate work.

Step 1: Verify which surety bond form you need. Step 2: Apply for a surety bond. Step 3: Get a surety bond quote. Step 4: Pay for your surety bond. Step 5: Verify the information on your bond. Step 6: File you surety bond with the obligee.

Surety bonds financially compensate the client if the contractor does not fulfill his contractual obligation. Most federal, state and municipal contracts require independent contractors to obtain a bond as part of a project agreement. Some states request a bond as part of the professional licensing process.

Contract bonds are used to guarantee performance of a written contract. They are primarily used in construction contracts. The following are the most common types of contract bonds: Bid bonds - When construction projects are awarded based on the lowest bid, the obligee usually also requires a bid bond.

Sometimes called warranty bonds, a maintenance bond is a type of surety bond that protects the owner of a completed construction project for a specified time period against faults and defects in workmanship, materials, and design that could arise later if the work was done incorrectly.