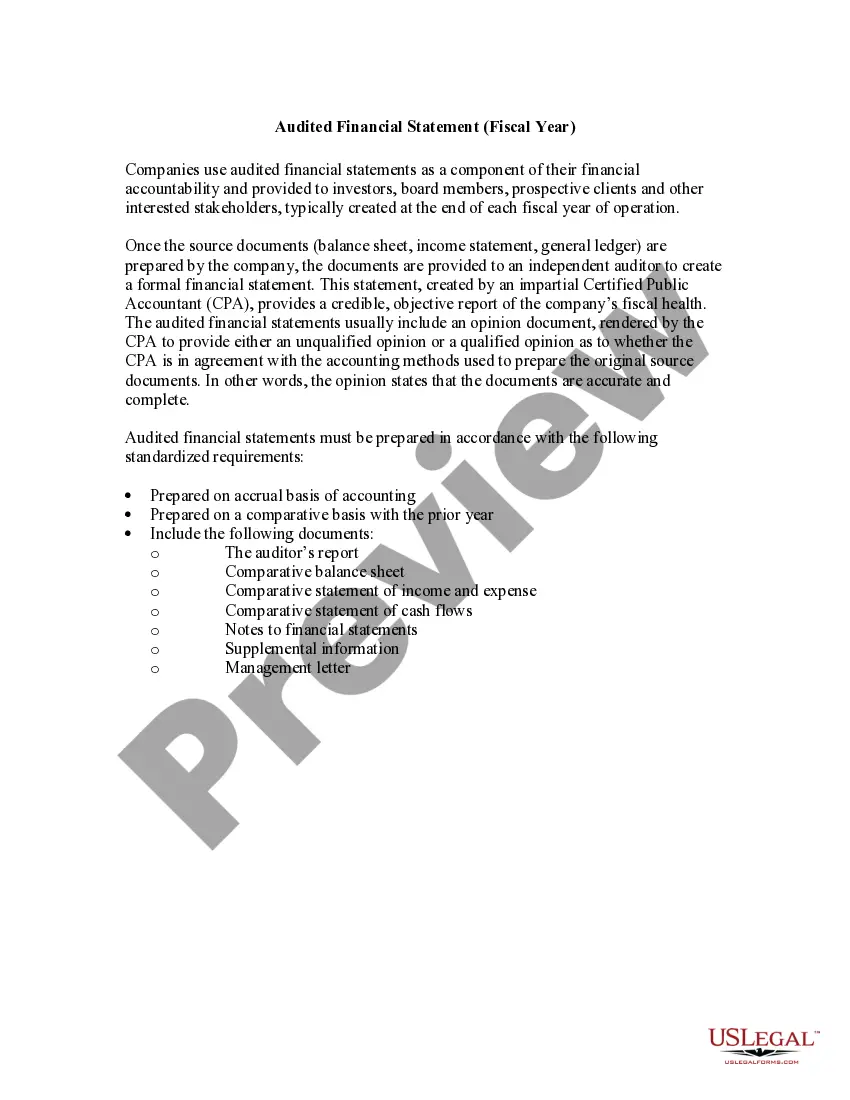

As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

Montana Report of Independent Accountants after Audit of Financial Statements

Category:

State:

Multi-State

Control #:

US-01939BG

Format:

Word

Instant download

Description

How to fill out Report Of Independent Accountants After Audit Of Financial Statements?

Have you ever found yourself in a situation where you require documents for various company or specific purposes consistently.

There are numerous authentic document templates accessible online, but locating ones you can trust is not easy.

US Legal Forms offers thousands of template forms, such as the Montana Report of Independent Accountants after Audit of Financial Statements, designed to comply with federal and state regulations.

When you locate the appropriate form, click Purchase now.

Choose the payment plan you prefer, fill in the necessary information to create your account, and complete your order using PayPal or a Visa or Mastercard.

- If you are already familiar with the US Legal Forms website and possess an account, simply Log In.

- Once logged in, you can download the Montana Report of Independent Accountants after Audit of Financial Statements template.

- If you do not have an account and want to start using US Legal Forms, follow these steps.

- Obtain the form you need and ensure it is applicable to your specific city or area.

- Utilize the Preview feature to examine the form.

- Review the description to verify that you have selected the correct form.

- If the form does not meet your needs, use the Search field to find the form that fits your requirements.

Form popularity

FAQ

An independent accountant who performs financial audits is a certified professional tasked with assessing the accuracy and integrity of financial records. This expert ensures that the financial statements reflect the true state of the organization's finances. The Montana Report of Independent Accountants after Audit of Financial Statements serves as a key document that communicates these findings to stakeholders and enhances audit reliability.

Whether you need to file audited financial statements depends on several factors, including your business structure and regulatory requirements. Generally, public companies and certain types of nonprofits are required to submit audited financial reports. Obtaining the Montana Report of Independent Accountants after Audit of Financial Statements can help you meet these obligations and enhance your organization's reputation.

An independent auditor is a professional accountant who reviews and evaluates the financial statements of an organization without any conflicts of interest. Their role is crucial in establishing credibility and trust in the financial reporting process. By producing the Montana Report of Independent Accountants after Audit of Financial Statements, they provide transparency to investors, creditors, and regulatory bodies.

An independent financial audit is a thorough examination of an organization’s financial statements by a qualified third party. The purpose of this audit is to provide assurance that the financial statements are accurate and comply with accounting standards. The resulting Montana Report of Independent Accountants after Audit of Financial Statements offers stakeholders insight into the financial health of the organization.

The independent auditor's responsibilities include evaluating the fairness and accuracy of the financial statements. They must conduct their work in accordance with established auditing standards, ultimately leading to the Montana Report of Independent Accountants after Audit of Financial Statements. This document relays the auditor’s opinion, ensuring stakeholders can trust the financial data presented.

An independent CPA is associated with the financial statements of a publicly held entity during the annual audit process. These audits are required by law to provide assurance to shareholders and regulatory bodies. The Montana Report of Independent Accountants after Audit of Financial Statements is essential for compliance and transparency in the eyes of the public.

An independent CPA is associated with the financial statements when they conduct an audit or review of those statements. This association ensures an unbiased approach and instills confidence for stakeholders. The resulting Montana Report of Independent Accountants after Audit of Financial Statements highlights the CPA's role and findings, facilitating informed decisions.

While an accountant can prepare financial statements, not all accountants are qualified to conduct audits. An independent CPA has the necessary training and experience to perform audits and develop comprehensive audit reports. A well-executed audit results in the Montana Report of Independent Accountants after Audit of Financial Statements, adding a layer of trust for users.

Yes, a CPA can prepare personal financial statements. These statements offer an overview of an individual's financial status, detailing assets, liabilities, and net worth. While personal financial statements are useful, an independent audit yields greater credibility, resulting in the Montana Report of Independent Accountants after Audit of Financial Statements.

The purpose of an independent CPA firm audit of financial statements is to provide an objective evaluation of financial records. This audit helps establish credibility with stakeholders, such as investors and creditors, who rely on accurate data for decision-making. Ultimately, the Montana Report of Independent Accountants after Audit of Financial Statements serves as a key document for transparency.