This form, a Reaffirmation Agreement, is for use in a federal bankruptcy proceeding in the designated state and district. Available in Word or pdf format.

Missouri Reaffirmation Agreement

Category:

State:

Missouri

Control #:

MO-BKR-801W

Format:

Word;

PDF;

Rich Text

Instant download

This website is not affiliated with any governmental entity

Public form

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Missouri Reaffirmation Agreement?

Obtain any template from 85,000 legal documents like the Missouri Reaffirmation Agreement online at US Legal Forms. Every template is composed and revised by state-certified attorneys.

If you possess a subscription, Log In. Once you’re on the form’s page, click the Download button and navigate to My documents to retrieve it.

If you haven't subscribed yet, follow the steps outlined below.

With US Legal Forms, you’ll consistently have instant access to the relevant downloadable sample. The platform grants you access to forms and categorizes them to facilitate your search. Utilize US Legal Forms to acquire your Missouri Reaffirmation Agreement swiftly and effortlessly.

- Verify the state-specific criteria for the Missouri Reaffirmation Agreement you intend to utilize.

- Examine the description and preview the template.

- Once you’re confident that the sample meets your needs, simply click Buy Now.

- Choose a subscription plan that aligns with your financial plan.

- Establish a personal account.

- Complete the payment in one of two suitable methods: by credit card or through PayPal.

- Choose a format to download the document in; two choices are available (PDF or Word).

- Download the document to the My documents section.

- After your reusable template is downloaded, print it out or save it to your device.

Form popularity

FAQ

A Missouri Reaffirmation Agreement works by allowing you to formally agree to continue paying a secured debt after your bankruptcy case is discharged. The agreement must be filed with the bankruptcy court and signed by you and your creditor. This process ensures that you keep the benefits of bankruptcy protection while retaining valuable assets, making it a strategic choice for many individuals.

After signing a Missouri Reaffirmation Agreement, you are obligated to continue making payments on the reaffirmed debt. This can help you retain your asset and potentially improve your credit score over time. However, if you miss payments, the lender can take action against you, so it is essential to stay on top of your financial responsibilities.

One of the main cons of entering into a Missouri Reaffirmation Agreement is that you remain personally liable for the debt, even after bankruptcy. If you fail to make payments, the lender can pursue you for the full amount owed. Additionally, reaffirmation can limit your financial flexibility, as it ties you to the debt, which may not align with your post-bankruptcy financial goals.

In Missouri, you typically have until the bankruptcy court discharges your debts to file a reaffirmation agreement. This period is often around 60 days after your bankruptcy hearing. It is crucial to submit the agreement on time to ensure that you can retain your secured assets while still benefiting from bankruptcy protections.

Typically, the creditor prepares the Missouri Reaffirmation Agreement. However, it is advisable for the debtor to review the terms carefully and consider seeking legal advice. Utilizing platforms like US Legal Forms can simplify the process, offering templates and guidance to help you create a compliant agreement. This ensures that both parties have a clear understanding of their obligations.

A Missouri Reaffirmation Agreement must meet specific legal requirements to be valid. First, it must be in writing and signed by both the debtor and the creditor. Additionally, the agreement should clearly outline the terms and conditions of the debt being reaffirmed. It is crucial to ensure compliance with the U.S. Bankruptcy Code to protect your rights.

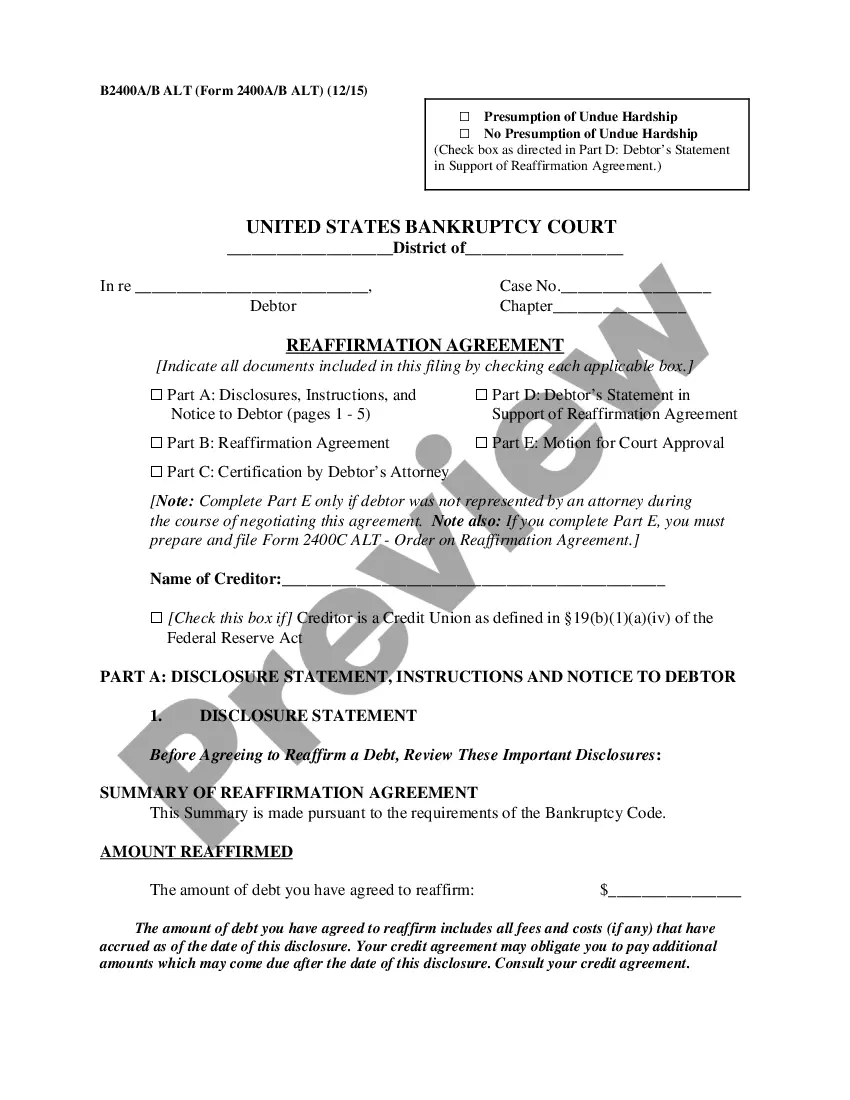

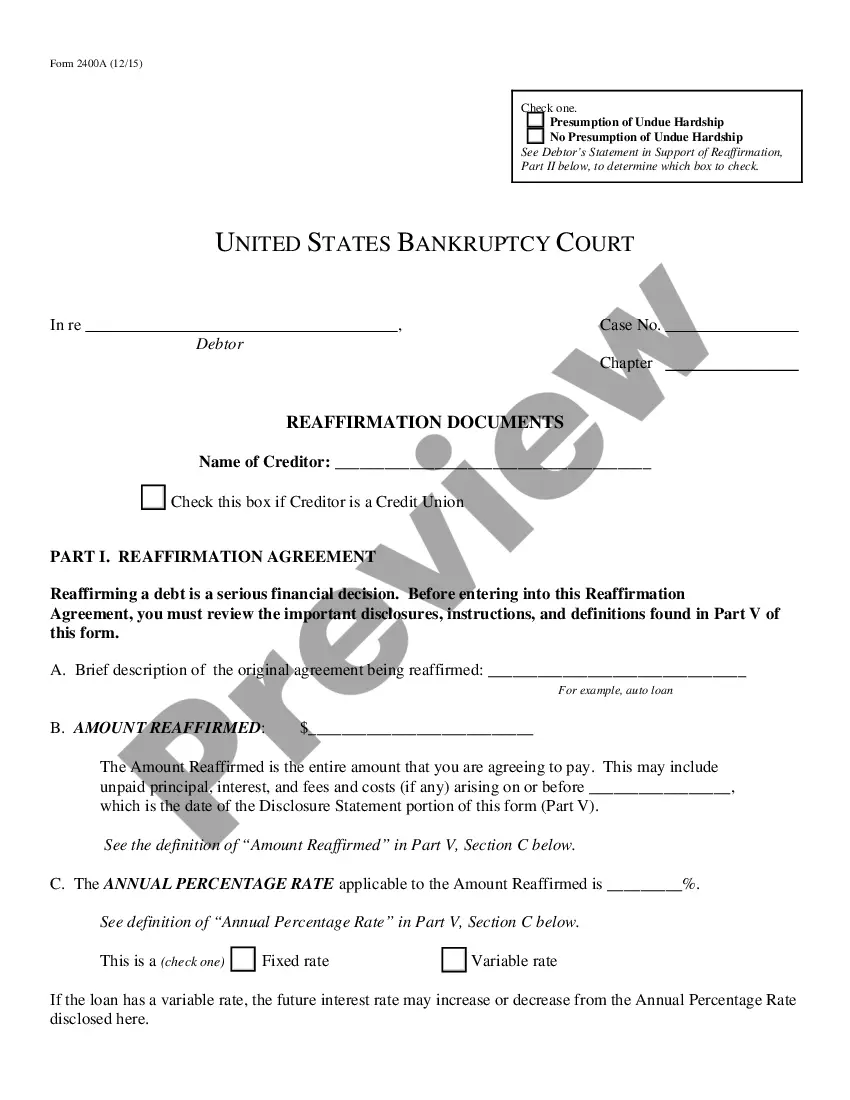

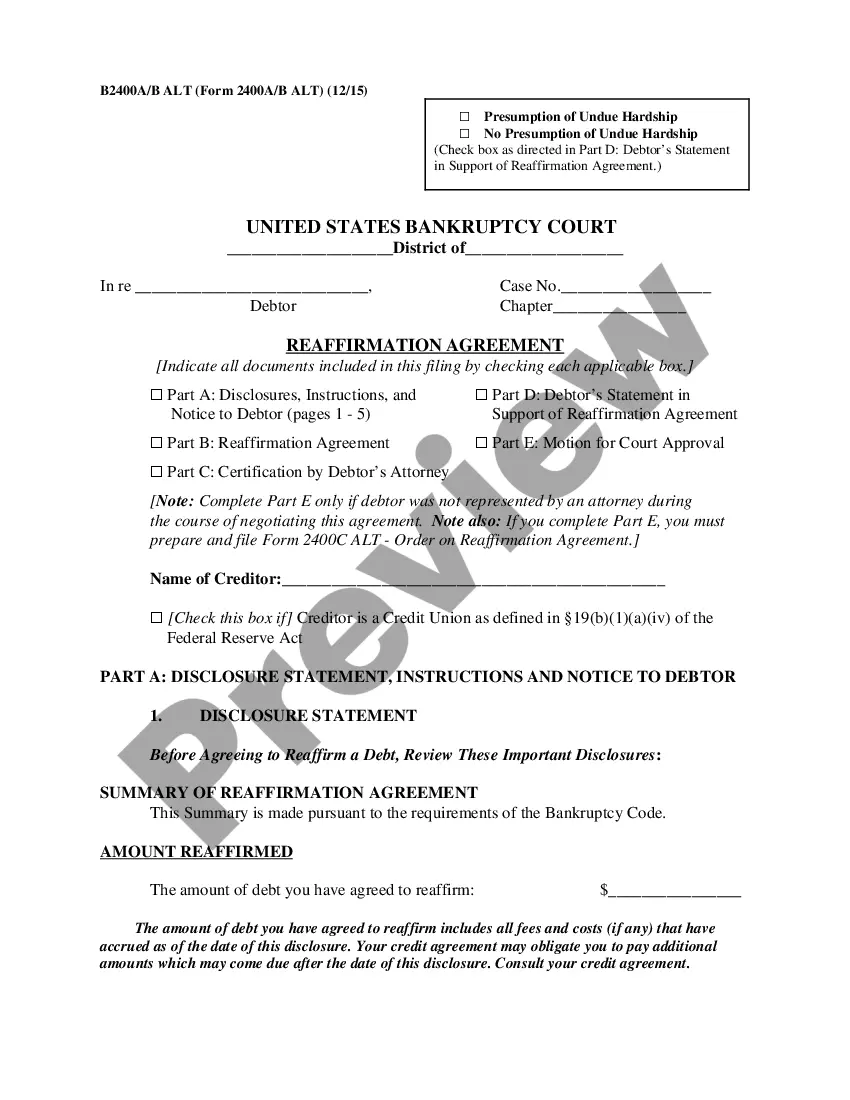

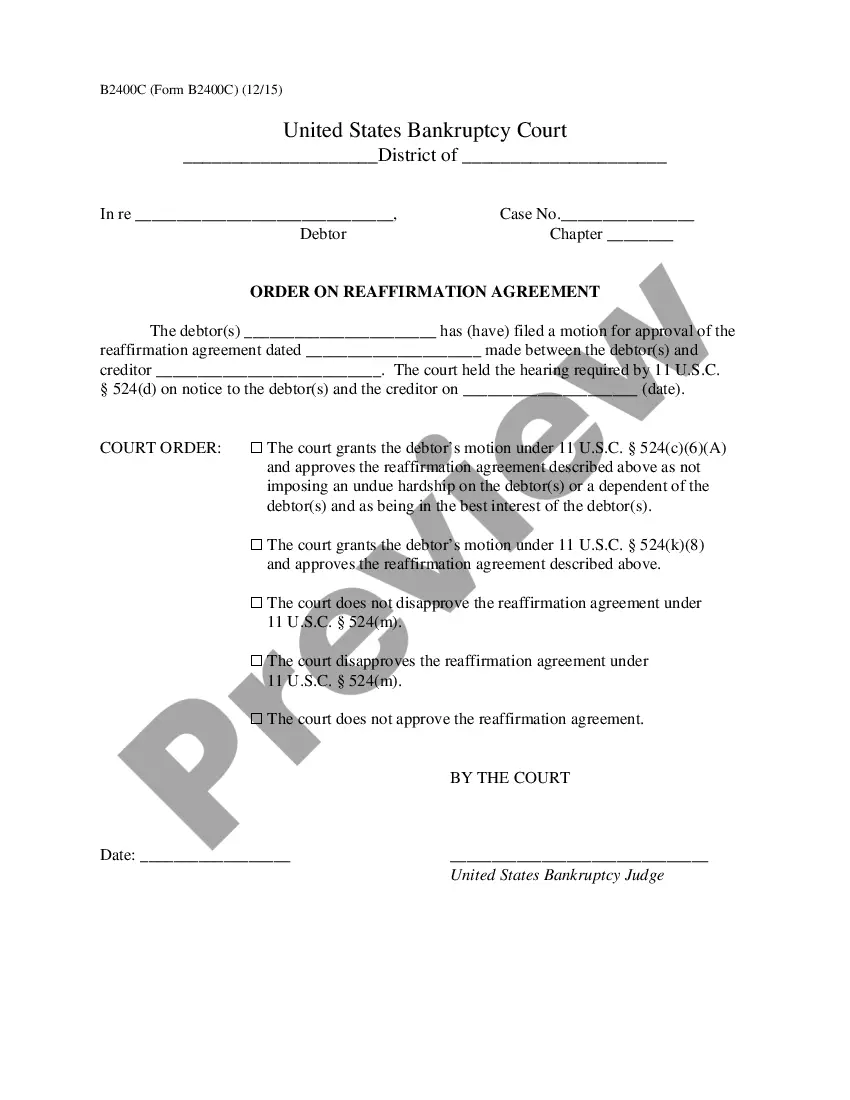

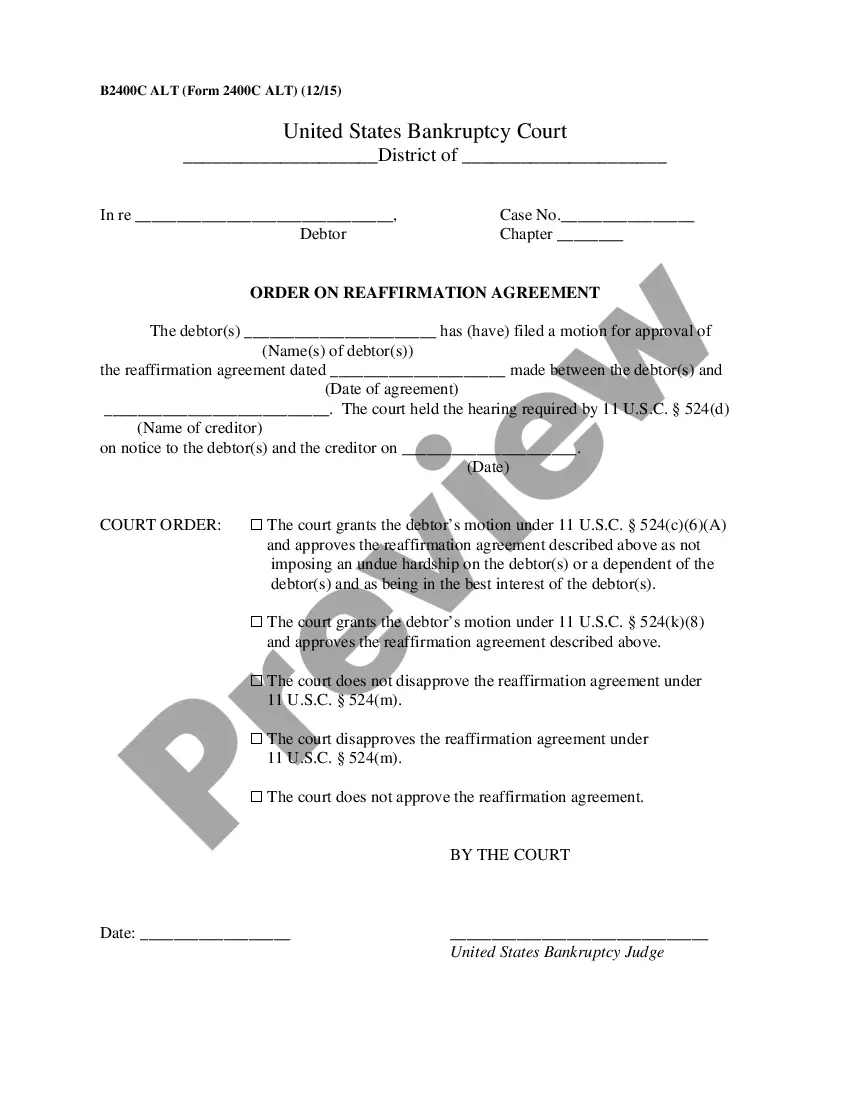

Either way - if the reaffirmation agreement is not approved, your personal liability is discharged. And - just like when the court denies approval of the reaffirmation - most lenders will simply keep everything the same, as long as you make timely payments and keep the vehicle insured.

Reaffirmation is voluntary Surrender may be the best thing if the car is simply too expensive or isn't reliable. You can choose to keep the car and continue paying without reaffirming. You take your chances that the lender will repossess the car, but you also keep the benefits of the bankruptcy discharge.

Reaffirmation is the process wherein you agree to remain responsible for a debt so that you can keep the property securing the debt (collateral). You and the lender enter into a new contractusually on the same termsand submit it to the bankruptcy court.

If you don't sign a reaffirmation agreement, the lender can repossess your car after your case closes and the automatic stay lifts. Some car lenders are known to repossess the car immediately, even if you are current on payments.