Maine Non-Foreign Affidavit Under IRC 1445

What is this form?

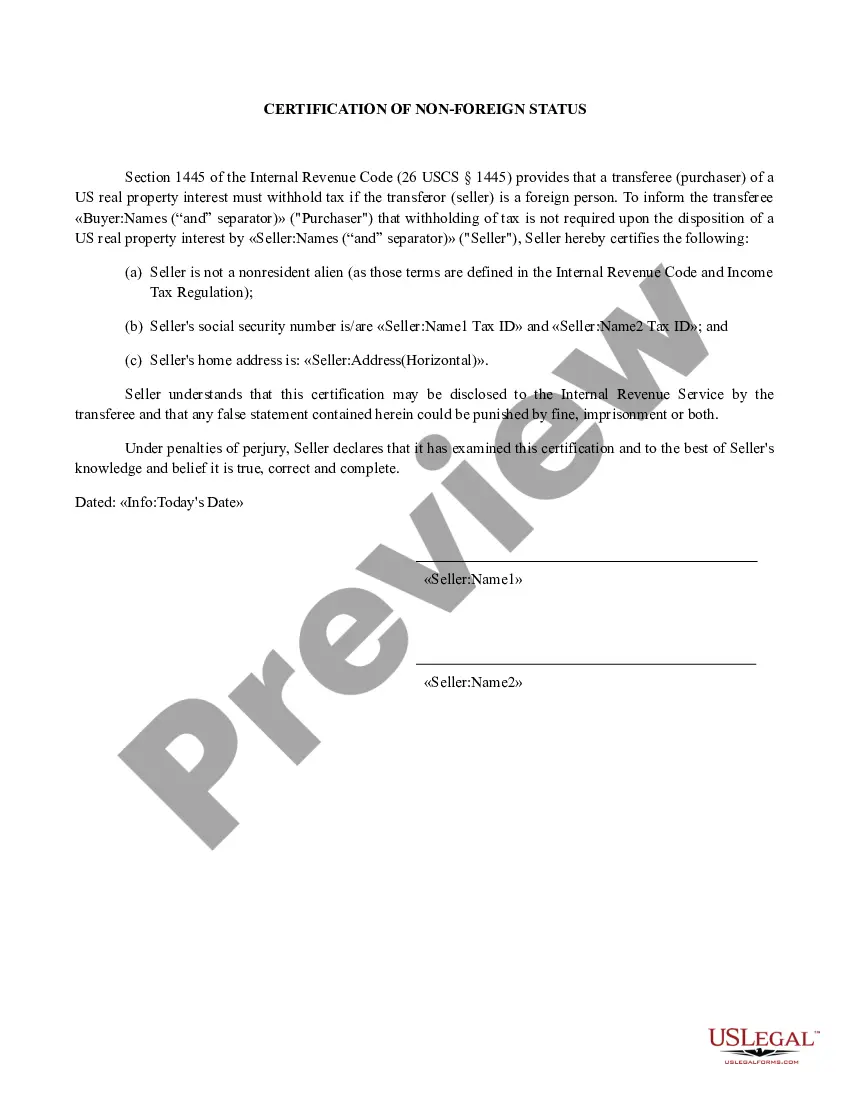

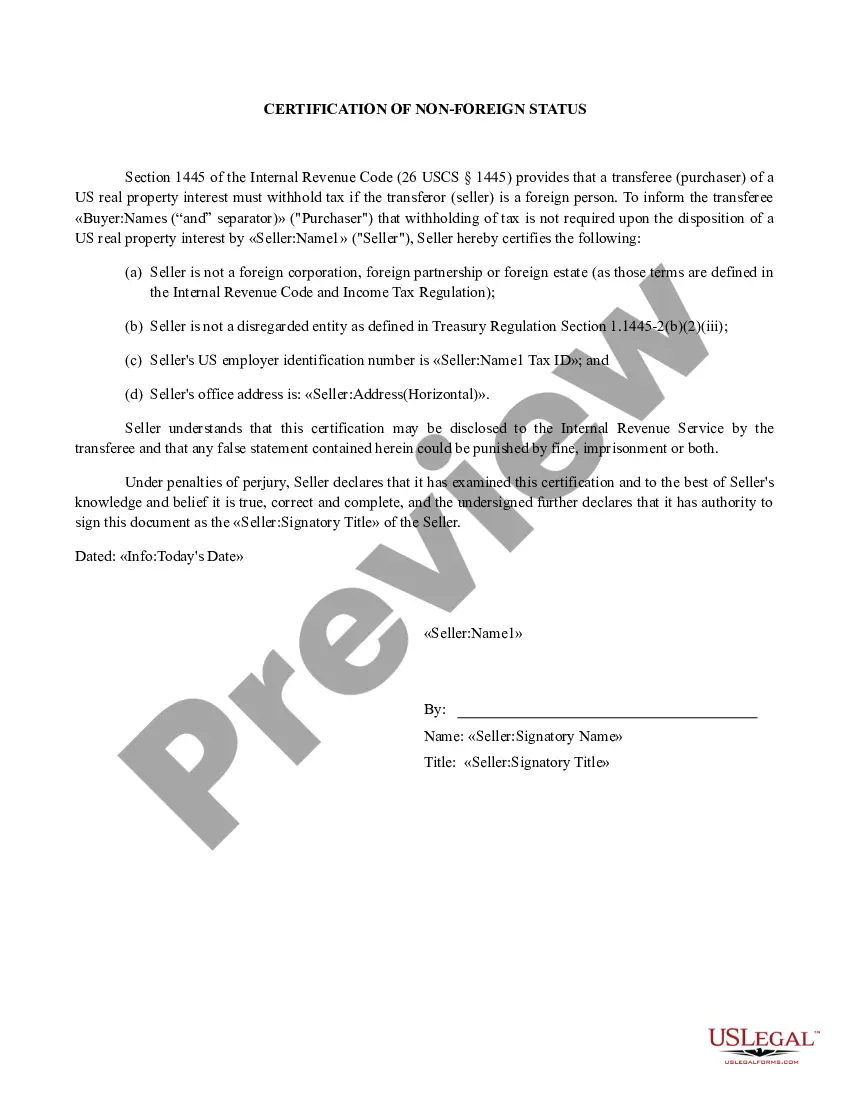

The Non-Foreign Affidavit Under IRC 1445 is a legal document that sellers of real property use to declare they are not foreign persons as defined by the Internal Revenue Code. This form is essential for complying with tax withholding requirements during property transfers, ensuring the buyer does not have to withhold a percentage of the sale price for tax purposes. It differs from other forms by specifically addressing the non-foreign status of the seller.

What’s included in this form

- Affirmation of seller's identity and property details.

- Statement confirming the seller is not a foreign person.

- Taxpayer identification number for each seller.

- Space for the buyer's information.

- Notary section for legal validation.

Situations where this form applies

This form is used when a seller is transferring real estate and needs to confirm their non-foreign status to avoid federal tax withholding obligations under Section 1445 of the Internal Revenue Code. It is particularly important in real estate transactions involving U.S. buyers and sellers. If you are engaging in a sale where the buyer may need this assurance, you should complete this affidavit.

Who should use this form

- Sellers of real property in the United States.

- Individuals or entities claiming non-foreign status under IRC 1445.

- Real estate professionals facilitating property sales.

Instructions for completing this form

- Identify the parties involved as sellers and include their contact details.

- Specify the property being sold, including its location and description.

- Enter the taxpayer identification numbers for each seller.

- Confirm the non-foreign status by checking the appropriate box.

- Have all sellers sign the document and include the date.

- Arrange for a notary to witness the signatures and complete the notarization section.

Is notarization required?

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to sign the affidavit before a notary.

- Providing incorrect or incomplete identification information.

- Not clearly identifying the property being transferred.

Advantages of online completion

- Easy download and customization to meet your specific needs.

- Access to forms prepared by licensed attorneys, ensuring accuracy and compliance.

- Convenient filling out of forms at your own pace.

Main things to remember

- This affidavit is crucial for sellers to confirm their non-foreign status during real property sales.

- All sellers must provide identification and have their signatures notarized.

- The form is compliant with IRS requirements to avoid unnecessary tax withholding.

Looking for another form?

Form popularity

FAQ

FIRPTA is a federal tax law that ensures that foreign sellers pay income tax on the sale of real property in the United States.

A withholding certificate is an application for a reduced withholding based on the gain of a sale instead of the selling price. If 15% of the selling price is more than the tax you will owe on this sale, then a withholding certificate may be ideal for you.

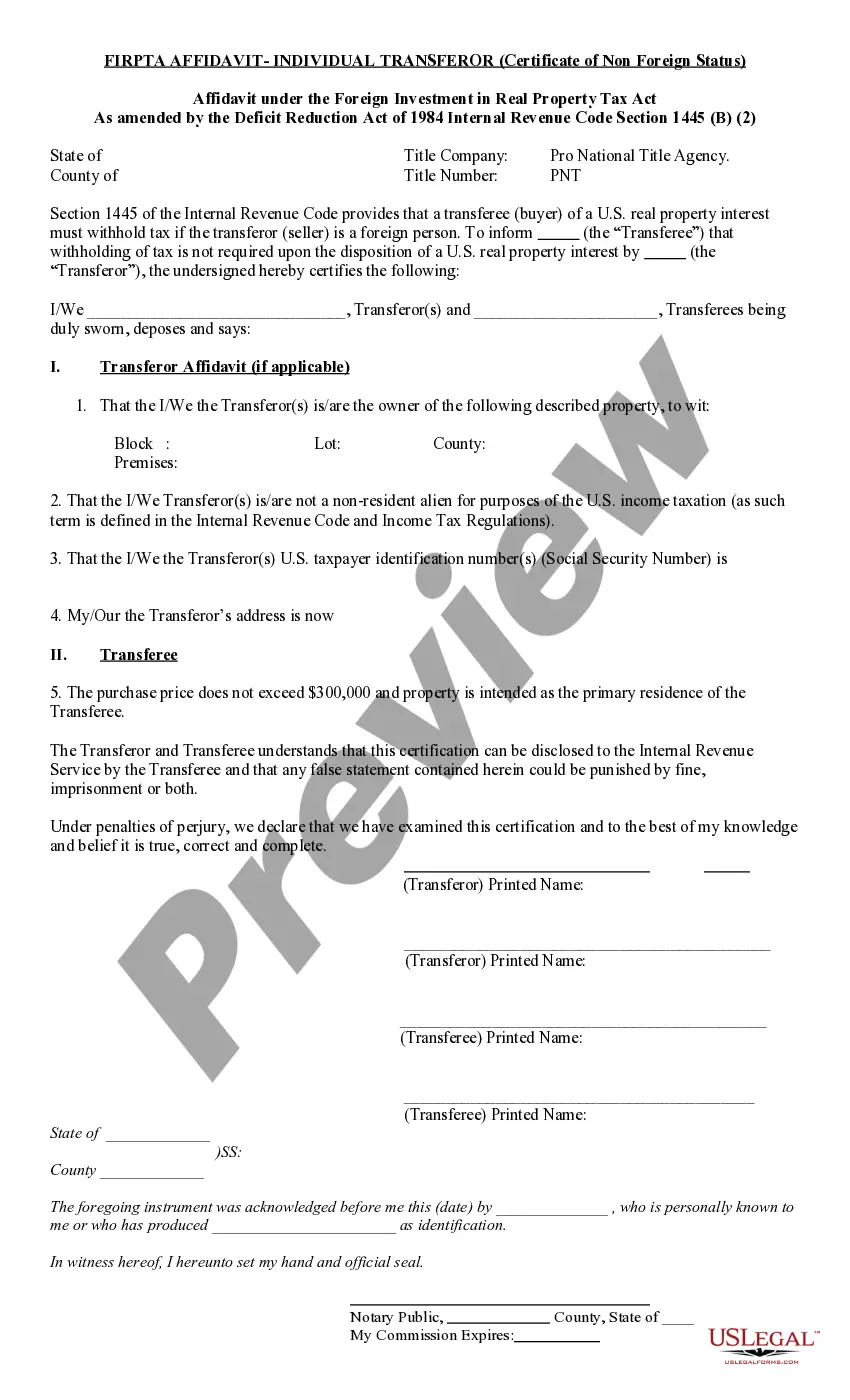

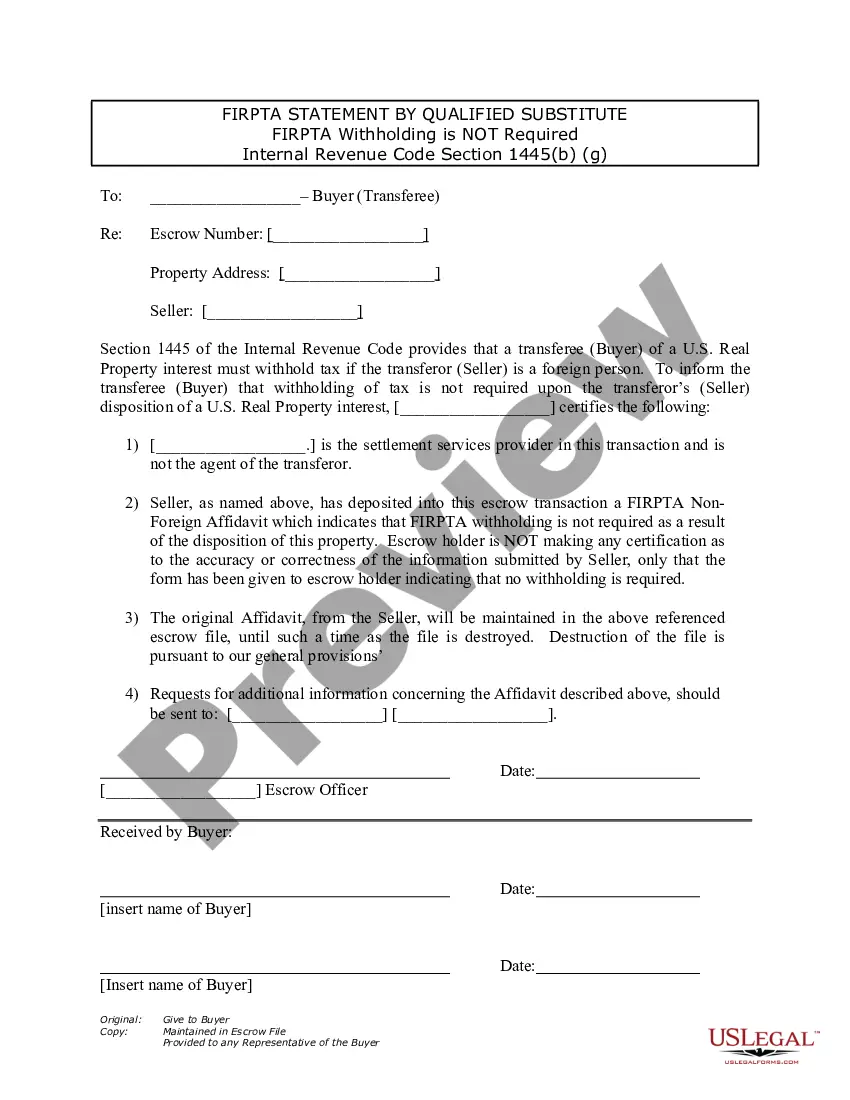

The Foreign Investment in Real Property Transfer Act (FIRPTA) requires any buyer of a U.S. real property interest to withhold ten percent of the amount realized by a foreign seller. 26 USC § 1445(a).

CERTIFICATE OF NON FOREIGN STATUS. Section 1445 of the Internal Revenue Code provides that a transferee (buyer) of a U.S. real property interest must withhold tax if the transferor (seller) is a foreign person.

What Is a Certification of Non-Foreign Status? With a Certification of Non-Foreign Status, the seller of real estate is certifying under penalty of perjury, that the seller is not foreign. Therefore, the seller and the transaction will not have the withholding requirements.

FIRPTA Exemptions The sales price is $300,000 or less, and. The buyer signs affidavit at or before closing stating they intend to use property for personal purposes for at least 50% of time property occupied for the each of the first two 12 month periods immediately after closing.

A: The buyer must agree to sign an affidavit stating that the purchase price is under $300,000 and the buyer intends to occupy. The buyer may choose not to sign the form, in which case withholding must be done.

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA) income tax withholding. FIRPTA authorized the United States to tax foreign persons on dispositions of U.S. real property interests.

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to income tax withholding (IRC section 1445).Withholding is required on certain distributions and other transactions by domestic or foreign corporations, partnerships, trusts, and estates.