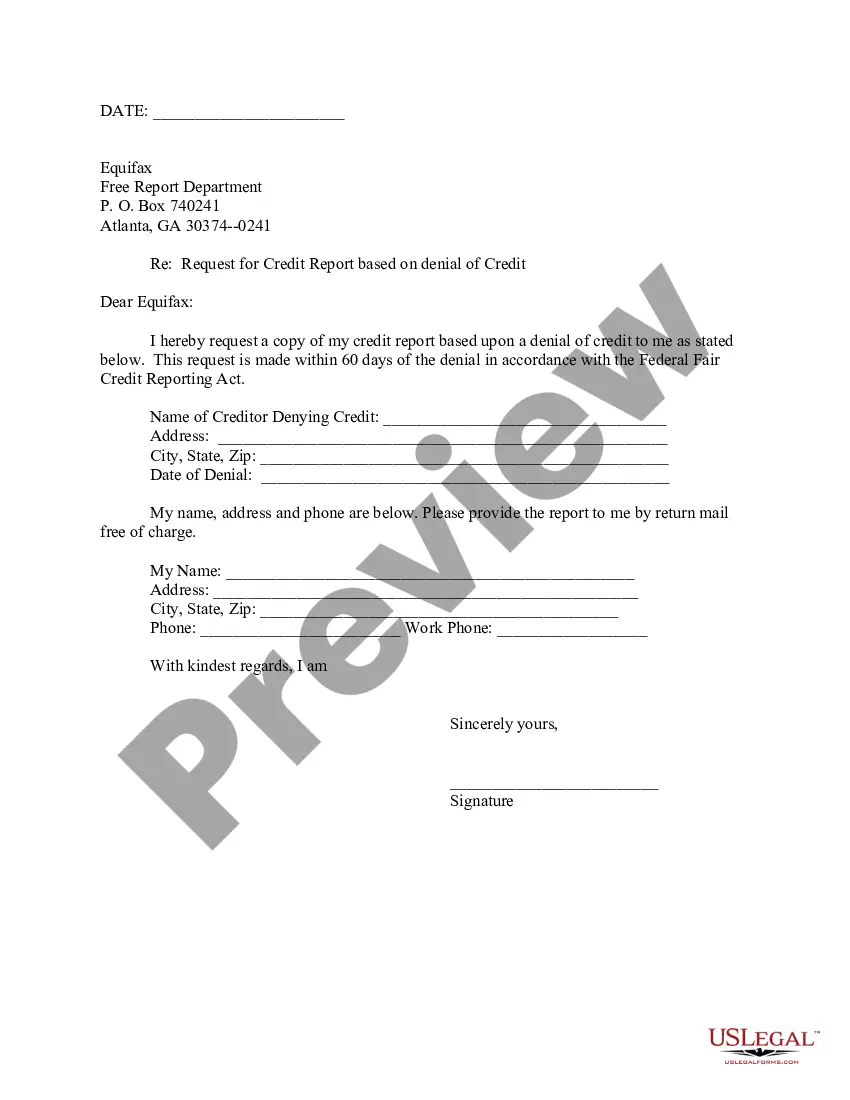

The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

Maryland Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency

Description

How to fill out Request For Disclosure Of Reasons For Denial Of Credit Application Where Action Was Based On Information Not Obtained By Reporting Agency?

Are you presently in the situation in which you will need files for both company or individual functions almost every time? There are plenty of legal file themes available on the Internet, but discovering ones you can depend on is not straightforward. US Legal Forms provides a huge number of develop themes, much like the Maryland Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency, which are written in order to meet federal and state requirements.

In case you are previously familiar with US Legal Forms website and get an account, just log in. Following that, you are able to acquire the Maryland Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency template.

Should you not offer an profile and would like to begin to use US Legal Forms, abide by these steps:

- Get the develop you will need and ensure it is for the right town/region.

- Utilize the Review option to review the form.

- See the explanation to ensure that you have chosen the proper develop.

- In case the develop is not what you are searching for, make use of the Research industry to obtain the develop that meets your requirements and requirements.

- If you discover the right develop, just click Get now.

- Choose the rates strategy you want, submit the specified details to create your money, and purchase an order making use of your PayPal or bank card.

- Decide on a hassle-free file file format and acquire your backup.

Get every one of the file themes you might have purchased in the My Forms food list. You can obtain a more backup of Maryland Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency at any time, if possible. Just select the needed develop to acquire or printing the file template.

Use US Legal Forms, the most extensive collection of legal types, to save lots of time as well as prevent faults. The service provides skillfully created legal file themes that you can use for a selection of functions. Produce an account on US Legal Forms and commence creating your life easier.

Form popularity

FAQ

If a lender rejects your application, it's required under the Equal Credit Opportunity Act (ECOA) to tell you the specific reasons your application was rejected or tell you that you have the right to learn the reasons if you ask within 60 days.

Duty to Promptly Correct and Update Information. Section 623(a) of the FCRA also requires a person who regularly furnishes information to CRAs to promptly notify a CRA if the person determines the previously furnished information is not complete or accurate.

Regulation B A written statement of actual and specific reasons for the adverse action or, if not providing the specific reason within the written notice, a statement that the applicant has a right to receive the specific reason for adverse action if requested within 60 days of the notification.

Debt-to-income ratio is high A major reason lenders reject borrowers is the debt-to-income ratio (DTI) of the borrower. Simply, a debt-to-income ratio compares one's debt obligations to his/her gross income on a monthly basis.

They do not meet the creditor's minimum income requirement; They have not been living at your address or working at your job for the required amount of time; They are too near their credit limits; and.

Reasons you may be denied for a credit card Insufficient credit history. If you have a short or nonexistent credit history, you may not qualify for a credit card. ... Low income or unemployed. ... Missed payments. ... You're carrying debt. ... Too many credit inquiries. ... Don't meet age requirements. ... There are errors on your credit report.

The Federal Equal Credit Opportunity Act prohibits creditors from discriminating against credit applicants on the basis of race, color, religion, national origin, sex, marital status, age (provided the applicant has the capacity to enter into a binding contract); because all or part of the applicant's income derives ...

First, find out what caused the lender to turn you down. If a lender rejects your application, it's required under the Equal Credit Opportunity Act (ECOA) to tell you the specific reasons your application was rejected or tell you that you have the right to learn the reasons if you ask within 60 days.