Maryland Newly Widowed Individuals Package

Overview of this form package

The Maryland Newly Widowed Individuals Package is a comprehensive set of legal documents designed specifically for individuals who have recently lost their spouse. This package will help you organize your legal affairs and ensure that your wishes are respected. It includes essential state-specific forms such as an Heirship Affidavit, General Power of Attorney, Revocation of Power of Attorney, Statutory Living Will, and a Personal Planning Information and Document Inventory Worksheet. These forms differ from others as they cater specifically to the needs of newly widowed individuals, addressing important financial and healthcare decisions during a difficult time.

Forms included in this package

- Small Estate Affidavit for Estates Not More Than $50,000 or $100,000 if Spouse is Sole Heir

- General Durable Power of Attorney for Property and Finances or Financial Effective Immediately

- Revocation of General Durable Power of Attorney

- Statutory Advance Health Directive

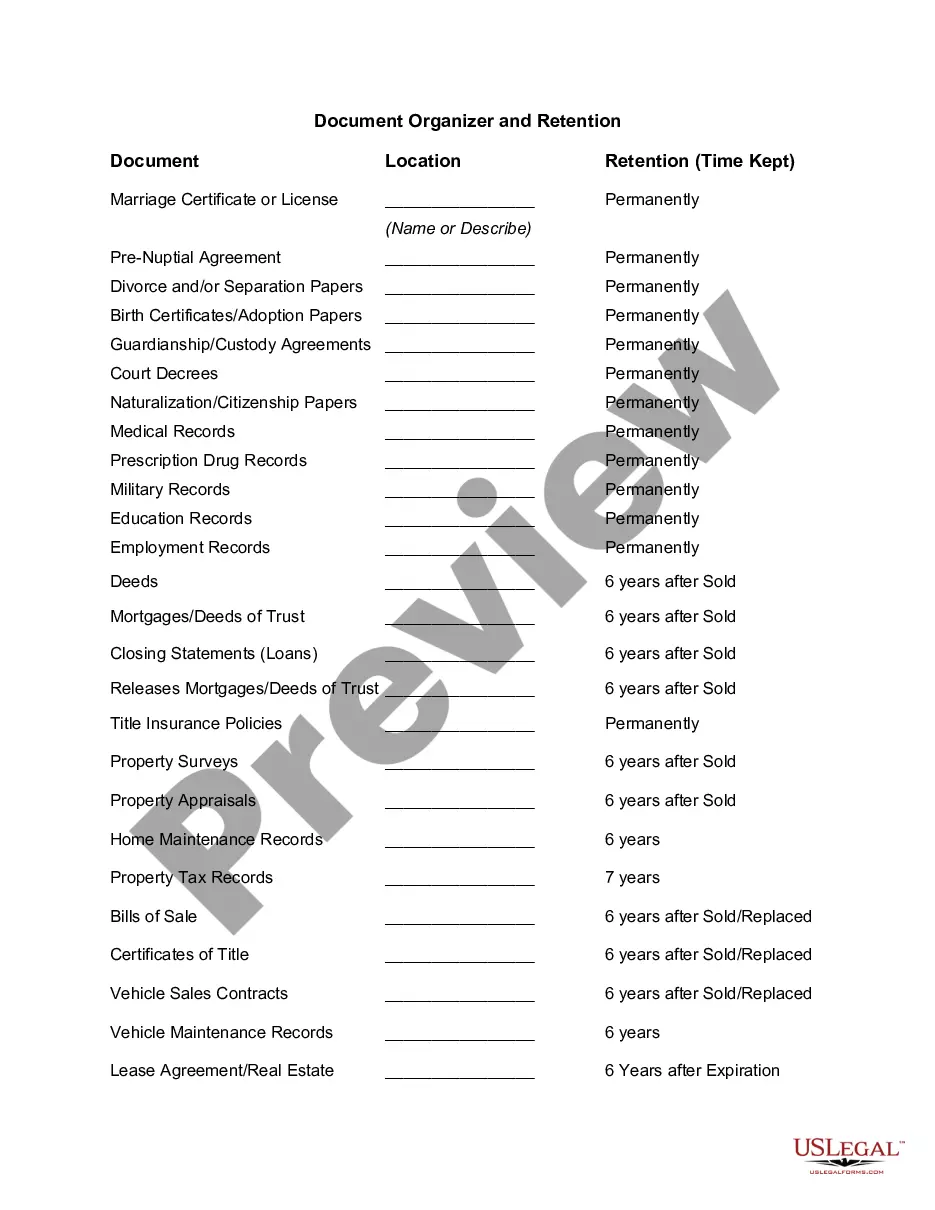

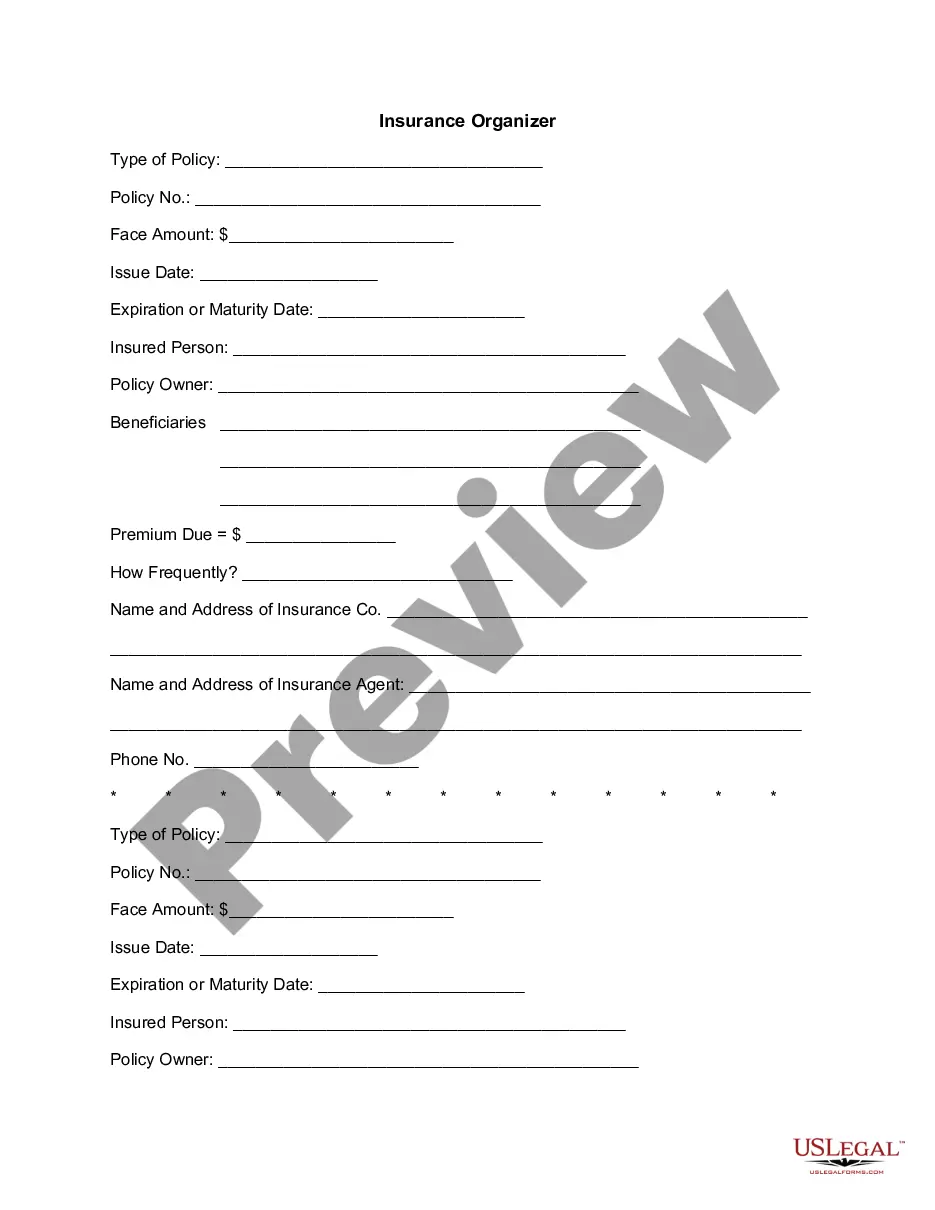

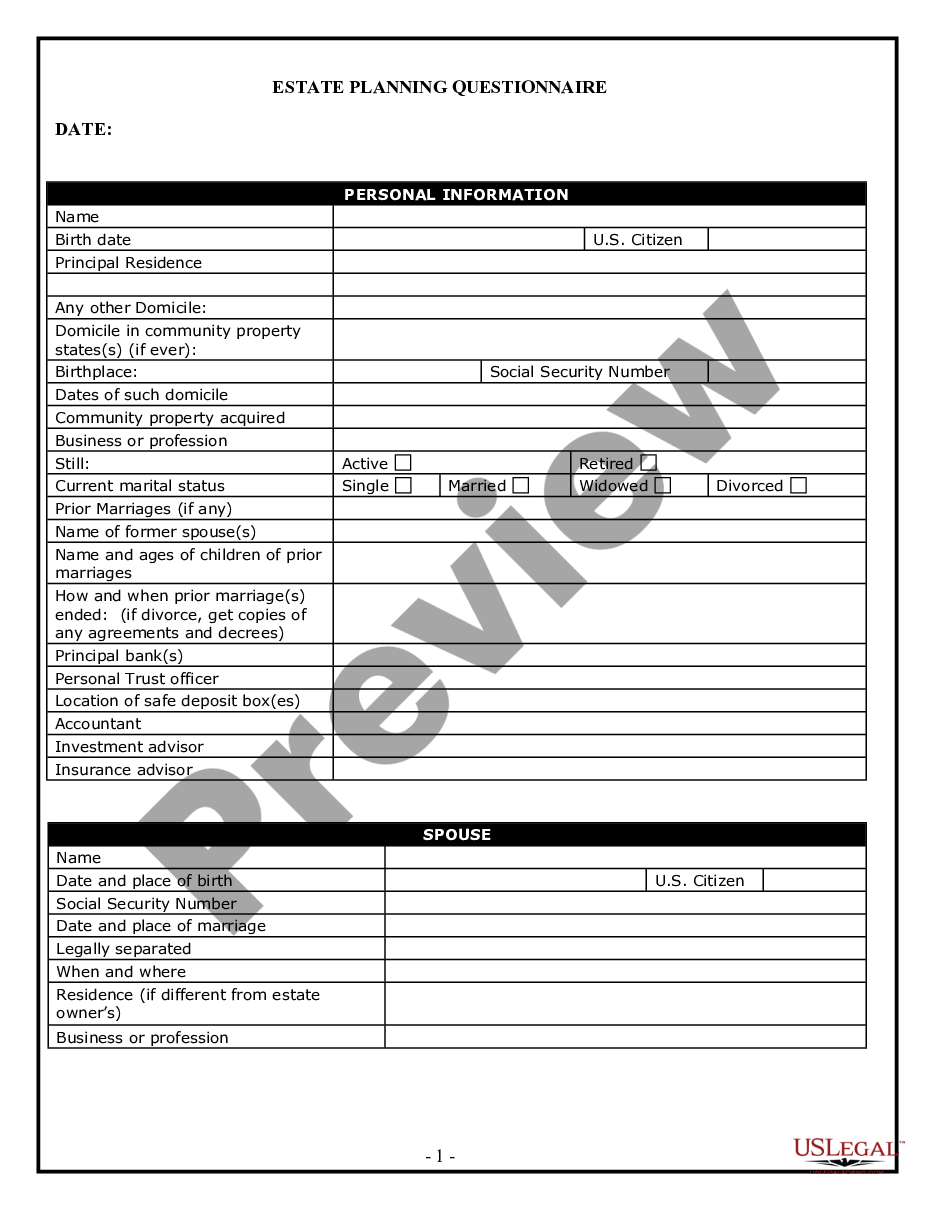

- Personal Planning Information and Document Inventory Worksheets - A Legal Life Document

When this form package is needed

This form package is essential during various scenarios, including:

- When you need to establish the rightful heirs to your spouse's estate.

- When you want to appoint someone to manage your financial affairs immediately following your spouse's passing.

- When you wish to revoke an old power of attorney that may no longer serve your best interests.

- When you want to express your healthcare wishes in case you are unable to make decisions for yourself.

- When you need to organize important personal information following the loss of a spouse.

Who should use this form package

- Individuals who have recently become widowed and need to organize their legal documents.

- Those wanting to ensure their healthcare and financial preferences are documented.

- Anyone responsible for managing the estate of a deceased spouse.

- People looking for guidance on legal matters arising from the loss of a partner.

How to complete these forms

- Review the included documents and identify which forms you need to fill out.

- Carefully read the instructions accompanying each form to understand requirements and legal implications.

- Enter the required information in the designated fields, ensuring accuracy and clarity.

- Sign the forms where necessary, considering whether notarization is required.

- Store completed documents safely, and inform your trusted contacts where they can be found.

Notarization details for included forms

Notarization is required for one or more forms in this package. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to fill out all required fields of the forms.

- Not understanding the implications of granting power of attorney.

- Overlooking the need to update documentation if circumstances change.

- Neglecting to store documents securely or inform a trusted family member of their location.

Benefits of completing this package online

- Convenience of accessing and downloading forms from anywhere at any time.

- Editability allows you to customize forms easily to fit your specific needs.

- Reliability of state-specific documents drafted by licensed attorneys ensures compliance with legal requirements.

Legal use & context

- The forms included in this package are legally valid in Maryland, making them enforceable in court.

- Having these documents prepared can prevent future legal disputes regarding your estate and healthcare preferences.

- It is advisable to review and update your documents periodically to reflect changes in your circumstances.

What to keep in mind

- This package is specifically designed for newly widowed individuals to organize their legal affairs.

- It contains vital forms necessary for making healthcare and financial decisions.

- Completing and storing these forms correctly can provide peace of mind and legal clarity.

Looking for another form?

Form popularity

FAQ

If you're making a WillMaker will, your spouse has died, and you haven't remarried, choose "I am not married" as your marital status. However, in the eyes of the law, your marriage ended when your spouse died.

The difference between Single and Widowed. When used as adjectives, single means not accompanied by anything else, whereas widowed means whose spouse has died or is gone missing.

Read on to learn more about the qualified widow or widower filing status. Qualifying Widow (or Qualifying Widower) is a filing status that allows you to retain the benefits of the Married Filing Jointly status for two years after the year of your spouse's death.

You can still use married filing jointly with your deceased spouse for the year of death unless you remarry during that year. If you remarry in the year of your spouse's death, you can't file jointly with your deceased spouse.You and your new spouse can also each use married filing separately.

The widow's tax penalty or tax trap, as some call it, refers to the situation many surviving spouses face with having to pay more taxes in the years following their spouse's passing.

After the two-year period has ended, you may no longer file as Qualifying Widow or Widower. If you remarry at this point, you can then file as Married Filing Jointly or as Married Filing Separately. If you do not remarry in the third year after your spouse's death, you are considered single.

Qualifying widow(er) status is a special filing status available to surviving spouses for two years following the year in which their spouse died. The married filing jointly and qualifying widow(er) statuses have the same applicable tax rates and tax brackets.

Although there are no additional tax breaks for widows, using the qualifying widow status means your standard deduction will be double the single status amount. Unless you qualify for something else, you'll usually file as single in the year after your spouse dies.

The deceased spouse's filing status becomes Married Filing Separately. Surviving spouses who have a dependent child may be able to use the Qualifying Widow(er) status in the two tax years following the year of the spouse's death.