Louisiana Revocable Inter Vivos Trust

What is this form?

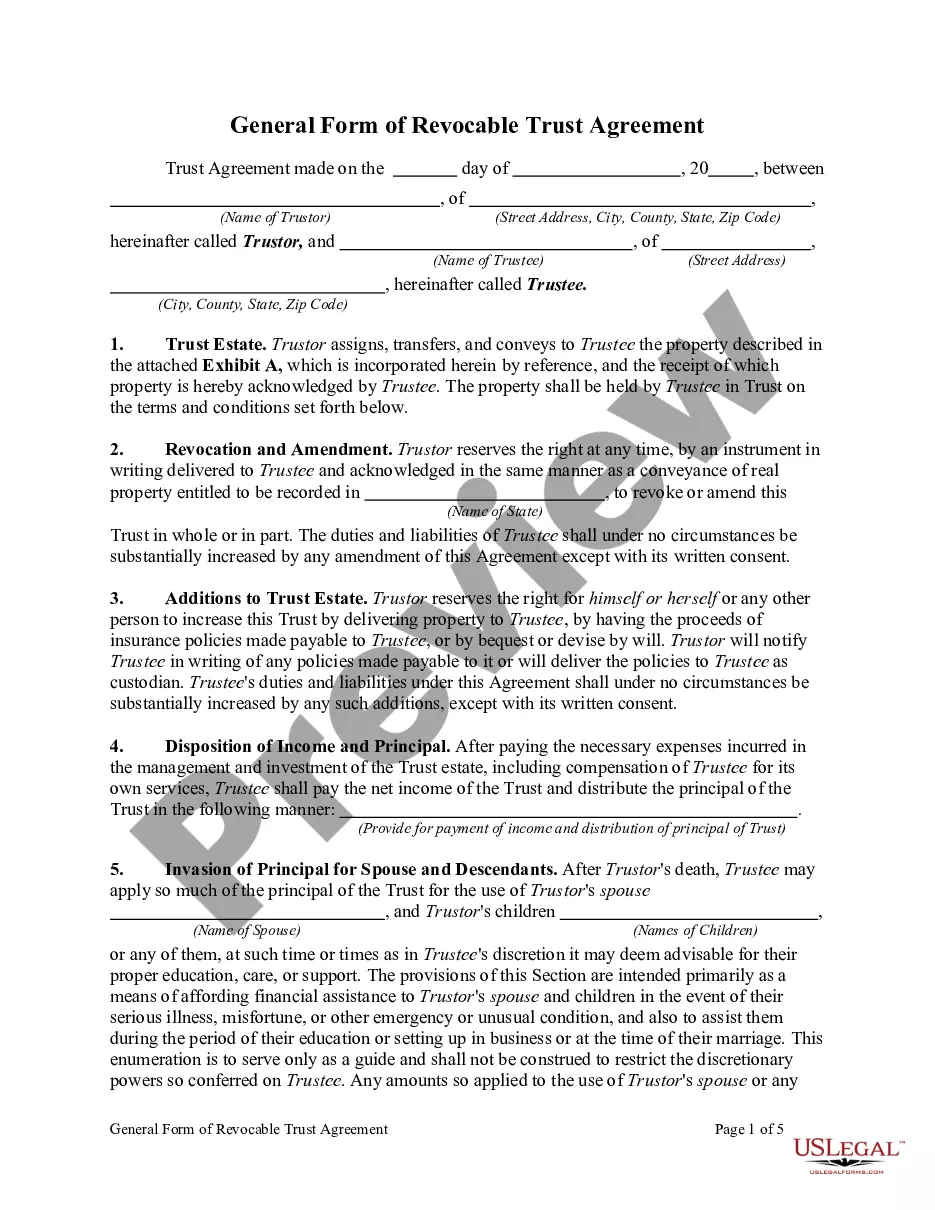

The Revocable Inter Vivos Trust is a legal document that allows the person establishing the trust, known as the Settlor, to manage and distribute their assets during their lifetime. Unlike other trusts that may be irrevocable, this type of trust can be amended or revoked at any time by the Settlor. This flexibility makes it unique and beneficial for individuals who want to retain control over their assets while planning for their management after death.

Key parts of this document

- Trust Creation: The Settlor creates the trust and transfers property into it, specifying that the trust will manage these assets.

- Trustee Appointment: A banking institution, often the preferred choice, is appointed as the initial trustee, responsible for managing the trust according to the terms set out in the document.

- Revocability: The Settlor retains the right to amend or revoke the trust at any time, ensuring ongoing control over the assets.

- Beneficiaries: Identifies who will receive the income and principal from the trust, typically the Settlor during their lifetime, and a spouse or designated individual thereafter.

- Trust Term: The trust remains in effect until the death of both the Settlor and their spouse, unless revoked earlier.

When this form is needed

This form should be utilized in various situations, such as when individuals wish to manage their assets while alive, provide for their loved ones after death, or maintain privacy regarding their estate. It is particularly useful for those wanting to avoid probate, offer asset protection, or change beneficiaries easily throughout their lifetime.

Who this form is for

This form is designed for:

- Individuals looking to establish a trust to manage their assets during their lifetime.

- Married couples aiming to provide for each other and designate beneficiaries in a flexible manner.

- People interested in simplifying estate management and avoiding probate costs and delays.

How to prepare this document

To complete this form, follow these steps:

- Identify the names and addresses of the Settlor and the banking institution acting as the trustee.

- Clearly describe the property being transferred into the trust.

- Specify the terms of revocability and amendments the Settlor wishes to maintain.

- Designate beneficiaries and outline how income will be distributed.

- Sign the document in the presence of a notary and witnesses as required.

Does this document require notarization?

Yes, this form must be notarized to be legally valid. US Legal Forms offers an integrated online notarization service, allowing users to have their documents notarized quickly and securely through a video call, ensuring compliance without the need for physical travel.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to specify all property included in the trust.

- Neglecting to have the document notarized or improperly executed.

- Not updating beneficiary designations after life changes.

Why complete this form online

- Easy access and editing capabilities online.

- Cost-effective, eliminating the need for a lawyer for simple trusts.

- Convenience of completing the form at your own pace and time.

Key takeaways

- The Revocable Inter Vivos Trust allows for controlled management of assets during life and beyond.

- It offers flexibility with the ability to amend or revoke the trust as needed.

- This trust is particularly beneficial for those wanting to avoid probate and provide clear guidance on asset distribution.

Looking for another form?

Form popularity

FAQ

The process of funding your living trust by transferring your assets to the trustee is an important part of what helps your loved ones avoid probate court in the event of your death or incapacity. Qualified retirement accounts such as 401(k)s, 403(b)s, IRAs, and annuities, should not be put in a living trust.

A Revocable Living Trust Defined Assets can include real estate, valuable possessions, bank accounts and investments. As with all living trusts, you create it during your lifetime.

Houses and other real estate (even if they're mortgaged) stock, bond, and other security accounts held by brokerages (but think about naming a TOD beneficiary instead) small business interests (stock in a closely held corporation, partnership interests, or limited liability company shares)

No separate tax return will be necessary for a Revocable Living Trust. However, even though the Grantor is taxed on the Trust income, the assets are legally held by the Trust, which will survive the Grantor's death. That is why the assets in the Trust do not need to go through the probate process.

Paperwork. Setting up a living trust isn't difficult or expensive, but it requires some paperwork. Record Keeping. After a revocable living trust is created, little day-to-day record keeping is required. Transfer Taxes. Difficulty Refinancing Trust Property. No Cutoff of Creditors' Claims.

A revocable trust becomes a separate entity only after the death of the grantor. At this point, the beneficiary must obtain an employer identification number and file a separate tax return for the entity if the income exceeds $600 in a year. To file a tax return for a separate trust entity, you must use Form 1041.

In order to set up a living trust, you should first create a document stating your intention to create a trust, and name the people who you want to benefit from the trust. You should then create another document that states the property that you want to begin the creation of the trust with.

Property you put in a living trust doesn't have to go through probate, which means that the assets won't get tied up in court for months and maybe years. However, you don't have to put bank accounts in a living trust, and sometimes it's not a good idea.

Sure you can write your own revocable living trust. In fact, you can do it better than a lot of the attorneys. First you have to ascertain that you really want a trust.