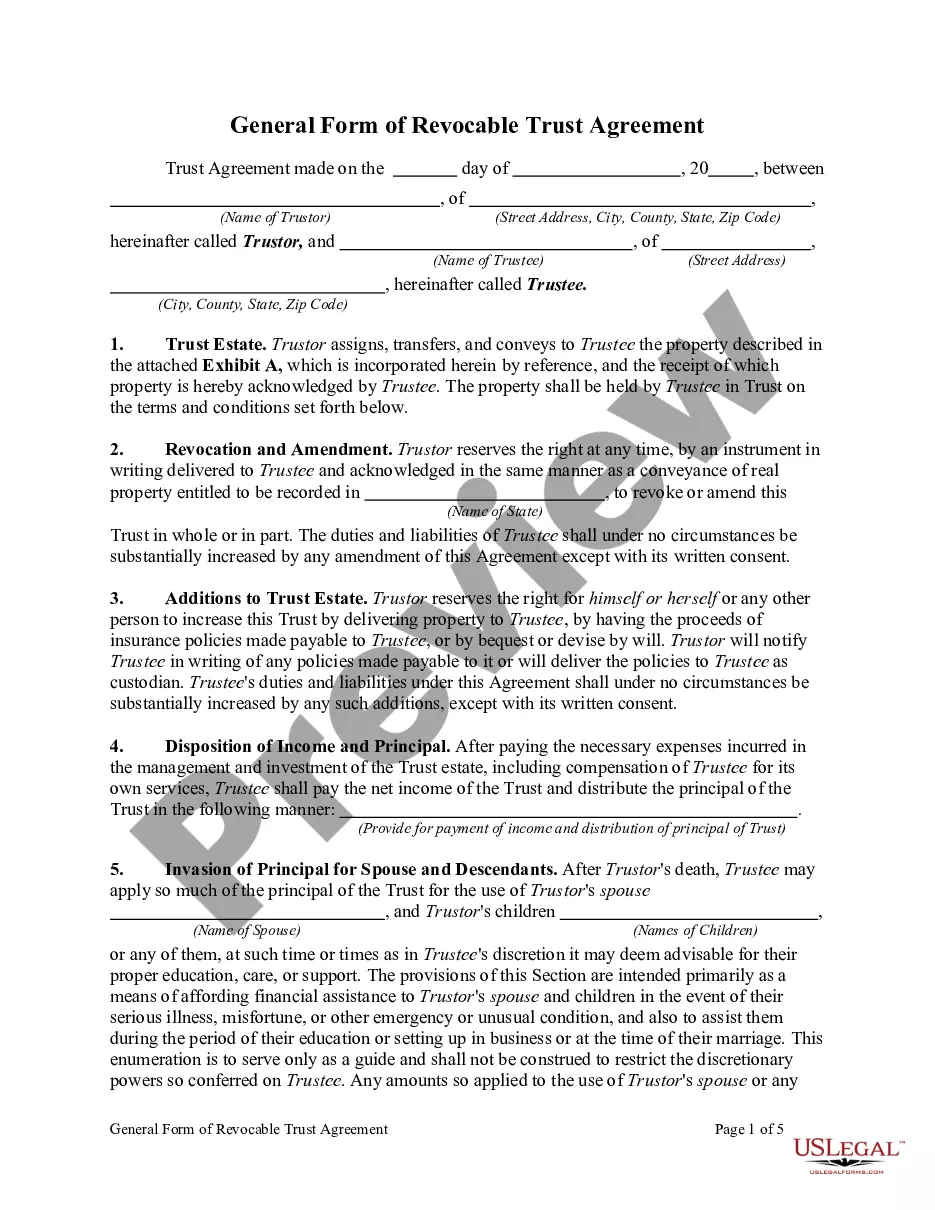

Revocable Trust for Real Estate

What is this form?

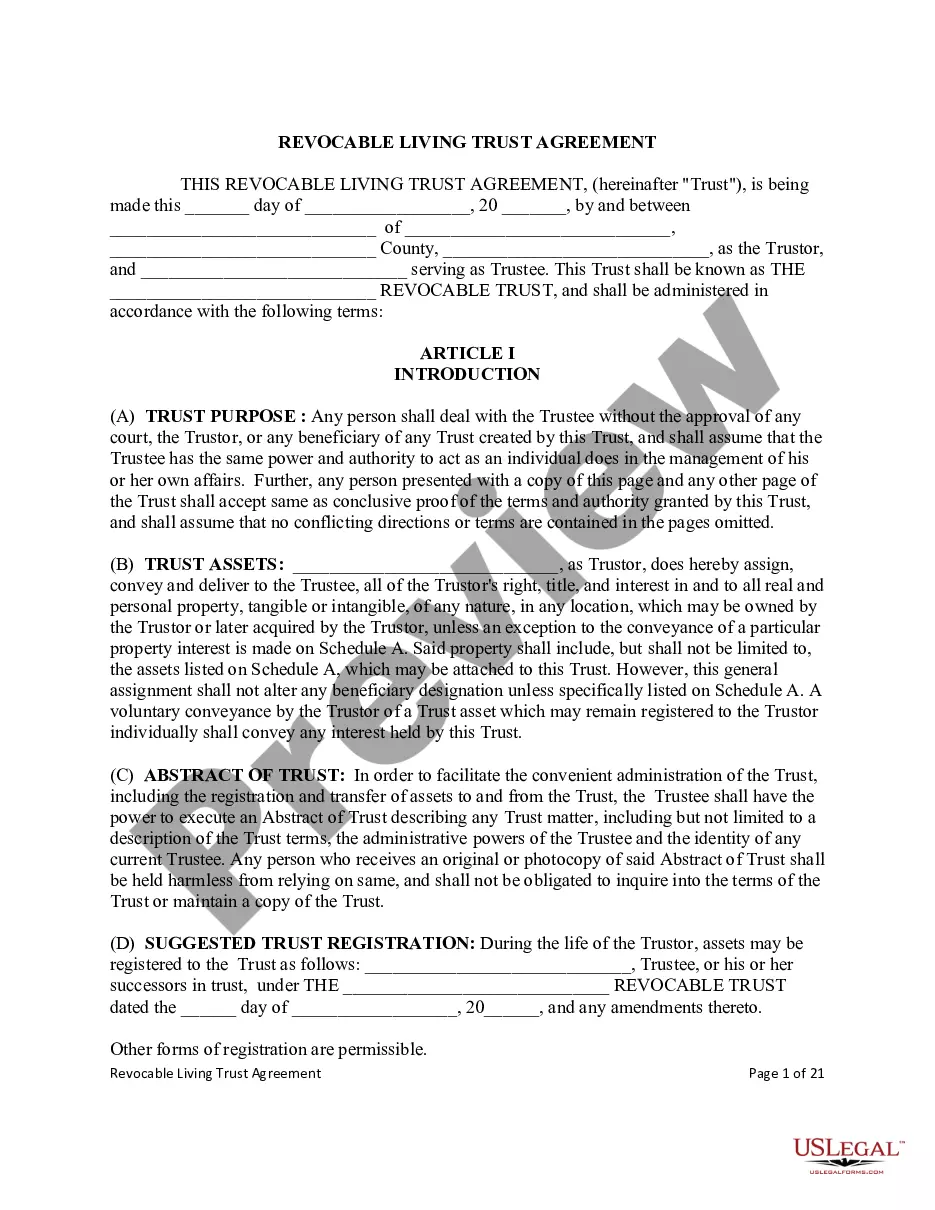

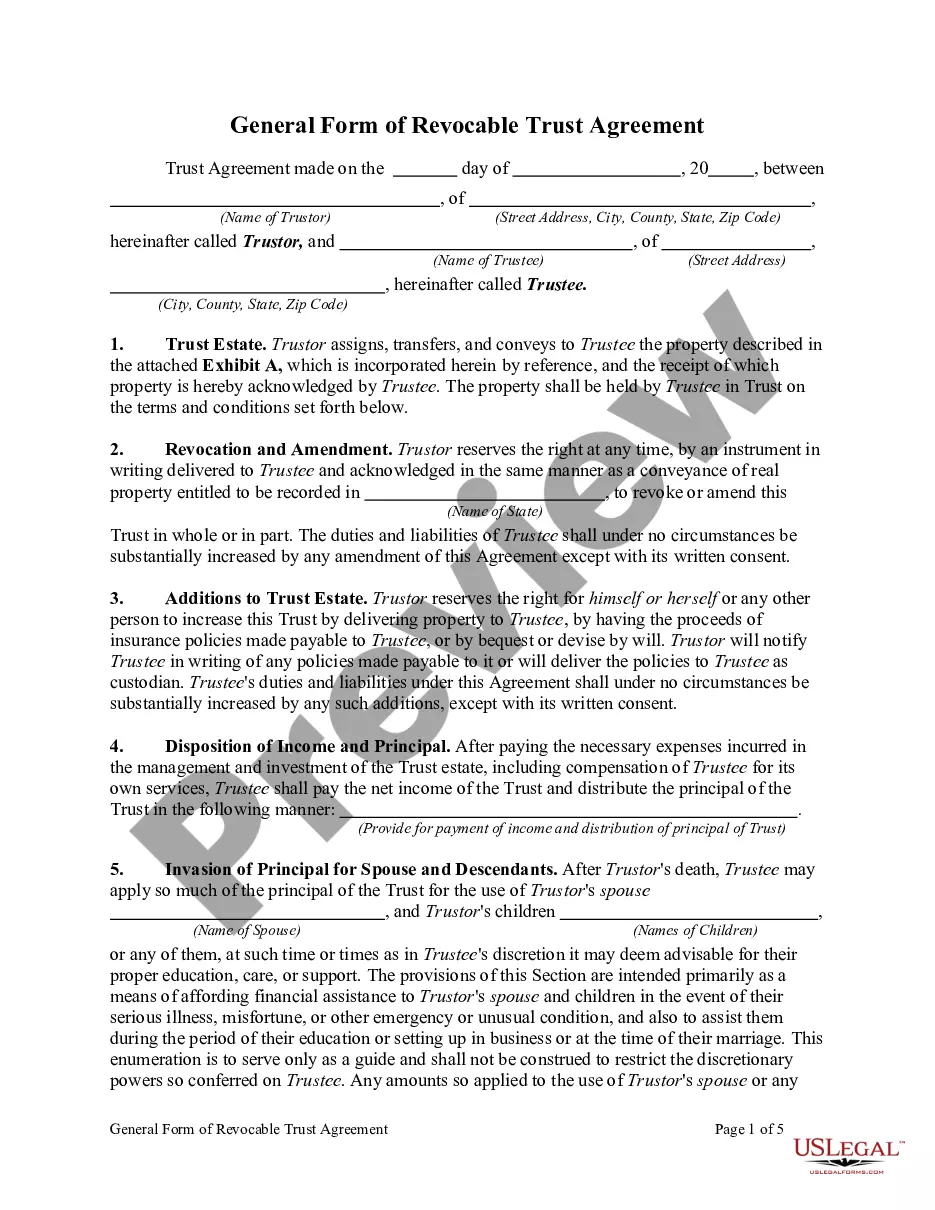

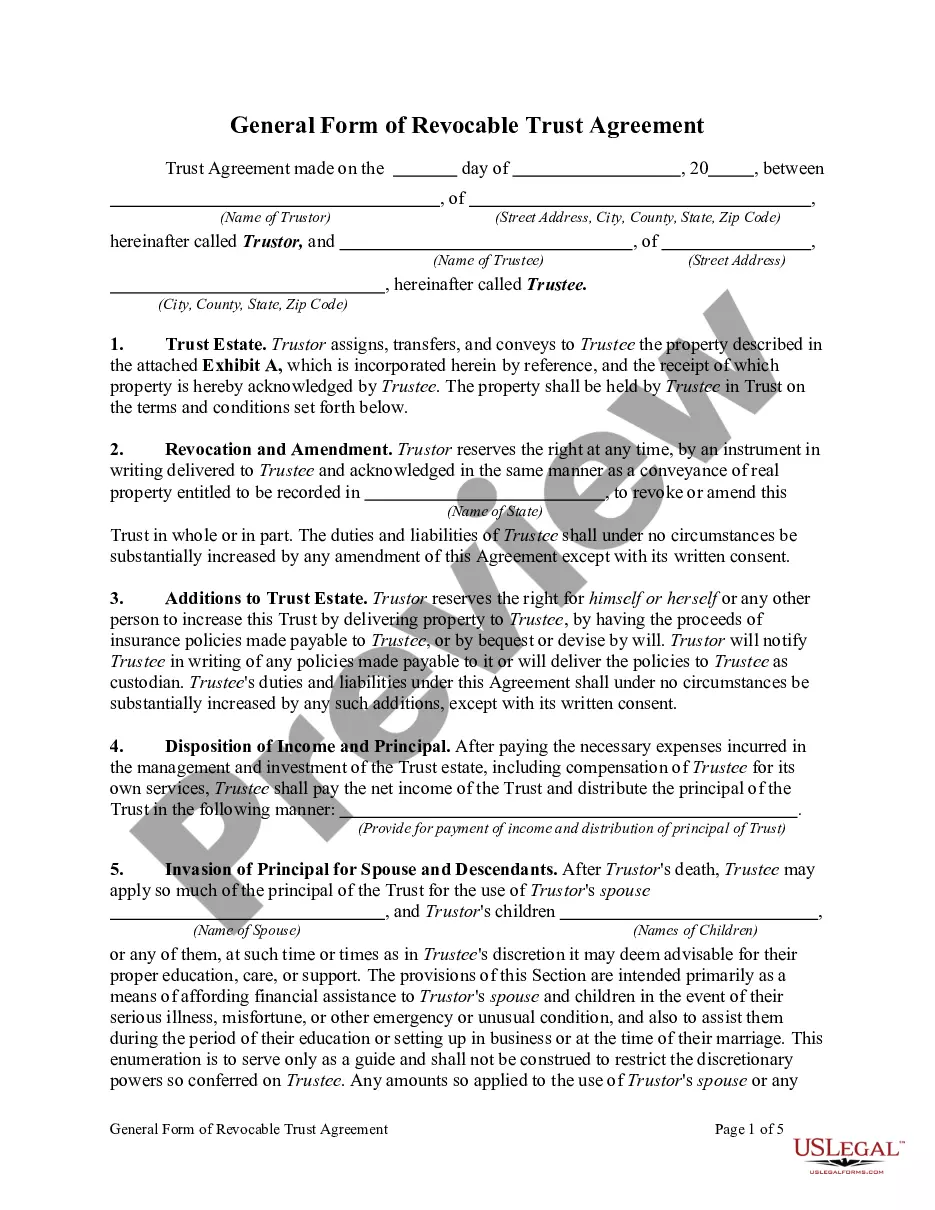

The Revocable Trust for Real Estate is a legal document that establishes a trust allowing the trustor to manage and control their real estate assets during their lifetime, with the flexibility to amend or revoke the trust as needed. Unlike irrevocable trusts, which cannot be modified once established, this revocable trust provides a more adaptable solution for individuals looking to protect their assets while retaining control over their modifications.

What’s included in this form

- Additions to Trust Estate: Allows the trustor to add property to the trust at any time.

- Distribution to Minors: Outlines how the trustee can manage distributions for minor beneficiaries.

- Powers of Trustee: Specifies the rights and powers granted to the trustee for managing trust assets.

- Transactions with Third Persons: Ensures no obligation for third parties to investigate the trustee's authority.

- Compensation of Trustee: Details the trustee's entitlement to reasonable compensation for their services.

When this form is needed

This form is useful in scenarios such as when an individual wants to manage their real estate assets effectively, wishes to avoid probate issues, or needs the flexibility to amend or dissolve their trust based on changing circumstances. It is particularly beneficial for those looking to create a plan for the distribution of their assets in the future while retaining control over those assets during their lifetime.

Who should use this form

- Individuals looking to create a trust for their real estate assets.

- Those who want a flexible estate planning tool that can be modified as needed.

- People concerned about avoiding probate for their real estate holdings.

- Parents wishing to set aside assets for their minor children.

How to prepare this document

- Identify the parties involved, including the trustor and trustee.

- Specify the details of the real estate being included in the trust.

- Outline how additions to the trust estate may occur.

- Detail any special instructions for distributions to beneficiaries, especially minors.

- Include signatures and dates where indicated to validate the trust agreement.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. Always check the specific requirements in your jurisdiction to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to specify all properties included in the trust.

- Not updating the trust when additional properties are acquired.

- Disregarding the specific needs of minor beneficiaries in distribution clauses.

- Overlooking the need for proper signatures and notarization, if required.

Benefits of completing this form online

- Convenience of accessing and completing the document from anywhere.

- Editable templates allow for quick adjustments as circumstances change.

- Reliability of attorney-drafted forms ensuring legal soundness.

Looking for another form?

Form popularity

FAQ

As far as the Internal Revenue Service is concerned, trust property belongs to the grantor. The grantor names a trustee to manage the assets, but during their lifetime, most people name themselves in this position. A successor trustee is named to carry on when the grantor dies or becomes incapacitated.

When the maker of a revocable trust, also known as the grantor or settlor, dies, the assets become property of the trust. If the grantor acted as trustee while he was alive, the named co-trustee or successor trustee will take over upon the grantor's death.

Many people use a revocable living trust because it gives them more control over the trust assets. Putting your house in a revocable trust still allows you to change the terms of the trust or remove the house from the trust if you want to.

Trust property refers to the assets placed into a trust, which are controlled by the trustee on behalf of the trustor's beneficiaries.Estate planning allows for trust property to pass directly to the designated beneficiaries upon the trustor's death without probate.

Many people use a revocable living trust because it gives them more control over the trust assets. Putting your house in a revocable trust still allows you to change the terms of the trust or remove the house from the trust if you want to.

A revocable trust is a part of estate planning that manages and protects the assets of the grantor as the owner ages. The trust can be amended or revoked as the grantor desires and is included in estate taxes.

Continuity of Management During Disability. Flexibility. Avoidance of Probate. Availability of Assets at Death. No Interruption in Investment Management. May Not Automatically Adapt to Changed Circumstances.

Due to changes in the tax laws, most revocable trusts can now be treated as part of a decedent's estate for federal income tax purposes.

Creation of a Trust To create a trust, the property owner (called the "trustor," "grantor," or "settlor") transfers legal ownership to a family member, professional, or institution (called the "trustee") to manage that property for the benefit of another person (called the "beneficiary").