Revocable Trust for House

Understanding this form

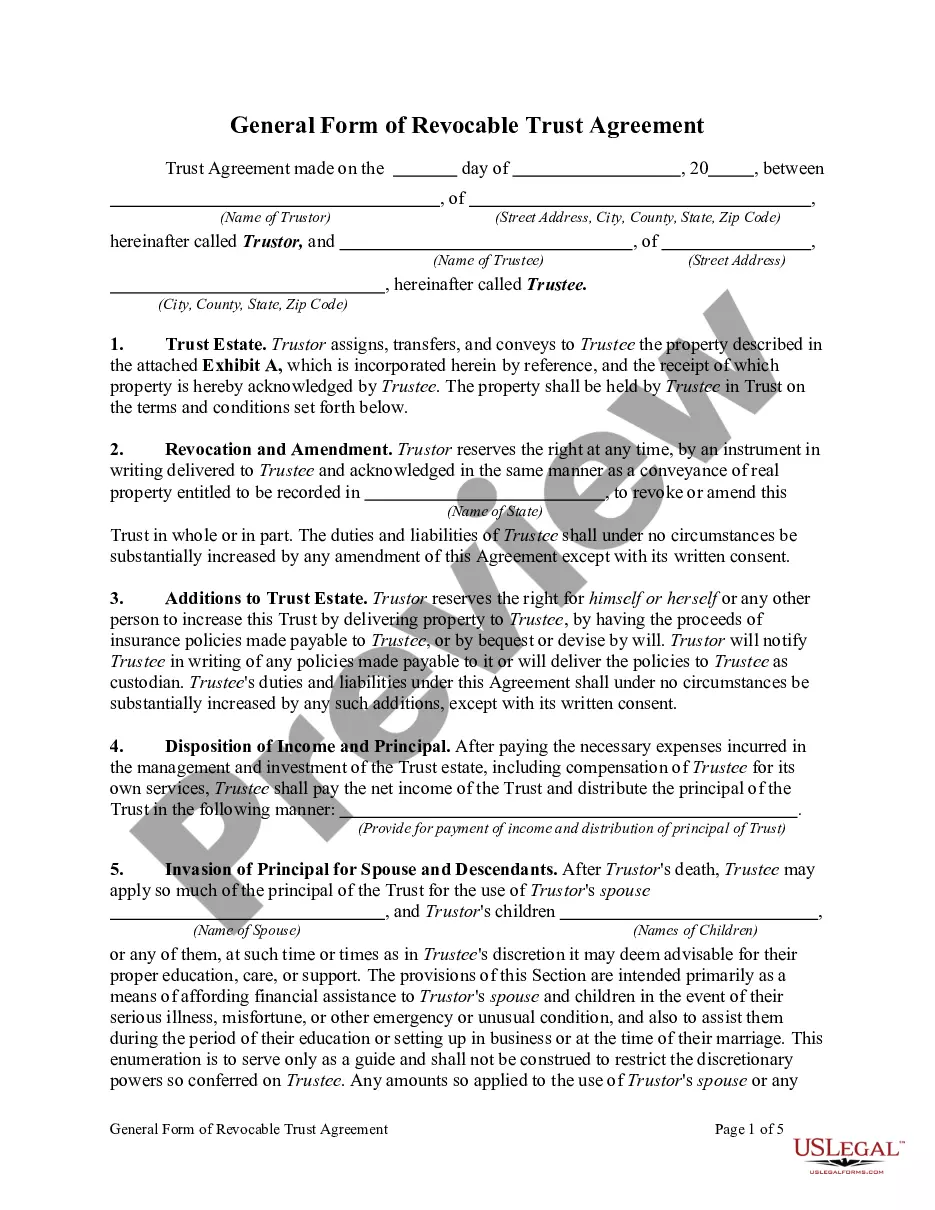

The Revocable Trust for House is a legal document that establishes a trust to hold and manage real estate. This type of trust allows the creator, known as the trustor, to maintain control over the assets during their lifetime while providing flexibility for future changes. Unlike irrevocable trusts, a revocable trust can be amended or revoked by the trustor, making it a versatile estate planning tool for homeowners. This form is specifically designed for use with residential properties and outlines the rights and responsibilities of both the trustor and trustee.

Key parts of this document

- Additions to Trust Estate: Allows the trustor to increase the trust by adding property.

- Distribution to Minors: Outlines how the trustee may manage and distribute assets intended for minors.

- Powers of Trustee: Details the authority granted to the trustee regarding asset management.

- Transactions with Third Persons: Clarifies the trustee's authority in dealings with others.

- Compensation of Trustee: Specifies the trustee's right to reasonable compensation for their services.

When this form is needed

This form should be used when you want to establish a trust that holds your home or other real estate while retaining the ability to amend or revoke the trust as needed. It is particularly useful for individuals who wish to manage their estate planning efficiently, ensuring a smooth transfer of property upon their passing or incapacity. Situations include estate planning for individuals with children, protecting assets from probate, or simplifying asset distribution among beneficiaries.

Intended users of this form

- Homeowners who want to put their property into a trust.

- Individuals looking for a flexible estate planning option.

- Those who wish to designate a trustee for asset management.

- People with minor children requiring managed distributions.

How to complete this form

- Identify the parties involved, including the trustor and trustee.

- Specify the property to be included in the trust.

- Outline any additions or changes to the trust estate.

- Determine how distributions of income to minors will be managed.

- Include signatures and dates to validate the agreement.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. However, verifying with state requirements is advisable to ensure compliance with any local regulations.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to specify all properties intended for the trust.

- Not identifying the trustee properly.

- Ignoring state-specific laws affecting the trust.

- Underestimating the importance of updating the trust after significant life changes.

Benefits of completing this form online

- Convenient access to a legally vetted document.

- Ability to edit and customize the form as needed.

- Simplified download process for immediate use.

- Guidance and support throughout the completion process.

Looking for another form?

Form popularity

FAQ

Creation of a Trust To create a trust, the property owner (called the "trustor," "grantor," or "settlor") transfers legal ownership to a family member, professional, or institution (called the "trustee") to manage that property for the benefit of another person (called the "beneficiary").

Due to changes in the tax laws, most revocable trusts can now be treated as part of a decedent's estate for federal income tax purposes.

As far as the Internal Revenue Service is concerned, trust property belongs to the grantor. The grantor names a trustee to manage the assets, but during their lifetime, most people name themselves in this position. A successor trustee is named to carry on when the grantor dies or becomes incapacitated.

Expect to pay $1,000 for a simple trust, up to several thousand dollars. You may incur additional costs after the trust has been established if you transfer property in and out or otherwise move things around. However, the bulk of the cost will be setting it up initially.

Paperwork. Setting up a living trust isn't difficult or expensive, but it requires some paperwork. Record Keeping. After a revocable living trust is created, little day-to-day record keeping is required. Transfer Taxes. Difficulty Refinancing Trust Property. No Cutoff of Creditors' Claims.

When the maker of a revocable trust, also known as the grantor or settlor, dies, the assets become property of the trust. If the grantor acted as trustee while he was alive, the named co-trustee or successor trustee will take over upon the grantor's death.

The advantages of placing your house in a trust include avoiding probate court, saving on estate taxes and possibly protecting your home from certain creditors. Disadvantages include the cost of creating the trust and the paperwork.

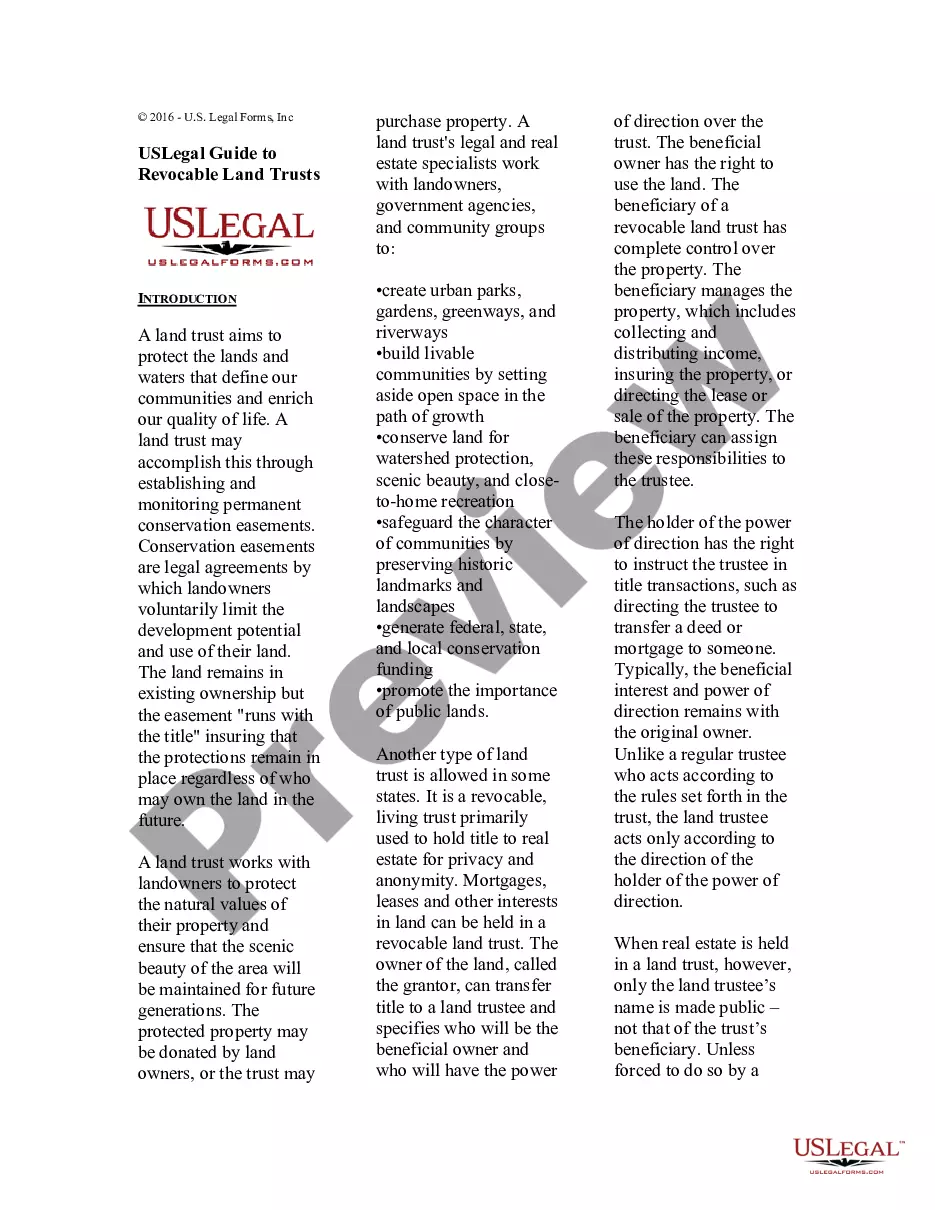

Trust property refers to the assets placed into a trust, which are controlled by the trustee on behalf of the trustor's beneficiaries.Estate planning allows for trust property to pass directly to the designated beneficiaries upon the trustor's death without probate.

A Revocable Living Trust DefinedAssets can include real estate, valuable possessions, bank accounts and investments. As with all living trusts, you create it during your lifetime.