The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use.

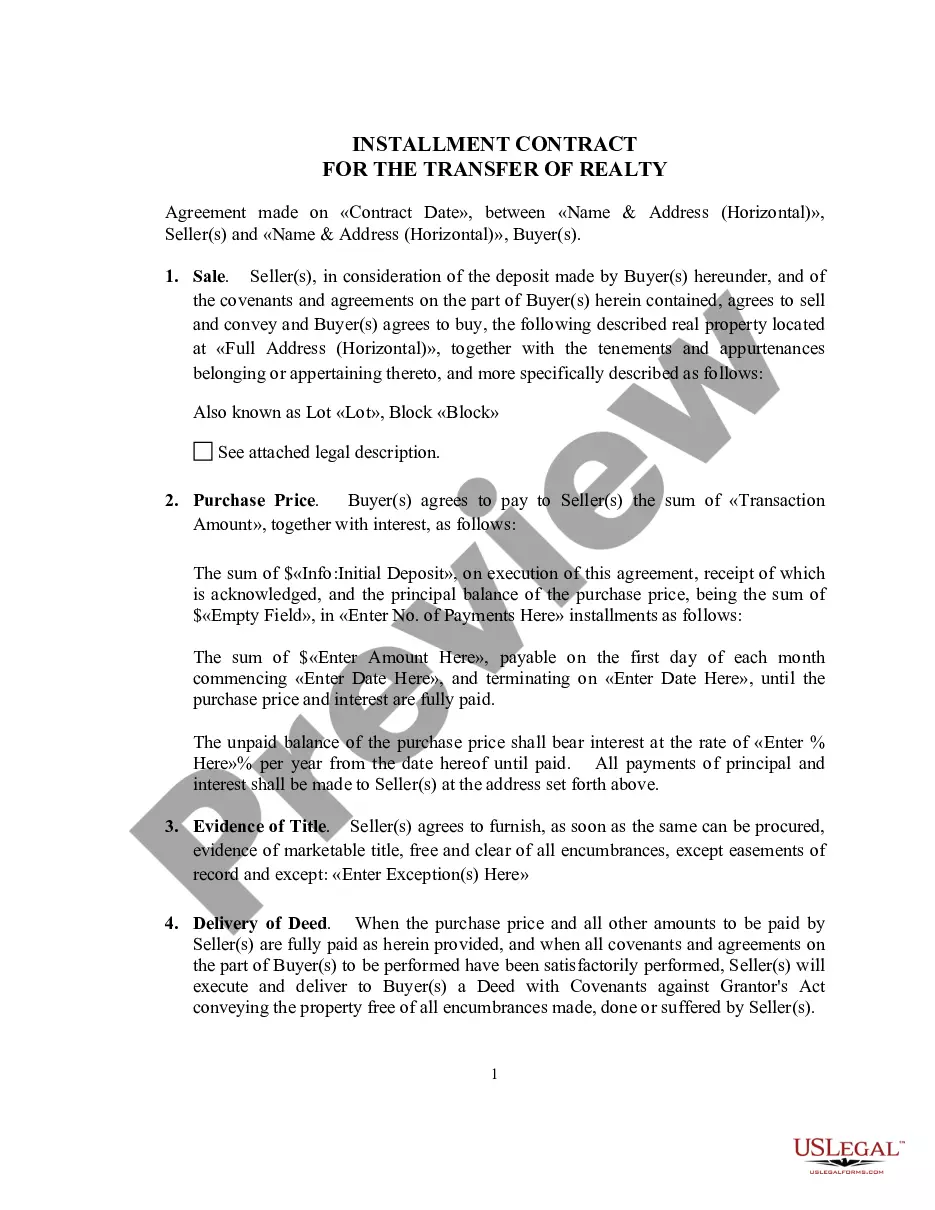

Closed-end transactions involve a fixed amount to be paid back over a period of time such as a note or a retail installment contract.

Kentucky General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Category:

State:

Multi-State

Control #:

US-02514BG

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures?

It is feasible to invest hours online striving to locate the sanctioned document template that conforms to the state and federal requirements you need.

US Legal Forms offers a wide array of legal forms that have been reviewed by professionals.

It is easy to acquire or print the Kentucky General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures from your service.

If available, use the Preview option to review the document template as well.

- If you have a US Legal Forms account, you can sign in and select the Download option.

- After that, you can complete, modify, print, or sign the Kentucky General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

- Every legal document template you purchase is yours indefinitely.

- To obtain an additional copy of any purchased form, visit the My documents section and select the appropriate option.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure you have chosen the correct document template for the area/town of your choice.

- Check the form details to ensure you have selected the correct form.

Form popularity

FAQ

TILA requires several essential disclosures, including the APR, the total amount financed, and the total payment amount for loans. It also mandates the disclosure of the payment schedule and any fees associated with the transaction. Reviewing these Kentucky General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures can enhance your comprehension of your financial commitments.

Reg Z requires lenders to provide clear disclosures about the terms of installment loans. This includes information about the annual percentage rate (APR), finance charges, total payments, and payment schedule. Understanding these Kentucky General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures can help you make informed financial decisions.

For open-end loans, the disclosures required include information about the annual percentage rate, terms of payment, and any fees involved. Lenders must inform borrowers about these aspects to comply with the Kentucky General Disclosures Required By The Federal Truth In Lending Act. This gives borrowers clarity when using revolving credit facilities. Finding resources and templates on uslegalforms can simplify the process of creating compliant disclosures.

Regulation Z implements the Truth in Lending Act and outlines the requirements for closed-end credit transactions. It aims to protect consumers by requiring lenders to disclose important details about credit terms. This regulation ensures that all material facts regarding closed-end credit agreements, such as interest rates and fees, are transparent and accessible to borrowers.

Lenders must provide a Truth in Lending (TIL) disclosure statement that includes information about the amount of your loan, the annual percentage rate (APR), finance charges (including application fees, late charges, prepayment penalties), a payment schedule and the total repayment amount over the lifetime of the loan.

Regulation Z also requires mortgage lenders to provide borrowers with a written disclosure of rates, fees and other finance charges. Plus, if you have an adjustable-rate mortgage, they're required to let you know in advance if your rate will be changing.

In any closed-end credit transaction, TILA requires disclosure of the total finance charge, which is the sum of all charges, expressed as a dollar amount, that meet the regulatory definition of finance charge.

Lenders must provide a Truth in Lending (TIL) disclosure statement that includes information about the amount of your loan, the annual percentage rate (APR), finance charges (including application fees, late charges, prepayment penalties), a payment schedule and the total repayment amount over the lifetime of the loan.

Sample disclosures required under TILA include:Annual percentage rate.Finance charges.Payment schedule.Total amount to be financed.Total amount made in payments over the life of the loan.