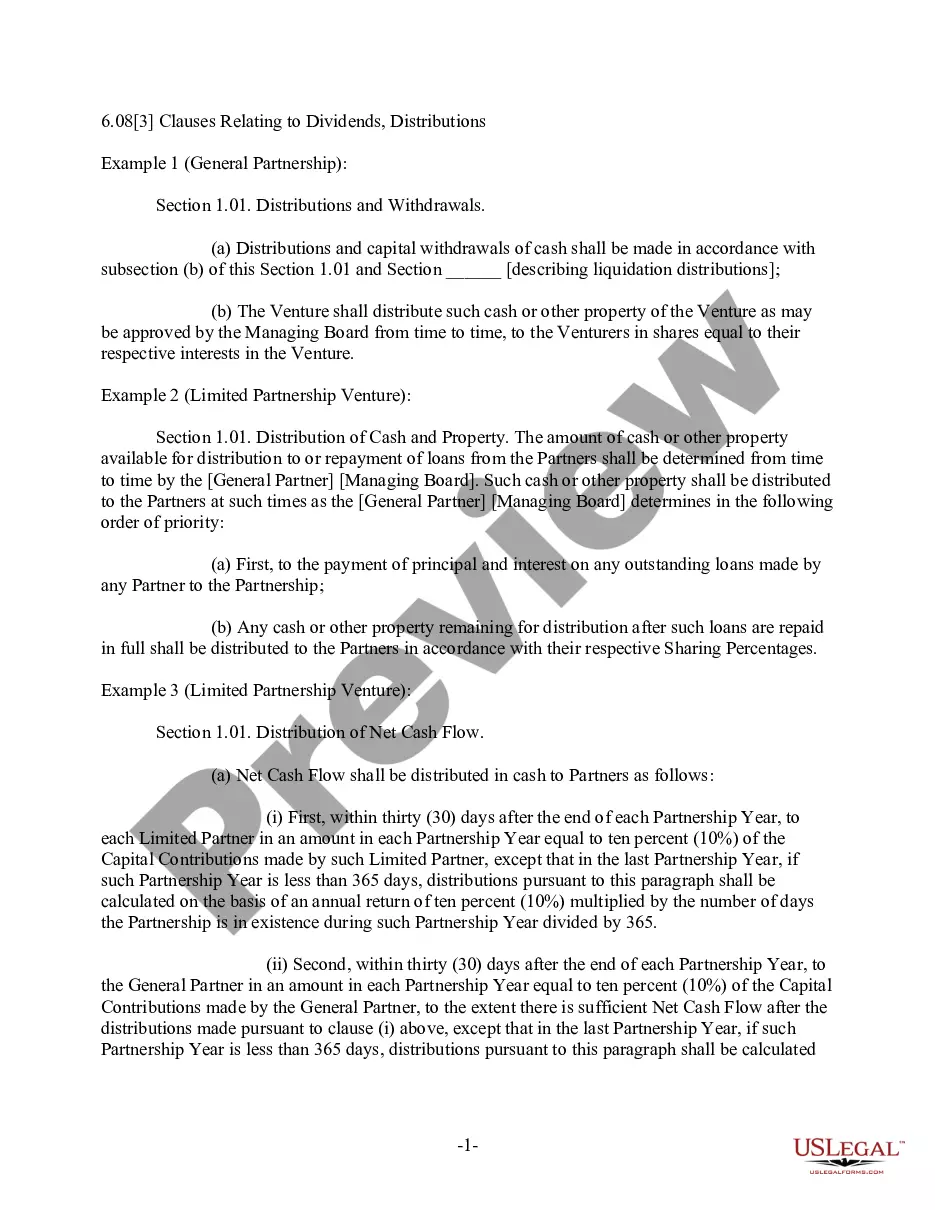

Kansas Clauses Relating to Capital Withdrawals, Interest on Capital

Description

How to fill out Clauses Relating To Capital Withdrawals, Interest On Capital?

You may spend time on the web trying to find the authorized document template that suits the state and federal specifications you want. US Legal Forms offers 1000s of authorized varieties which are reviewed by specialists. It is simple to download or print the Kansas Clauses Relating to Capital Withdrawals, Interest on Capital from the support.

If you already possess a US Legal Forms account, you may log in and click the Down load button. Afterward, you may comprehensive, edit, print, or indication the Kansas Clauses Relating to Capital Withdrawals, Interest on Capital. Each and every authorized document template you acquire is yours eternally. To obtain an additional copy of the acquired kind, check out the My Forms tab and click the related button.

If you are using the US Legal Forms web site the first time, stick to the straightforward guidelines listed below:

- Very first, make sure that you have selected the correct document template for your area/city of your liking. See the kind information to make sure you have selected the right kind. If readily available, take advantage of the Preview button to check from the document template also.

- If you want to locate an additional version of the kind, take advantage of the Search industry to get the template that meets your needs and specifications.

- Upon having discovered the template you desire, click Acquire now to move forward.

- Pick the rates plan you desire, key in your references, and sign up for a free account on US Legal Forms.

- Comprehensive the transaction. You should use your credit card or PayPal account to fund the authorized kind.

- Pick the file format of the document and download it in your product.

- Make adjustments in your document if needed. You may comprehensive, edit and indication and print Kansas Clauses Relating to Capital Withdrawals, Interest on Capital.

Down load and print 1000s of document web templates using the US Legal Forms website, which offers the greatest assortment of authorized varieties. Use expert and express-particular web templates to take on your small business or specific demands.

Form popularity

FAQ

Profits interests are generally preferable from a tax perspective, as there is no tax liability at the time the interest is granted, whereas a capital interest can result in immediate taxable compensation income for the service provider.

If the firm receives interest on partner drawings, it is taxable in the firm's hands. When it is stated that remuneration or interest is not permitted, it means that it is not permitted as a deduction when calculating net taxable profit.

12% Interest on Partner's Capital: Interest payment must be authorized/approved in the partnership deed. The rate of interest paid should not exceed 12%. If the amount of interest exceeds 12% of the capital, the excess amount is disallowed. Partner's Remuneration And How It Is Calculated? - ClearTax cleartax.in ? partner-remuneration-taxation cleartax.in ? partner-remuneration-taxation

Interest on Partner's Capital The rate of interest should not exceed 12%. If the amount of interest exceeds 12% of the capital then such excess amount is disallowed. It is not allowed if the tax is paid on presumptive basis under section 44AD or section 44ADA. Remuneration and Interest to Partner ? Section 40b - TaxAdda taxadda.com ? remuneration-and-interest-to-partn... taxadda.com ? remuneration-and-interest-to-partn...

Corporations which elect under subchapter S of the Internal Revenue Code not to be taxed as a corporation must file a Kansas Partnership or S Corporation Return (Form K-120S). All other corporations must file a Form K-120. K-120S Partnership or S Corporation Income Return (Rev. 7-11) ksrevenue.gov ? pdf ksrevenue.gov ? pdf

In determining gain or loss on sale of a partnership interest, taxpayers are often surprised to find they have a taxable gain. For income tax purposes gain or loss is the difference between the amount realized and adjusted basis of the partnership interest in the hands of the partner.

The Ending capital account represents the monetary investment ?left? in their account after all the increases (money contributed and profits reported) and decreases (money taken out and losses reported). What does "Ending Capital" mean in a K-1 for a Partnership/LLC filing an ... qbkaccounting.com ? what-does-ending-capital-m... qbkaccounting.com ? what-does-ending-capital-m...

The partners are paid interest on the capital that remains outstanding. The maximum rate of interest that can be paid to the owners is 12% as per the Income Tax Act u/s 40(b). If a partner introduces any further capital to the business then the additional capital is also taken into account for providing interest.