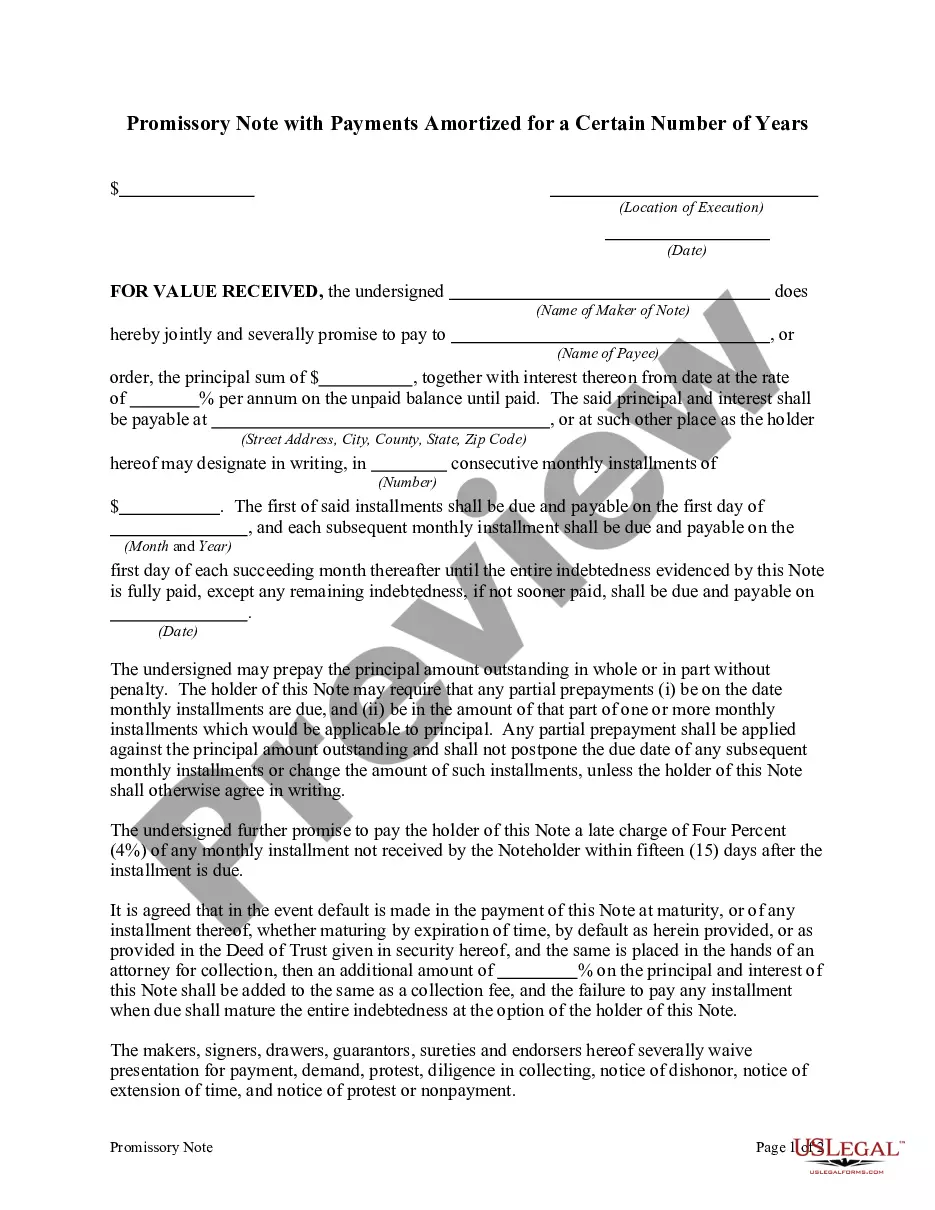

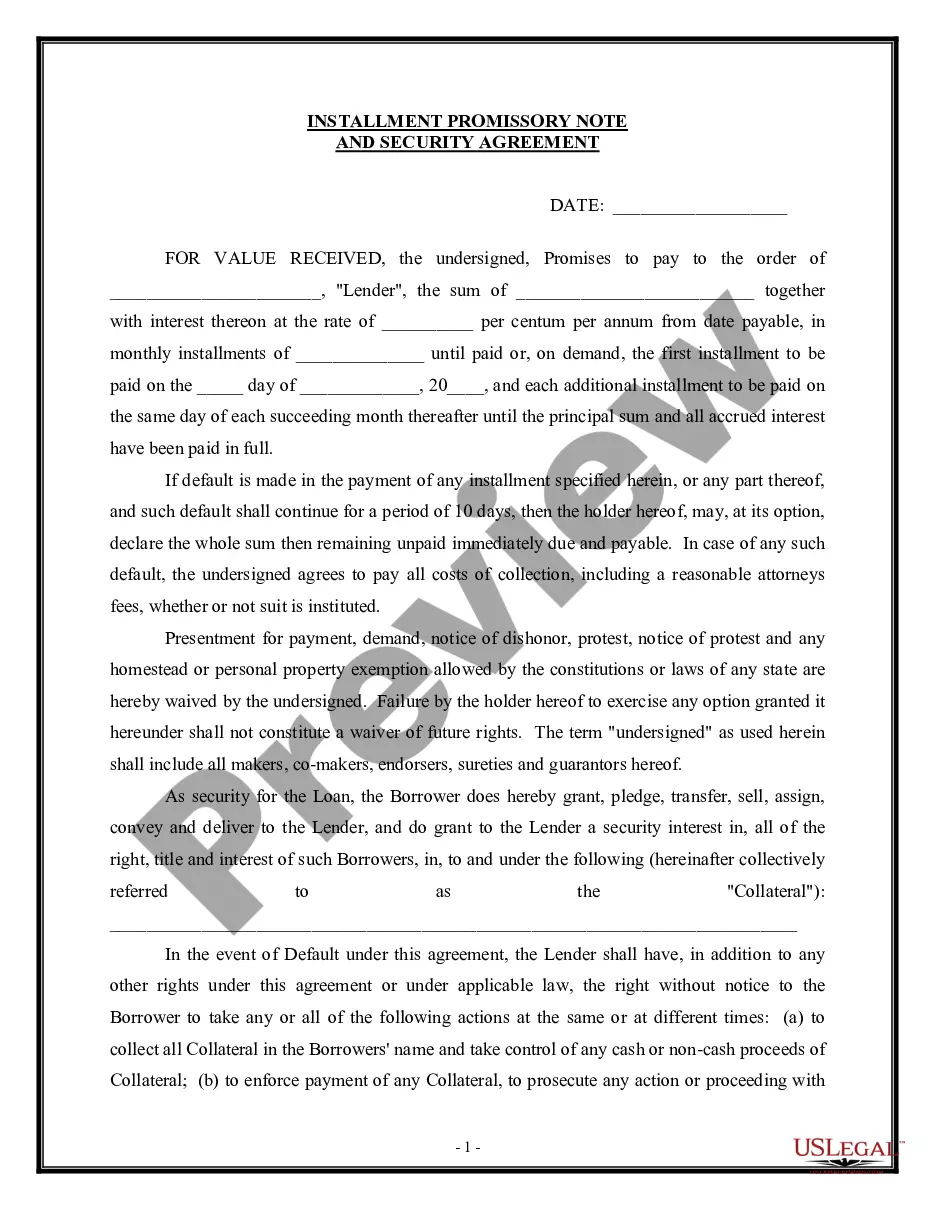

This form is a Promissory Note. The form provides that the borrower promises to pay the lender in monthly installments. The agreement also provides that there will not be a pre-payment penalty on the note.

Indiana Promissory Note with Installment Payments

Category:

State:

Multi-State

Control #:

US-00598

Format:

Word;

Rich Text

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Promissory Note With Installment Payments?

It is feasible to invest numerous hours online searching for the legal document format that complies with the state and federal regulations you need.

US Legal Forms offers a vast array of legal forms that can be reviewed by experts.

You can obtain or print the Indiana Promissory Note with Installment Payments from this service.

If you are using the US Legal Forms website for the first time, follow the simple instructions below: First, ensure that you have selected the correct document format for the area/city of your choice.

- If you possess a US Legal Forms account, you can Log In and click the Acquire button.

- Subsequently, you may complete, modify, print, or sign the Indiana Promissory Note with Installment Payments.

- Every legal document format you obtain is yours permanently.

- To get an additional copy of any form you purchased, go to the My documents section and click the appropriate button.

Form popularity

FAQ

When creating an Indiana Promissory Note with Installment Payments, it is crucial to include specific elements such as the principal amount, interest rate, repayment schedule, and signatures of both parties. This document must clearly state the terms to avoid any potential future disputes. Additionally, ensure that all parties understand their rights and obligations under the note. Following state laws will help enforce the agreement effectively.

To record a promissory note payment, you first need to maintain a detailed ledger. Each payment should be noted with the date, amount, and outstanding balance. This practice helps both parties track payment history, promoting transparency regarding the Indiana Promissory Note with Installment Payments. Consider utilizing platforms like US Legal Forms to access templates and resources for managing your records efficiently.

The main purpose of a promissory note is to establish a clear agreement between a lender and a borrower regarding repayment terms. It acts as a legally binding document that outlines the amount borrowed, interest rates, and payment schedules. With an Indiana Promissory Note with Installment Payments, both parties benefit from having a formal record, reducing the likelihood of misunderstandings. Overall, this document fosters trust and transparency in financial transactions.

Promissory notes come in various types, including demand notes, installment notes, and secured notes. A specific variant, the Indiana Promissory Note with Installment Payments, is a common choice for structured repayments over time. Each type serves different needs; for instance, demand notes require full repayment upon request, while installment notes allow for periodic payments. Understanding these distinctions helps borrowers choose the right note for their financial situation.

An installment promissory note is a type of agreement where repayments occur in fixed installments over a designated time frame. This format allows borrowers to manage their repayments more effectively, as each installment typically includes both principal and interest components. In Indiana, an Indiana Promissory Note with Installment Payments provides legal protection and clarity for both parties involved. This ensures that borrowers understand their obligations and lenders have a formal record of the agreement.

A prepayment may be allowed by a promissory note. A prepayment provision would allow you, as a borrower, to pay a debt early without paying an extra premium payment or penalty. It can consist of the unpaid accrued interest and the unpaid principal sum as of the date of prepayment.

An installment note is a form of promissory note calling for payment of both principal and interest in specified amounts, or specified minimum amounts, at specific time intervals.

Such an early release of a promissory note without full payment may be considered by the Internal Revenue Service ( IRS) to be a taxable event. The value of the amount of debt forgiven may be deemed either taxable income, or a gift subject to the federal estate and gift tax.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.