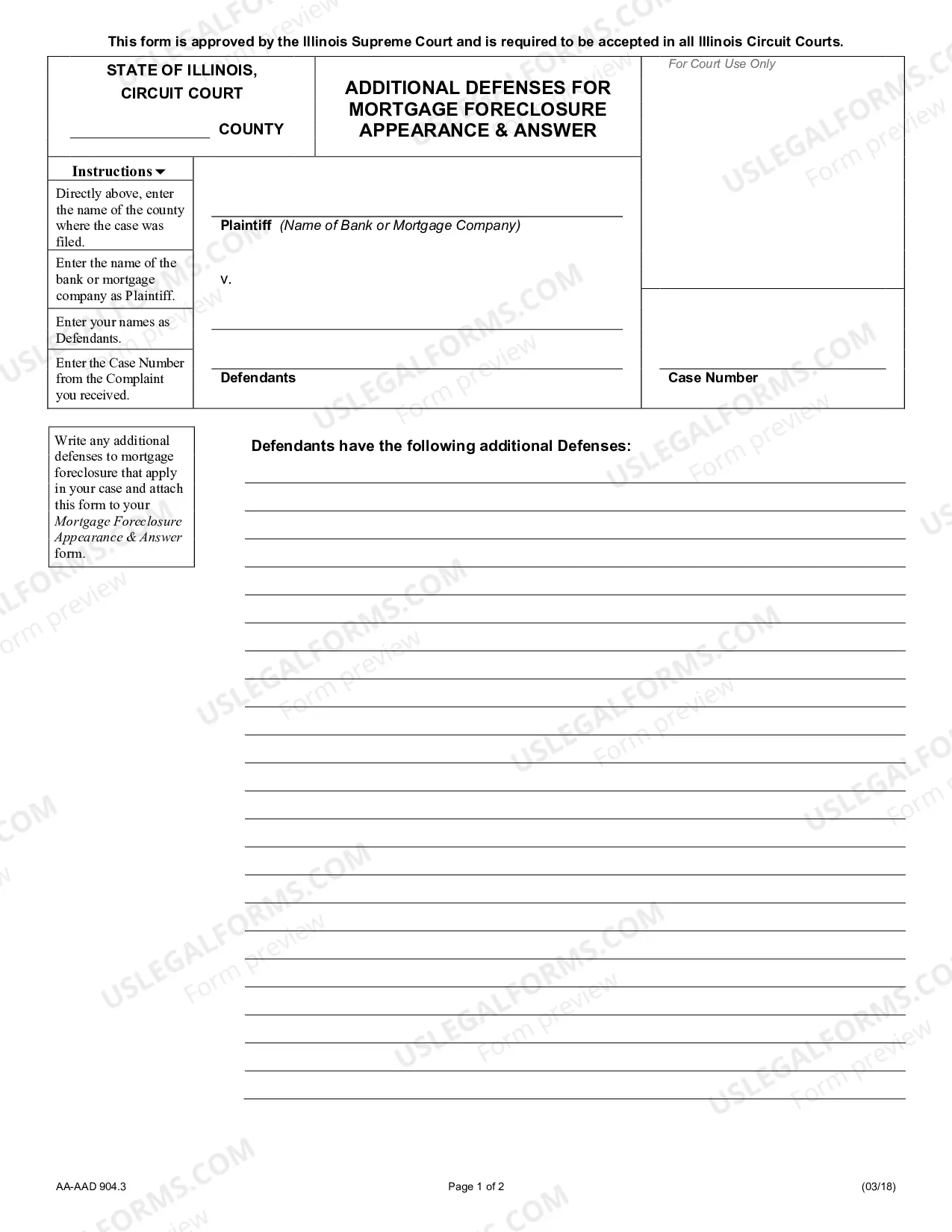

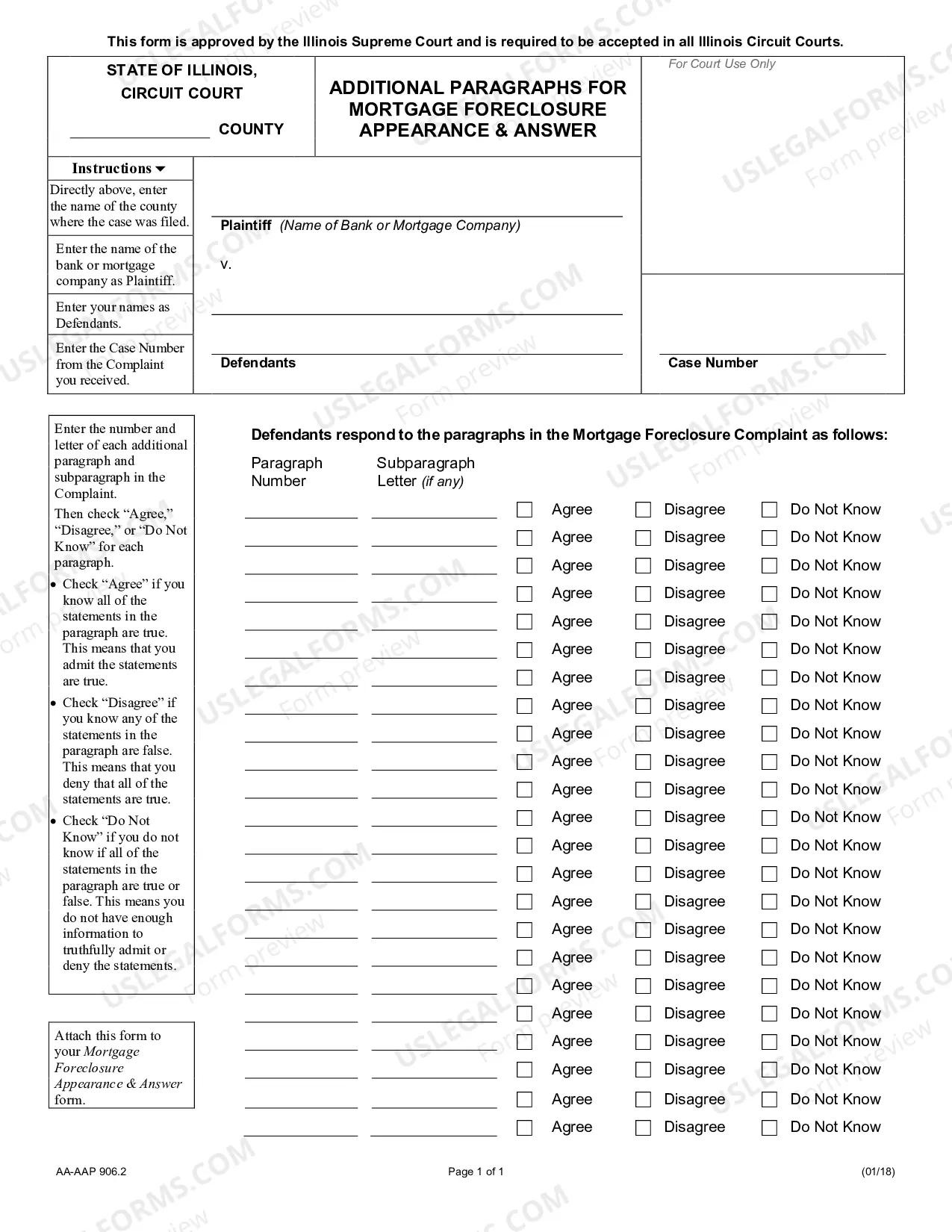

Illinois Additional Defenses for Mortgage Foreclosure Appearance & Answer is a legal document that a mortgagor (borrower) may file with the court when they are facing foreclosure. This document is used to raise certain defenses to the foreclosure proceedings, such as challenging the validity of the mortgage or the enforceability of the underlying debt. The document must be filed in the county where the mortgage was executed and must be served upon the lender. Types of Illinois Additional Defenses for Mortgage Foreclosure Appearance & Answer include: 1. Challenge to Validity of Mortgage — This is a defense to foreclosure based on the assertion that the mortgage was not validly executed, that it was obtained by fraud or duress, or that it was otherwise invalid. 2. Challenge to Enforceability of Underlying Debt — This is a defense to foreclosure based on the assertion that the underlying debt is not enforceable, such as when the debt is discharged in bankruptcy or when the lender has failed to comply with applicable state laws. 3. Challenge to Notice of Default — This is a defense to foreclosure based on the assertion that the lender failed to provide proper notice of the default to the mortgagor. 4. Challenge to Acceleration — This is a defense to foreclosure based on the assertion that the lender improperly accelerated the mortgage by demanding all unpaid amounts due immediately. 5. Challenge to Amounts Due — This is a defense to foreclosure based on the assertion that the amount of the debt claimed by the lender is incorrect. 6. Challenge to Standing — This is a defense to foreclosure based on the assertion that the lender is not the proper party to bring the foreclosure action, such as when the debt has been assigned to another entity.

Illinois Additional Defenses for Mortgage Foreclosure appearance & answer

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Illinois Additional Defenses For Mortgage Foreclosure Appearance & Answer?

Handling official documentation necessitates focus, precision, and utilizing properly crafted templates. US Legal Forms has been assisting individuals nationwide with this for 25 years, so when you select your Illinois Additional Defenses for Mortgage Foreclosure appearance & answer template from our platform, you can be assured it adheres to federal and state regulations.

Utilizing our platform is straightforward and efficient. To acquire the required paperwork, all you need is an account with an active subscription. Here’s a concise guide for you to secure your Illinois Additional Defenses for Mortgage Foreclosure appearance & answer in just a few moments.

All documents are prepared for multiple uses, such as the Illinois Additional Defenses for Mortgage Foreclosure appearance & answer you see on this page. If you require them in the future, you can complete them without repaying - simply access the My documents tab in your profile and finalize your document anytime you need it. Try US Legal Forms and efficiently complete your business and personal documentation in full legal compliance!

- Ensure to thoroughly review the form content and its alignment with general and legal standards by previewing it or perusing its description.

- Seek an alternative official template if the previously accessed one doesn’t align with your circumstances or state laws (the option for that is located at the top page corner).

- Log in to your account and download the Illinois Additional Defenses for Mortgage Foreclosure appearance & answer in the format of your choice. If it’s your first experience with our platform, click Buy now to move forward.

- Create an account, choose your subscription plan, and pay using your credit card or PayPal account.

- Decide in which format you want to receive your form and click Download. Print the template or incorporate it into a professional PDF editor for a paperless submission.

Form popularity

FAQ

A "reinstatement" occurs when the borrower brings the delinquent loan current in one lump sum. Reinstating a loan stops a foreclosure because the borrower catches up on the defaulted payments. The borrower also has to pay any overdue fees and expenses incurred because of the default.

A mortgage reinstatement could help to stabilize your homeownership claims. Although this is a great option, you will not be able to negotiate the terms of your mortgage reinstatement with your lender.

In Illinois, it can take approximately 12-15 months for a foreclosure to be completed. Call your lender or a HUD-certified counseling agency as soon as you can. You miss your second payment. When your lender calls, it is important to pick up the phone and speak to your lender.

What is a reinstatement quote? A reinstatement quote is the document that tells you the total amount needed to reinstate your mortgage. You should have a reinstatement quote in writing before you send any money to the bank. Do not rely on any verbal reinstatement number given to you by a bank representative.

Right of redemption is a legal process that allows a delinquent mortgage borrower to reclaim their home or other property subject to foreclosure if they are able to repay their obligations in time.

The Illinois Mortgage Foreclosure Law provides for a specific right of reinstatement. In order to reinstate your loan, you must repay any missed payments and any costs and expenses required by the mortgage. You cannot be required to repay the amount of principal due as a result of the lender accelerating your loan.

In Illinois, there is a redemption period during which you have the legal right to pay off the total debt plus certain costs and interest and reclaim your property, even after a judgment of foreclosure. The property cannot be sold during the redemption period.

Subject to a few limited exceptions, you have 7 months from the date you are served to pay off your loan in full, either by refinancing the loan or by selling the house or by other means. This is called your right to redeem, and the 7-month period is called the redemption period. Sometimes you can have longer.