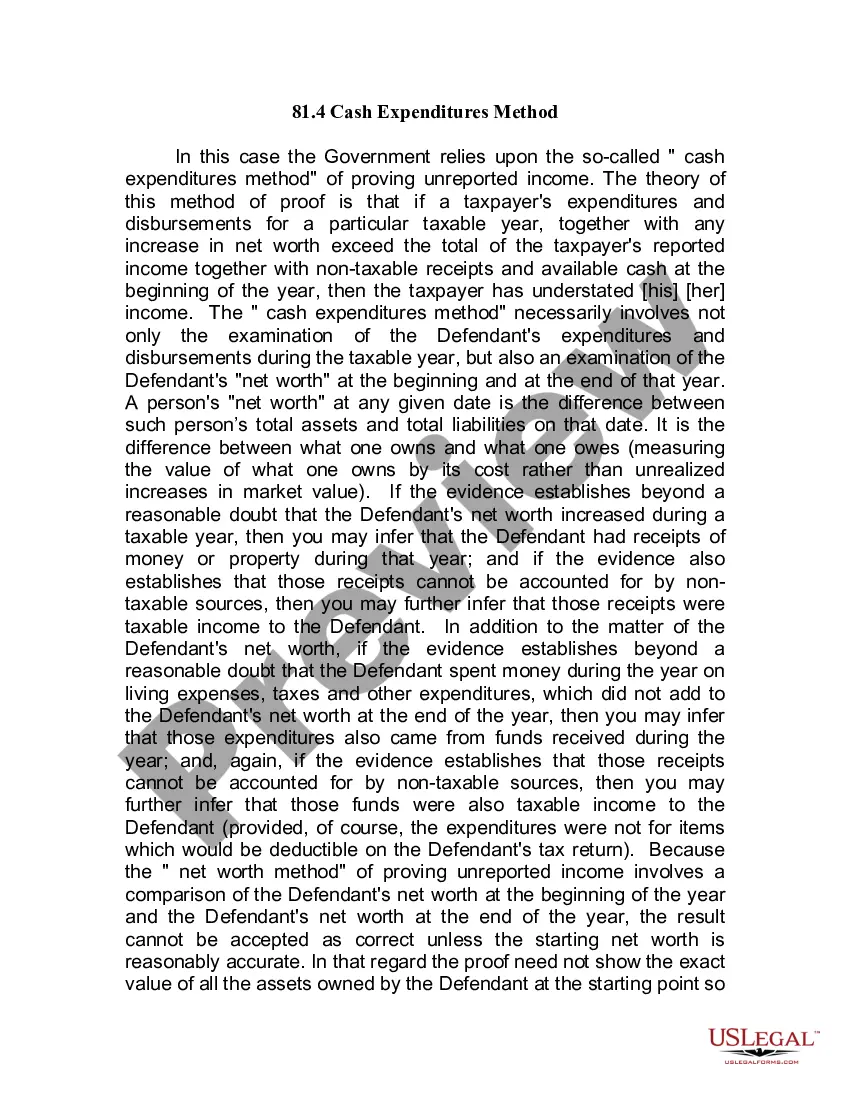

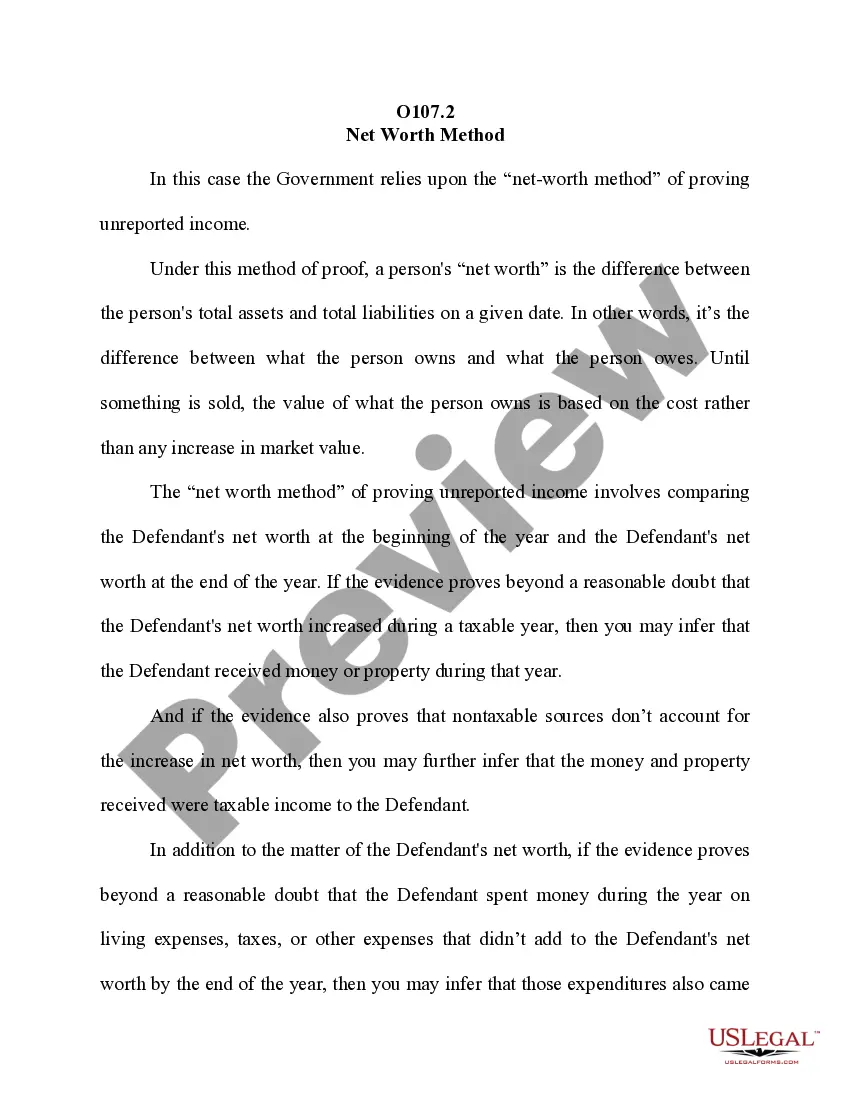

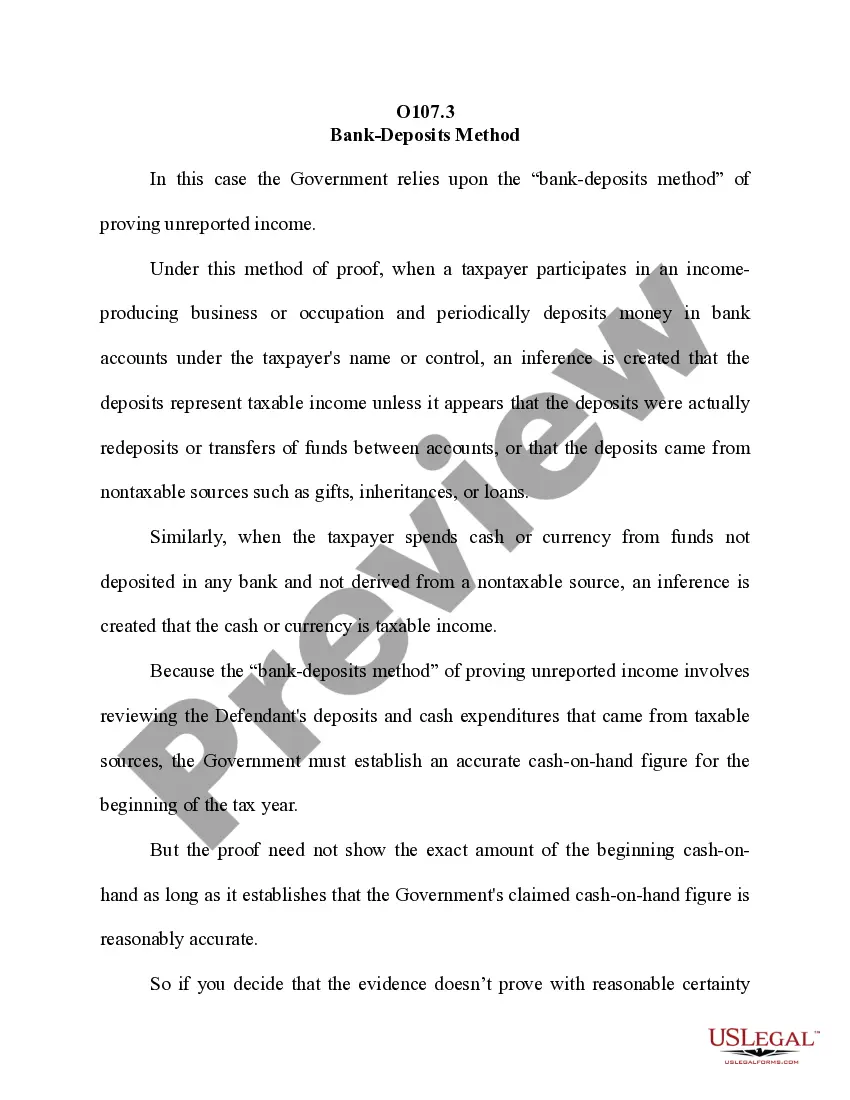

Cash Expenditures Method

About this form

The Cash Expenditures Method is a legal guideline used primarily in tax cases to prove unreported income. This method assesses a taxpayer's expenditures and net worth to determine if the reported income is accurate. Unlike traditional income documentation, this method infers income through the comparison of spending and net worth changes, making it a useful tool for government entities in tax enforcement cases.

Form components explained

- Definition of the cash-expenditures method used to establish unreported income.

- Clarification on how net worth is calculated, including assets and liabilities.

- Criteria for inferring income based on net worth increases and expenditures.

- Importance of investigating nontaxable income sources and leads suggested by the defendant.

- Requirement for the government to reasonably investigate claims made by the defendant.

- Standard of proof required to find the defendant guilty based on the cash-expenditures method.

Situations where this form applies

This form should be used in situations where there is suspicion of unreported income or tax evasion. It is commonly relevant in tax court cases, where the government must prove that a taxpayer's income has been understated based on their spending patterns and overall financial growth. The cash-expenditures method is particularly applicable when traditional documentation of income is limited or absent.

Who should use this form

- Tax professionals or attorneys involved in cases of alleged tax evasion.

- Government prosecutors handling tax fraud cases.

- Defendants in tax-related legal disputes, particularly those challenging income reports.

- Financial analysts involved in examining a taxpayer's financial history for compliance verifications.

How to complete this form

- Identify the tax year in question and gather all financial data for that year.

- Calculate the total expenditures and determine changes in net worth by comparing beginning and ending assets and liabilities.

- Evaluate if any increase in net worth aligns with reported income or can be attributed to nontaxable sources.

- Consider providing evidence that supports the taxpayer's claims or challenges about their financial situation.

- Document any reasonable leads or suggestions made by the defendant that should be investigated further.

Does this document require notarization?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to thoroughly investigate all leads suggested by the defendant.

- Overlooking certain nontaxable sources of income that can affect net worth calculations.

- Miscalculating the starting net worth, which can invalidate the case.

- Assuming that all expenditures are subject to the cash-expenditures method without proper justification.

Benefits of using this form online

- Immediate access to legal templates drafted by licensed attorneys.

- Editability allows tailoring the form to specific case needs without hassle.

- Reliability in using a standardized method that aligns with legal proceedings.

Legal use & context

- The cash-expenditures method is a legitimate method for authorities to prove tax evasion.

- It serves as a rebuttable presumption against the defendant, requiring them to provide evidence of their income sources.

What to keep in mind

- The Cash Expenditures Method is a critical tool for the government in enforcing tax laws.

- Taxpayers have the right to challenge the governmentâs claims through evidence and documentation.

- Understanding net worth and expenditures is essential for both taxpayers and their legal representatives.

Looking for another form?

Form popularity

FAQ

Unreported income: The IRS will catch this through their matching process if you fail to report income. It is required that third parties report taxpayer income to the IRS, such as employers, banks, and brokerage firms.

IRS reporting Once the IRS thinks that you owe additional tax on your unreported 1099 income, it will usually notify you and retroactively charge you penalties and interest beginning on the first day they think that you owed additional tax.

Reporting cash income It's not hard to report cash income when you file your taxes. All you'll need to do is include it when you fill out your Schedule C, which shows your business income and business expenses (and, as a result, your net income from self-employment).

The IRS receives information from third parties, such as employers and financial institutions. Using an automated system, the Automated Underreporter (AUR) function compares the information reported by third parties to the information reported on your return to identify potential discrepancies.

The direct method uses real-time figures and considers only cash flow to show actual payments and receipts. The indirect method adjusts net income with changes applied from non-cash transactions. Not commonly used. It is most appropriate for small businesses without significant cash transactions.

Through the expenditures method, the government will look for spending that exceeds an individual's reported taxable income in a specific tax year. If the expenditures exceed reported taxable income in a tax year, the excess is suspected to be unreported income.

Failing to file a tax return is classified as a misdemeanor and the most common outcome is the assessment of civil tax penalties against the taxpayer. That's not to say you still can't go to jail for it. The penalty is $25,000 for each year you failed to file.

When your tax return doesn't match income information the IRS has (like Forms W-2 and 1099), the IRS sends a notice. It's usually a CP2000 notice, also called an underreporter inquiry. This notice basically proposes taxes, and possibly penalties, you might owe for missing income on your return.