Iowa Breakdown of Savings for Budget and Emergency Fund

Description

How to fill out Breakdown Of Savings For Budget And Emergency Fund?

Locating the proper authorized document template can be a challenge.

It goes without saying, there are numerous designs accessible online, but how do you find the authorized form you require.

Utilize the US Legal Forms website. This service offers thousands of templates, including the Iowa Breakdown of Savings for Budget and Emergency Fund, which you can use for both professional and personal purposes.

- All forms are reviewed by experts and comply with federal and state regulations.

- If you are already registered, Log In to your account and hit the Download button to obtain the Iowa Breakdown of Savings for Budget and Emergency Fund.

- Leverage your account to browse through the legal documents you might have previously acquired.

- Visit the My documents tab in your account and retrieve another copy of the document you require.

- If you are a new user of US Legal Forms, here are straightforward steps to follow.

Form popularity

FAQ

5 Steps to Creating a BudgetStep 1: Determine Your Income. This amount should be your monthly take-home pay after taxes and other deductions.Step 2: Determine Your Expenses.Step 3: Choose Your Budget Plan.Step 4: Adjust Your Habits.Step 5: Live the Plan.

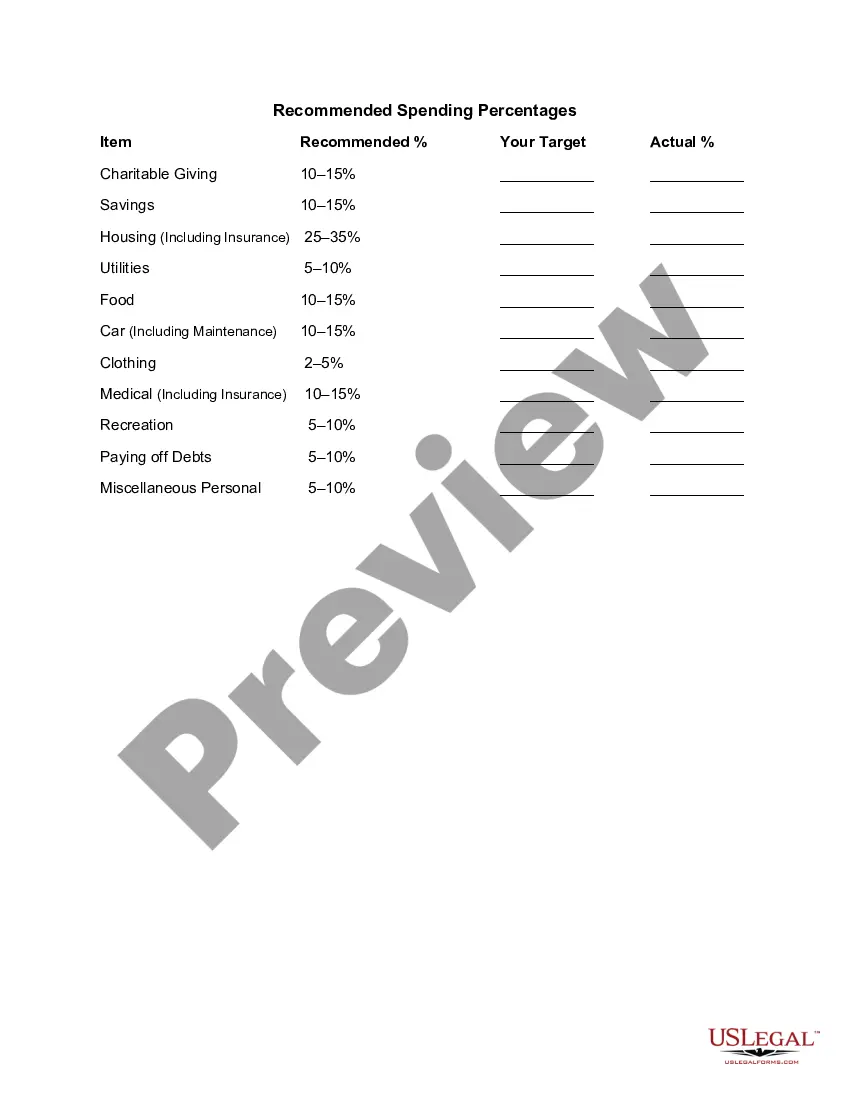

It recommends dividing your income in this way:50% - Spend for your needs. These include basic necessities like housing, food, utilities, health care (insurance, treatments), or car payments.30% - Spend for your wants.20% - Set aside for savings.

7 Steps to a Budget Made EasyStep 1: Set Realistic Goals.Step 2: Identify your Income and Expenses.Step 3: Separate Needs and Wants.Step 4: Design Your Budget.Step 5: Put Your Plan Into Action.Step 6: Seasonal Expenses.Step 7: Look Ahead.

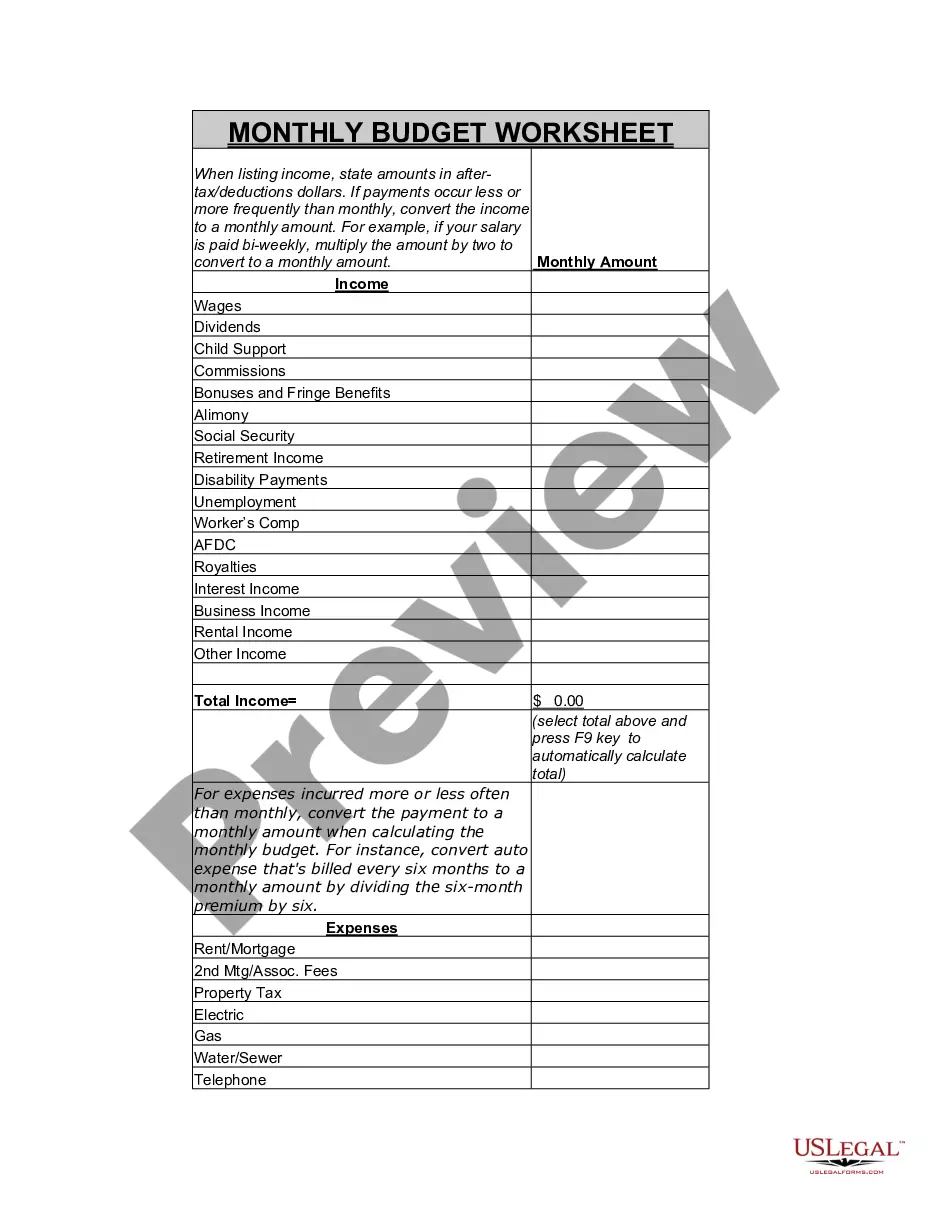

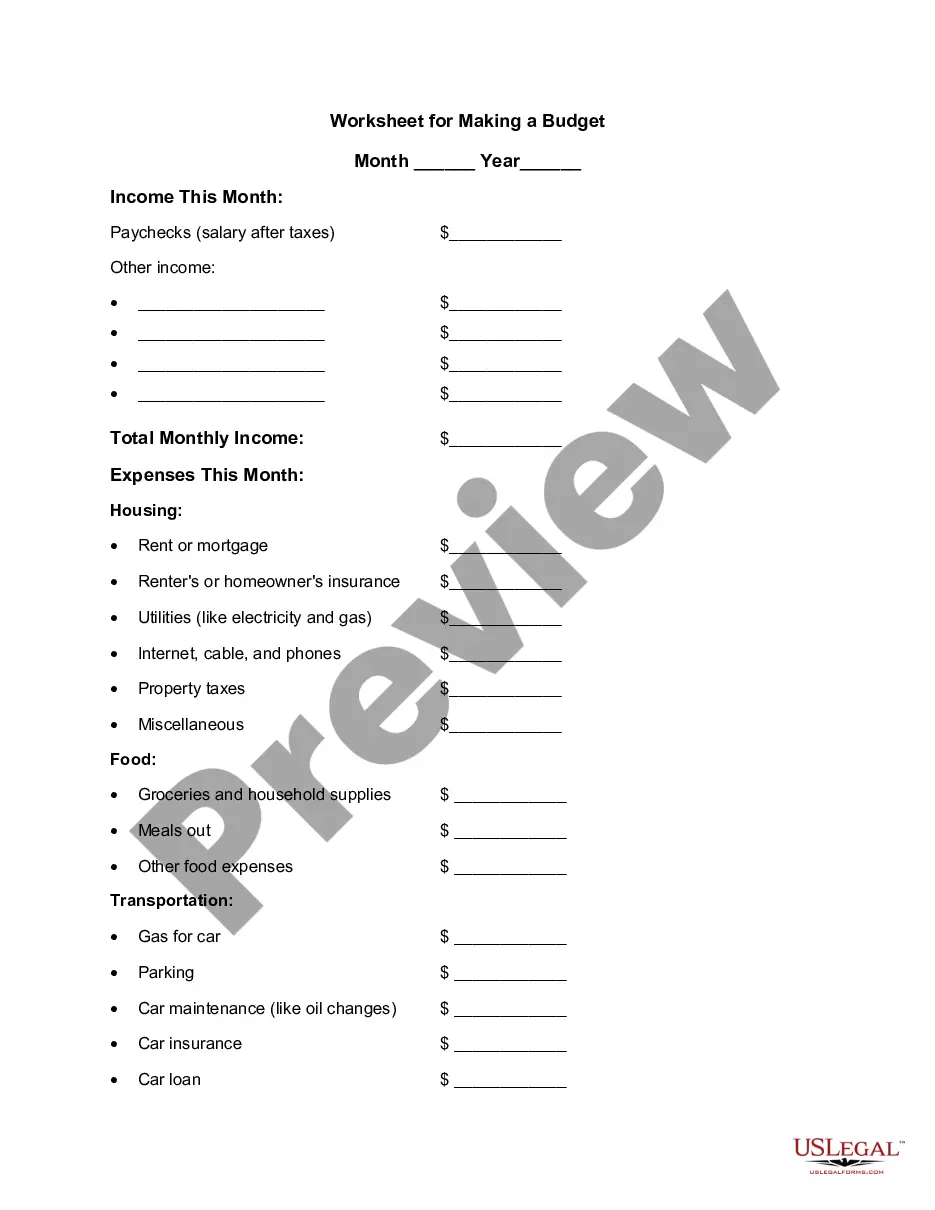

Creating a budgetStep 1: Calculate your net income. The foundation of an effective budget is your net income.Step 2: Track your spending.Step 3: Set realistic goals.Step 4: Make a plan.Step 5: Adjust your spending to stay on budget.Step 6: Review your budget regularly.

While the size of your emergency fund will vary depending on your lifestyle, monthly costs, income, and dependents, the rule of thumb is to put away at least three to six months' worth of expenses.

Senator Elizabeth Warren popularized the so-called "50/20/30 budget rule" (sometimes labeled "50-30-20") in her book, All Your Worth: The Ultimate Lifetime Money Plan. The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.

The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.

The 50/30/20 budget divides your after-tax income into three separate categories: 50% for needs, 30% for wants and 20% for savings/financial goals. This approach is best for younger, average-income earners who have paid off their high-interest debt.

If You Are Paid Bi-Weekly: Multiply your take-home pay for one paycheck by the number of paychecks in a year: 26. Then divide this number by 12 to get your monthly income. If You Are Paid Weekly: Take your weekly pay and multiply it by the number of weeks in a year: 52.