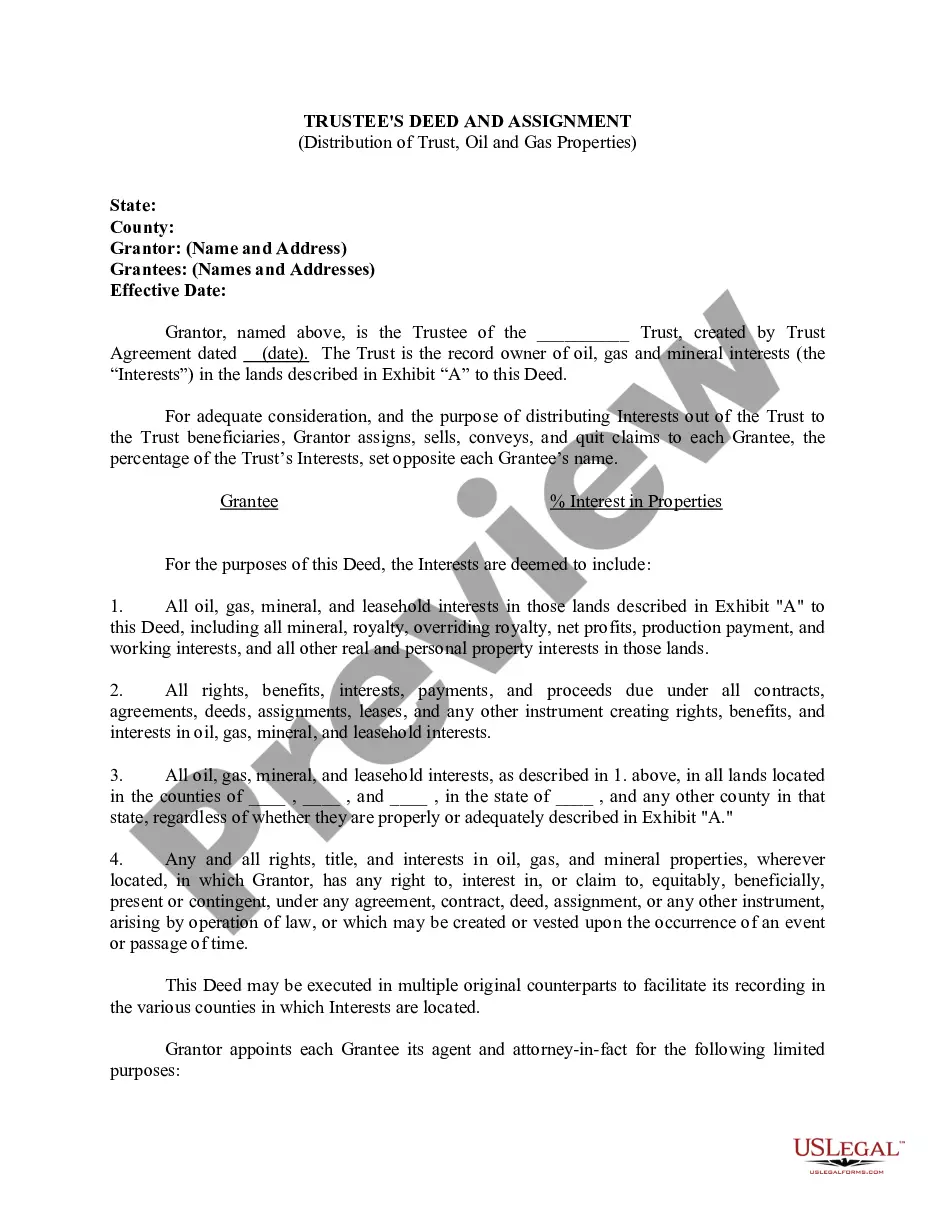

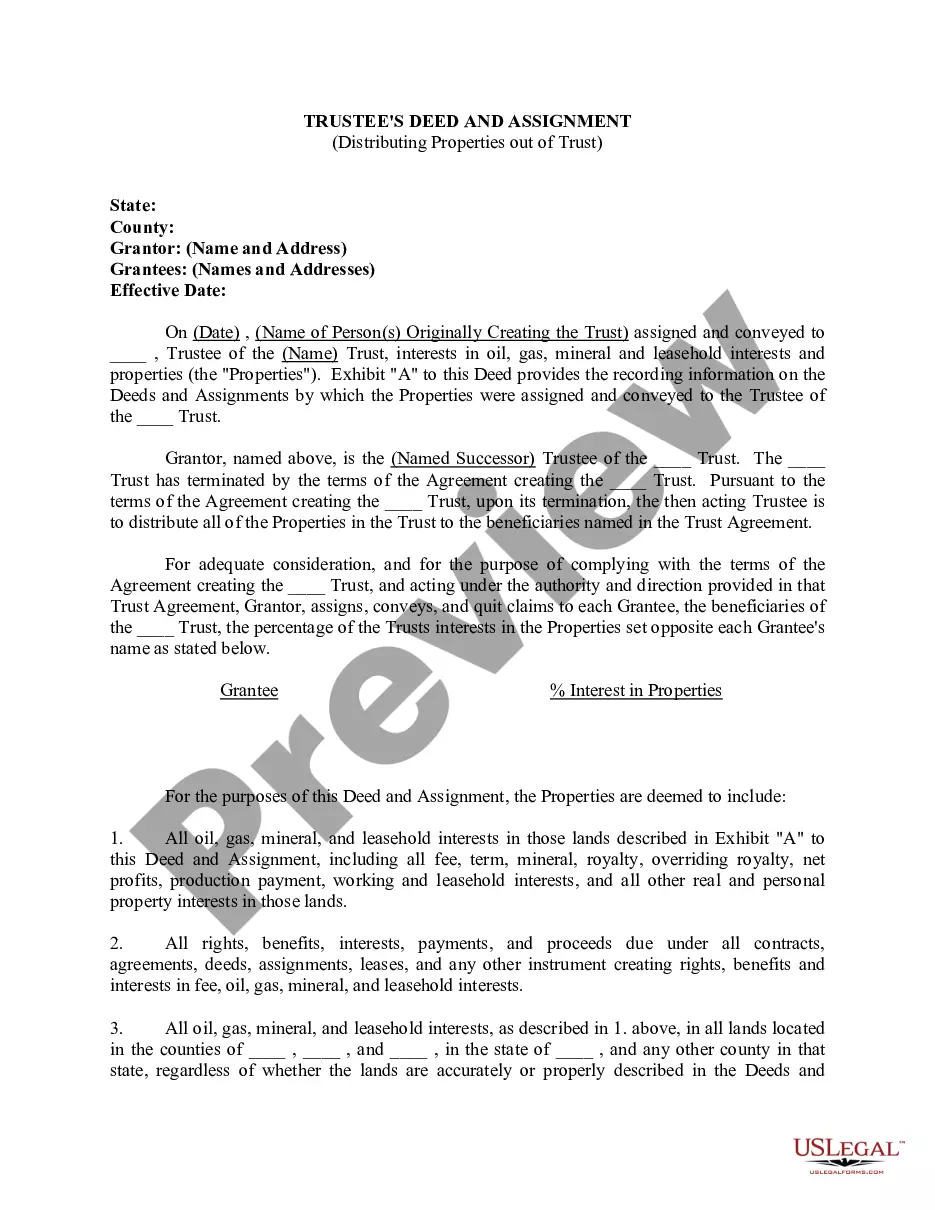

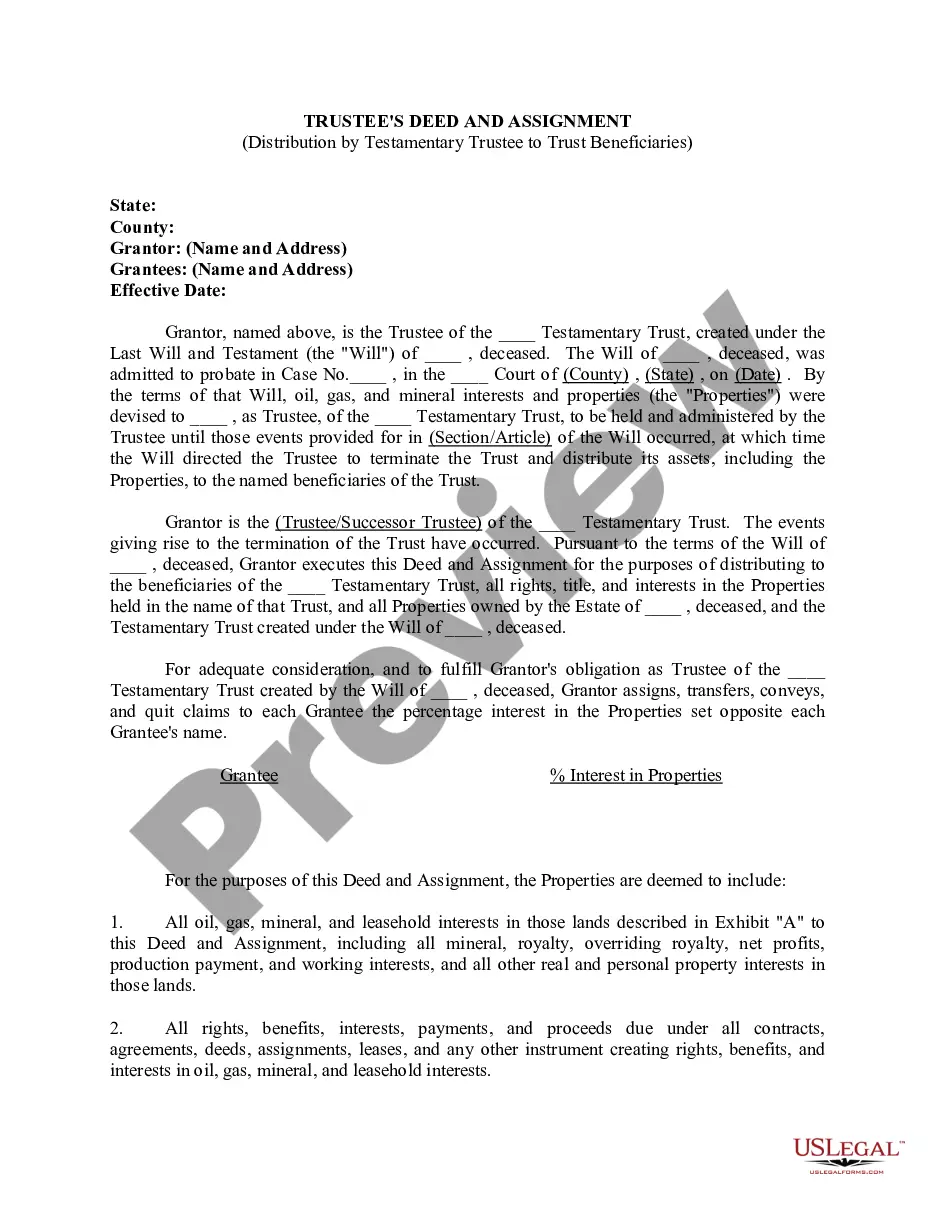

Connecticut Trustee's Deed and Assignment for Distribution by Trustee to Testamentary Trust Beneficiaries

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Trustee's Deed And Assignment For Distribution By Trustee To Testamentary Trust Beneficiaries?

You are able to commit hrs on the Internet trying to find the authorized record web template which fits the state and federal specifications you want. US Legal Forms gives 1000s of authorized varieties that are analyzed by experts. It is simple to down load or print out the Connecticut Trustee's Deed and Assignment for Distribution by Trustee to Testamentary Trust Beneficiaries from my assistance.

If you already have a US Legal Forms profile, you can log in and click on the Down load switch. Next, you can comprehensive, revise, print out, or signal the Connecticut Trustee's Deed and Assignment for Distribution by Trustee to Testamentary Trust Beneficiaries. Every authorized record web template you acquire is yours forever. To have another duplicate associated with a acquired type, proceed to the My Forms tab and click on the corresponding switch.

If you are using the US Legal Forms site initially, follow the basic guidelines listed below:

- Very first, make sure that you have chosen the right record web template for that region/town of your choice. See the type description to ensure you have picked the right type. If readily available, utilize the Preview switch to look from the record web template as well.

- If you wish to find another edition of the type, utilize the Search industry to discover the web template that suits you and specifications.

- After you have located the web template you need, click Purchase now to move forward.

- Pick the prices program you need, key in your references, and sign up for your account on US Legal Forms.

- Full the purchase. You can utilize your credit card or PayPal profile to cover the authorized type.

- Pick the file format of the record and down load it to the product.

- Make alterations to the record if needed. You are able to comprehensive, revise and signal and print out Connecticut Trustee's Deed and Assignment for Distribution by Trustee to Testamentary Trust Beneficiaries.

Down load and print out 1000s of record web templates making use of the US Legal Forms Internet site, which provides the most important selection of authorized varieties. Use specialist and state-certain web templates to tackle your small business or individual requires.

Form popularity

FAQ

Stocks and bonds can be transferred from the trust into the beneficiary's brokerage accounts. Beneficiaries typically have to pay taxes on trust income, except for distributions from the trust's principle.

The transferee must have been a beneficiary of the trust when the property was acquired and became an asset of the trust (i.e. the relevant time). There must be no consideration for the transfer and the transfer of property from trustee to beneficiary must not be part of a sale or other arrangement.

Yes, as a trustee, you can transfer stock from a trust to a beneficiary without selling it if the terms of the trust allow you to do so. If the trust instrument allows for the transfer of stock to a beneficiary, the trustee can transfer the stock as directed by the trust agreement.

During the transition, the beneficiaries are not the legal owners of the estate's assets. They are known as the ?beneficial owners.? This is a trust relationship. Once an estate is administered (all the bills are paid) the trustee ?vests? or transfers legal ownership of the assets to the beneficiaries.

The grantor can opt to have the beneficiaries receive trust property directly without any restrictions. The trustee can write the beneficiary a check, give them cash, and transfer real estate by drawing up a new deed or selling the house and giving them the proceeds.

When trust beneficiaries receive distributions from the trust's principal balance, they don't have to pay taxes on this disbursement. The Internal Revenue Service (IRS) assumes this money was taxed before being placed into the trust. Gains on the trust are taxable as income to the beneficiary or the trust.

Distribute trust assets outright The grantor can opt to have the beneficiaries receive trust property directly without any restrictions. The trustee can write the beneficiary a check, give them cash, and transfer real estate by drawing up a new deed or selling the house and giving them the proceeds.

Whether or not the trustee can withhold funds from you depends on the terms of the trust itself. If the trust requires withholding distributions under certain circumstances, such as the beneficiary reaching a specific age, the trustee must follow those stipulations.