Connecticut Sample Letter for Request for Removal of Derogatory Credit Information

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sample Letter For Request For Removal Of Derogatory Credit Information?

US Legal Forms - one of several biggest libraries of authorized forms in the USA - delivers a wide range of authorized document web templates you are able to download or printing. While using internet site, you will get 1000s of forms for business and individual functions, categorized by types, says, or search phrases.You will find the most recent variations of forms such as the Connecticut Sample Letter for Request for Removal of Derogatory Credit Information in seconds.

If you already possess a membership, log in and download Connecticut Sample Letter for Request for Removal of Derogatory Credit Information through the US Legal Forms collection. The Download switch will show up on each develop you look at. You get access to all formerly acquired forms in the My Forms tab of the bank account.

If you want to use US Legal Forms the very first time, listed here are straightforward directions to help you began:

- Make sure you have chosen the right develop for your metropolis/area. Go through the Review switch to analyze the form`s information. Look at the develop description to actually have selected the proper develop.

- In the event the develop does not satisfy your requirements, utilize the Look for industry towards the top of the screen to discover the one which does.

- In case you are pleased with the shape, verify your choice by clicking the Acquire now switch. Then, pick the rates plan you prefer and offer your qualifications to sign up for the bank account.

- Process the purchase. Make use of credit card or PayPal bank account to perform the purchase.

- Choose the formatting and download the shape on the gadget.

- Make alterations. Fill out, modify and printing and sign the acquired Connecticut Sample Letter for Request for Removal of Derogatory Credit Information.

Every web template you put into your bank account lacks an expiration particular date and it is your own property for a long time. So, if you wish to download or printing yet another backup, just proceed to the My Forms segment and click around the develop you will need.

Get access to the Connecticut Sample Letter for Request for Removal of Derogatory Credit Information with US Legal Forms, the most extensive collection of authorized document web templates. Use 1000s of specialist and state-certain web templates that meet your small business or individual demands and requirements.

Form popularity

FAQ

A 609 Dispute Letter is often billed as a credit repair secret or legal loophole that forces the credit reporting agencies to remove certain negative information from your credit reports. And if you're willing, you can spend big bucks on templates for these magical dispute letters.

Generally speaking, negative information such as late or missed payments, accounts that have been sent to collection agencies, accounts not being paid as agreed, or bankruptcies stays on credit reports for approximately seven years.

How to remove negative items from your credit report yourself Get a free copy of your credit report. ... File a dispute with the credit reporting agency. ... File a dispute directly with the creditor. ... Review the claim results. ... Hire a credit repair service. ... Send a request for ?goodwill deletion? ... Work with a credit counseling agency.

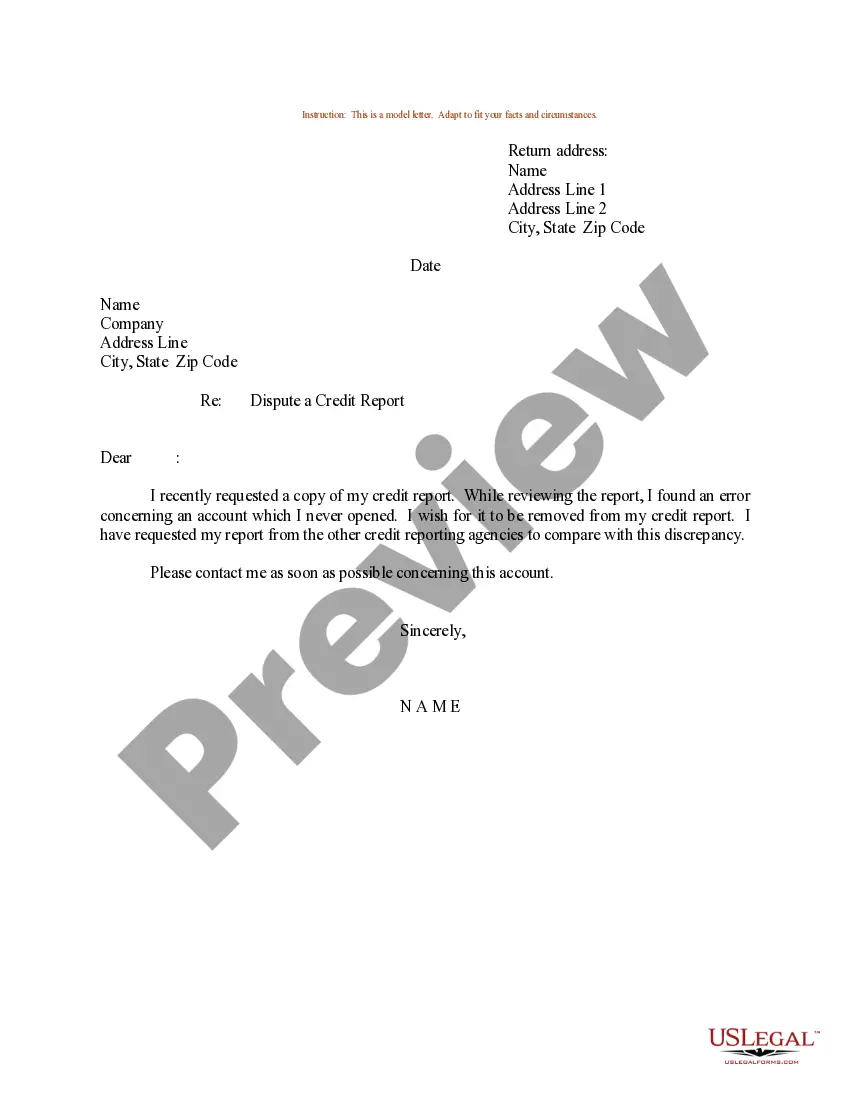

If the derogatory mark is in error, you can file a dispute with the credit bureaus to get negative information removed from your credit reports. You can see all three of your credit reports for free on a weekly basis. If the derogatory marks are not errors, you'll need to wait for them to age off your credit reports.

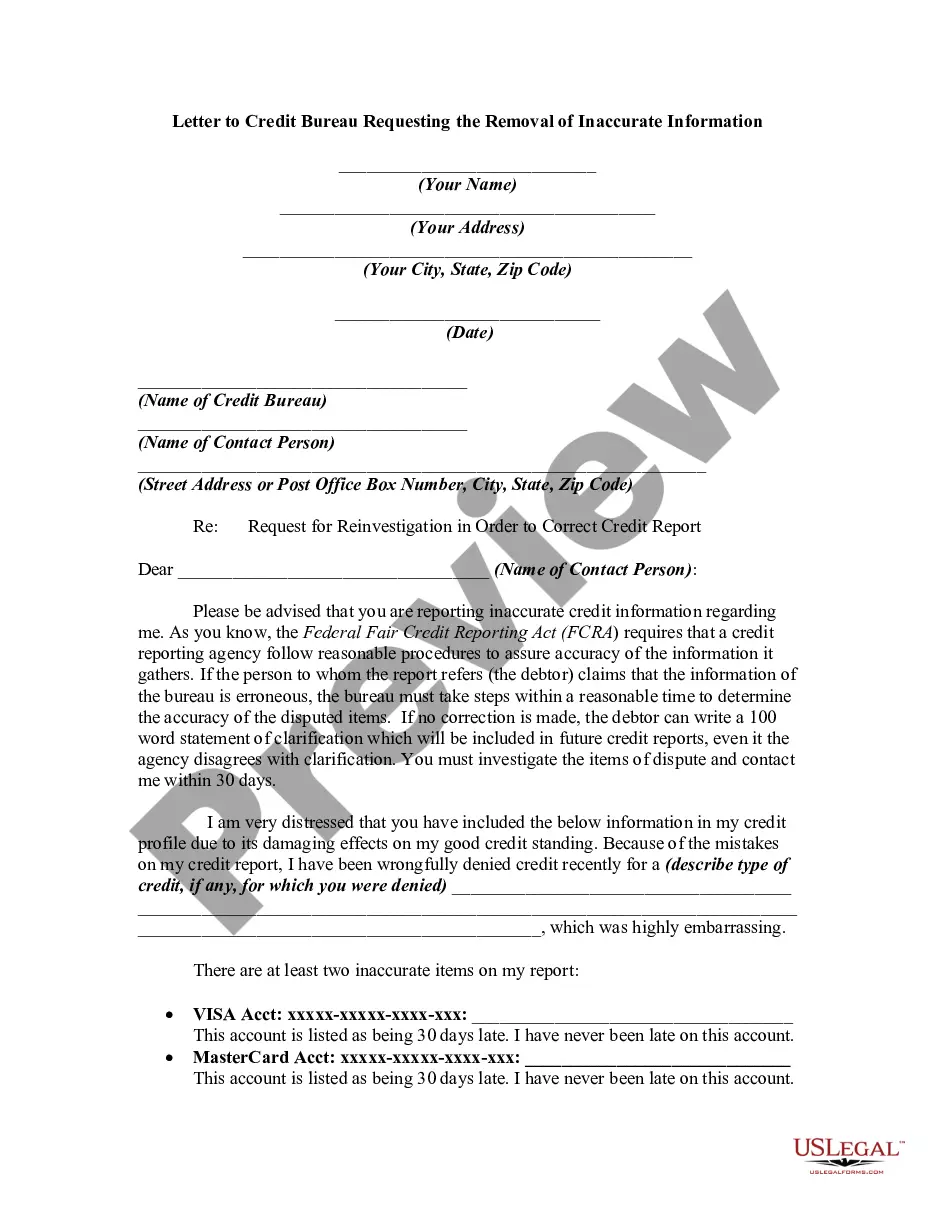

I am requesting that this item be removed [or request another specific change to correct the information]. [List and describe any other items you are disputing.] Enclosed is documentation supporting my request: [describe the documents you're sending, for instance: my credit report, with the disputed items circled.]

The following are important details to include in the goodwill letter: The date. Your name. Your address. Your creditor's name. Your creditor's address. Your account number. The negative mark you'd like removed. Which credit bureaus the mark needs to be removed from.

If you do have valid negative items on record, here are some things that might help: Send a request for ?goodwill deletion? Writing a goodwill letter can be a viable option for people who are otherwise in good standing with creditors. ... Work with a credit counseling agency. ... Negotiate a pay-for-delete.

Paying off collection accounts can raise credit scores calculated using FICO® Score 9 and 10 and VantageScore 3.0 and 4.0, but it won't have any effect on scores produced by older FICO scoring models.