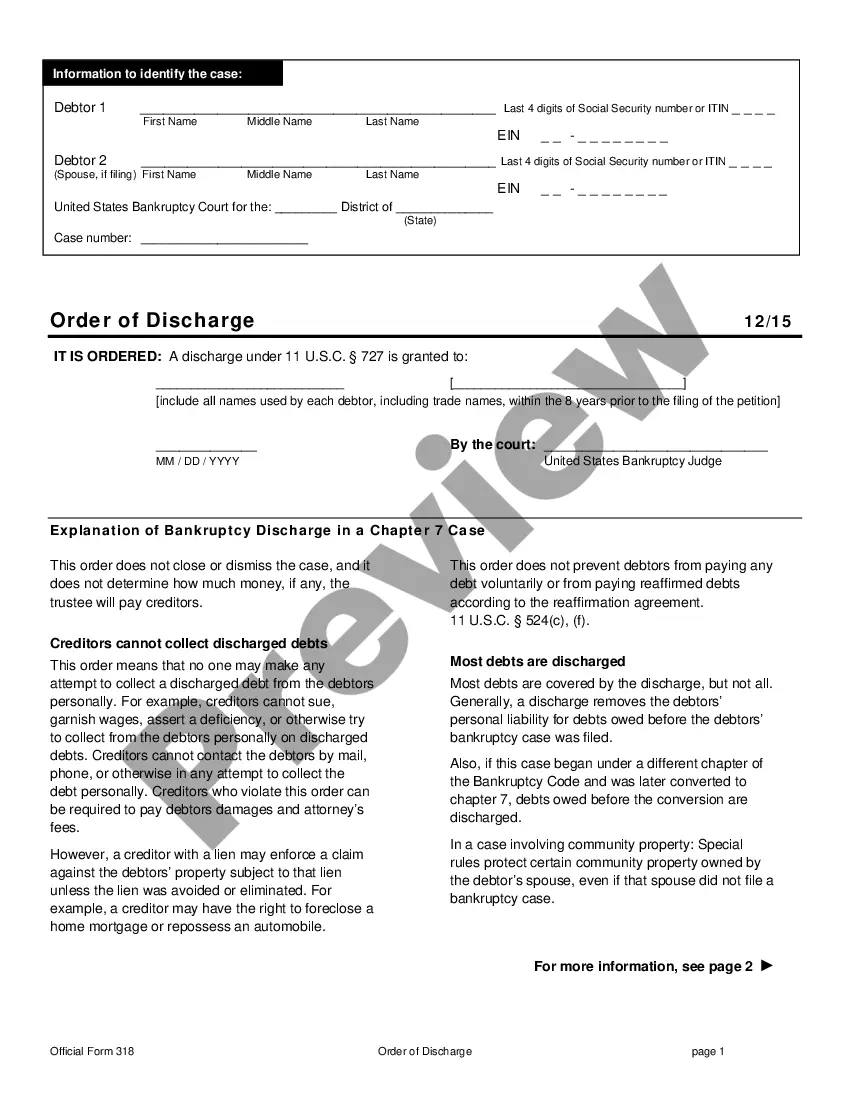

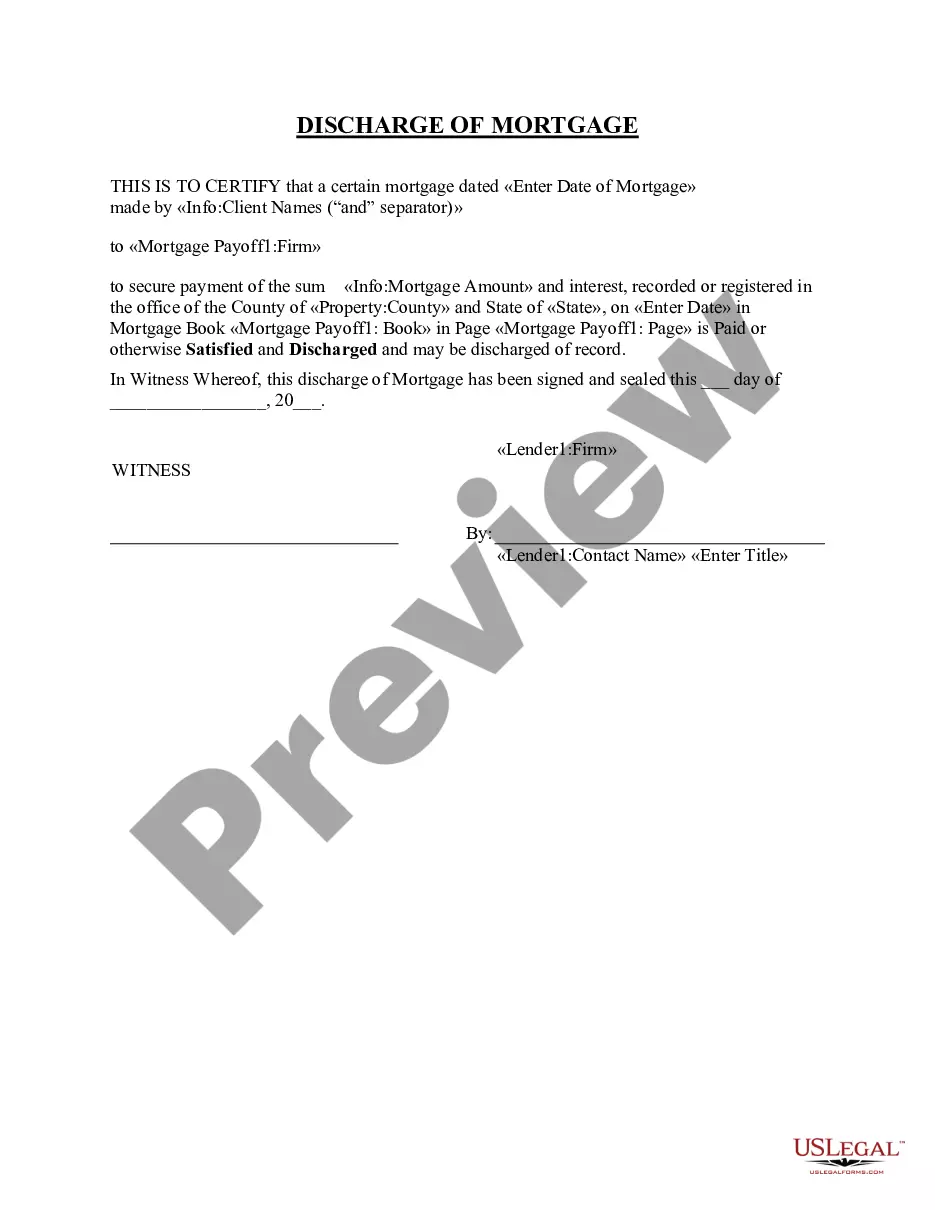

The form is a discharge of joint debtors. The debtors are granted a discharge pursuant to 11 U.S.C. section 727. The signature of the bankruptcy judge is required for this action.

California Discharge of Joint Debtors - Chapter 7 - updated 2005 Act form

Category:

State:

Multi-State

Control #:

US-B-18J

Format:

Word;

PDF;

Rich Text

Instant download

This website is not affiliated with any governmental entity

Public form

Description

How to fill out Discharge Of Joint Debtors - Chapter 7 - Updated 2005 Act Form?

Choosing the best legal papers format might be a struggle. Naturally, there are plenty of themes available on the net, but how would you obtain the legal kind you will need? Utilize the US Legal Forms website. The assistance provides a huge number of themes, including the California Discharge of Joint Debtors - Chapter 7 - updated 2005 Act form, that can be used for enterprise and private requirements. All the types are checked out by pros and meet state and federal demands.

When you are currently registered, log in to your bank account and then click the Obtain switch to have the California Discharge of Joint Debtors - Chapter 7 - updated 2005 Act form. Make use of your bank account to search with the legal types you may have purchased earlier. Visit the My Forms tab of the bank account and get yet another copy of your papers you will need.

When you are a brand new customer of US Legal Forms, listed here are straightforward directions that you can follow:

- Very first, be sure you have selected the correct kind to your metropolis/area. You may look over the form utilizing the Preview switch and browse the form explanation to make certain this is basically the right one for you.

- In the event the kind is not going to meet your needs, take advantage of the Seach field to get the appropriate kind.

- When you are certain that the form is acceptable, select the Acquire now switch to have the kind.

- Pick the costs strategy you would like and enter the required information and facts. Make your bank account and buy the transaction using your PayPal bank account or credit card.

- Opt for the submit structure and down load the legal papers format to your product.

- Full, change and print and signal the received California Discharge of Joint Debtors - Chapter 7 - updated 2005 Act form.

US Legal Forms is definitely the most significant collection of legal types in which you can discover numerous papers themes. Utilize the service to down load expertly-created files that follow status demands.

Form popularity

FAQ

In most cases, a Chapter 7 bankruptcy can stay on your credit reports for up to 10 years from the date you file bankruptcy. Once the 10-year period ends, the bankruptcy should fall off your credit reports automatically.

Generally speaking, Sabatini says, "Chapter 7 is less expensive than Chapter 13 and much faster. A Chapter 7 is usually over within about four months. A Chapter 13 takes at least three years. But for some consumers, Chapter 13 offers some relief that is not available in Chapter 7."

Courts can issue a discharge ruling when the debtor meets the discharge requirements under Chapter 7 or Chapter 11 of federal bankruptcy law, or the ruling is based on a debt canceling. A canceling of debt happens when the lender agrees that the rest of the debt is forgiven.

That being said, here's what you're not allowed to do with a Chapter 7: Lie under oath about your financial or property assets. Keep property that must be used to discharge your debts. Miss payments to certain creditors in order to keep your home.

The biggest difference between Chapter 7 and Chapter 13 is that Chapter 7 focuses on discharging (getting rid of) unsecured debt such as credit cards, personal loans and medical bills while Chapter 13 allows you to catch up on secured debts like your home or your car while also discharging unsecured debt.

Not All Debts Are Discharged Certain debts will remain on your account when you file for Chapter 7 bankruptcy. You will still be responsible for alimony and child support. Tax liens, student loans, and personal injury debts caused by intoxicated drivers are still on the docket, as well.

Of the two options, Chapter 7 is more popular because filers don't have to pay back part of their debts. Chapter 13 may be a better solution if you're in arrears on your mortgage because you can keep your house in Chapter 13 and have time to get caught up on payments.

CHAPTER 7 BANKRUPTCY TIMELINE Day 1: File Bankruptcy Petition with Court & Pay Filing Fees. Day 13 to 33: (7 Days BEFORE Meeting of Creditors) Deadline to Provide Tax Returns to Trustee. Day 20 to 40: Meeting of Creditors - also called 341(a) Meeting. Day 80 to 100: (60 Days AFTER First Date Set. ... DISCHARGE GRANTED.