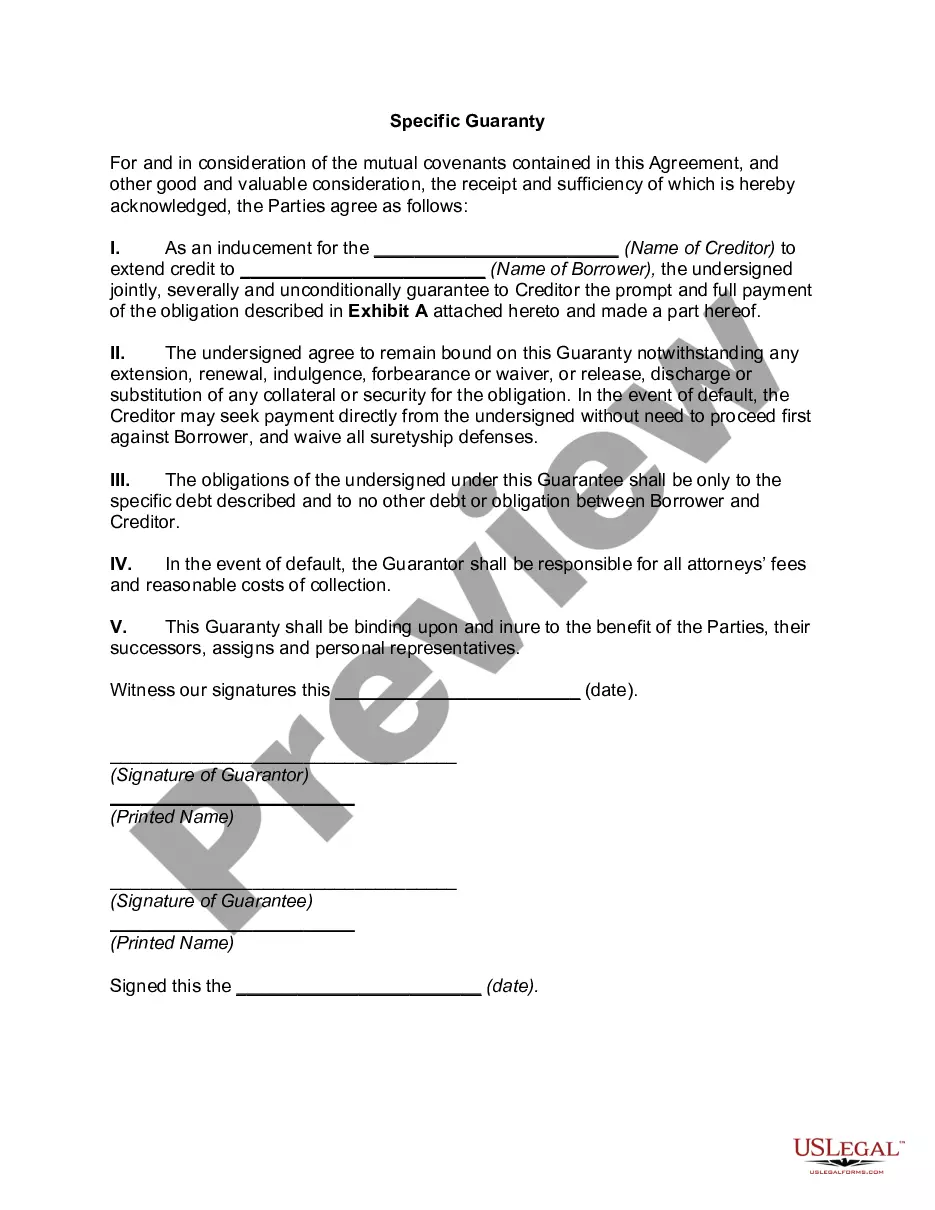

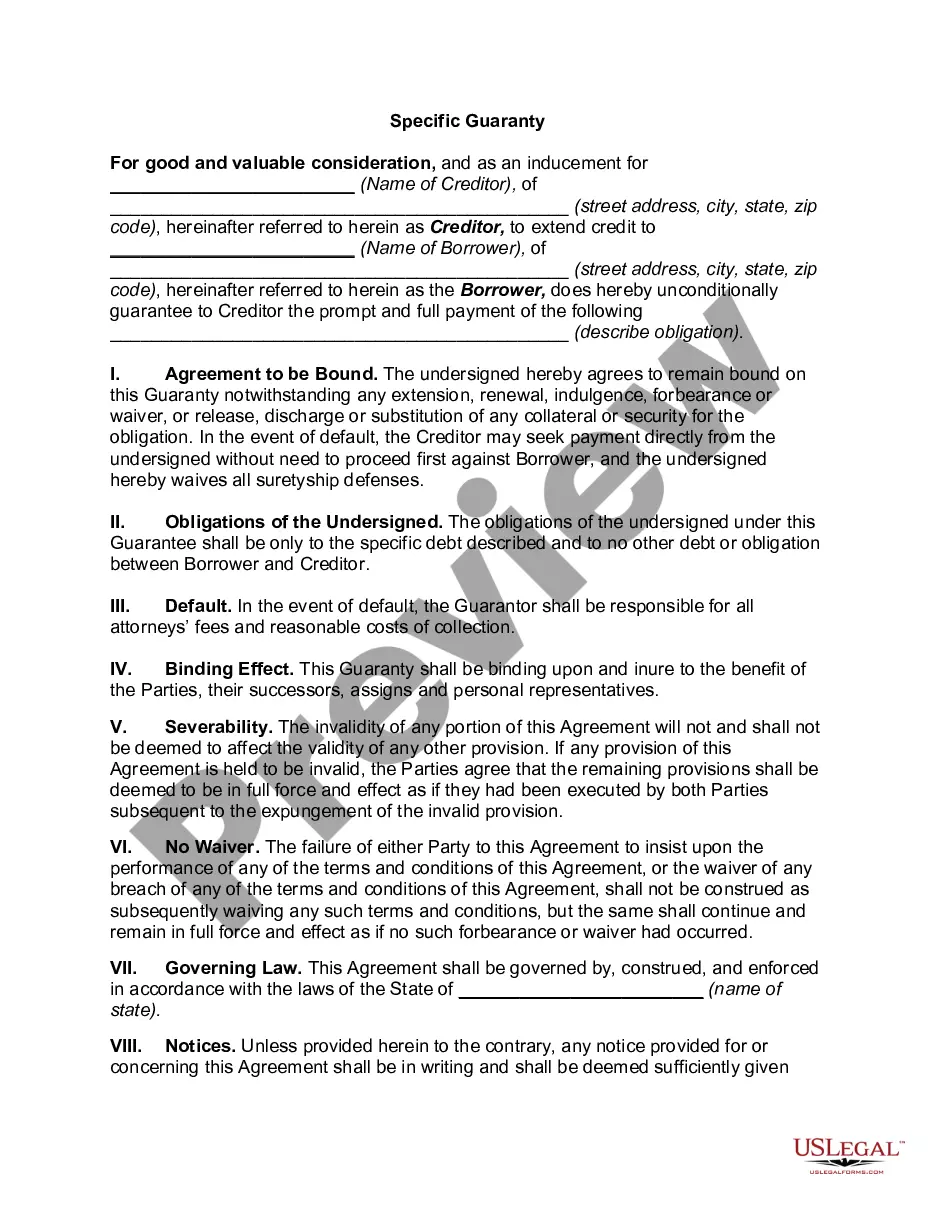

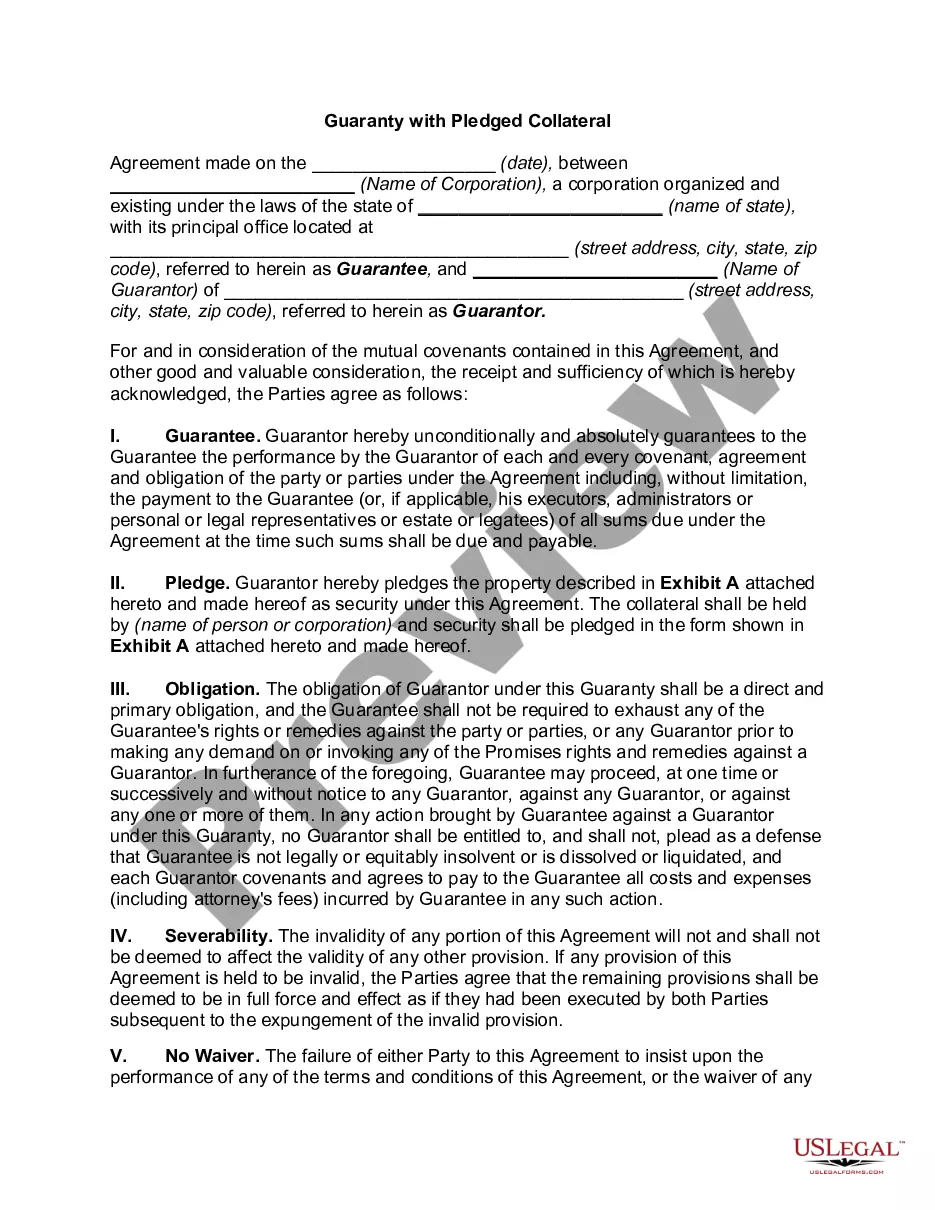

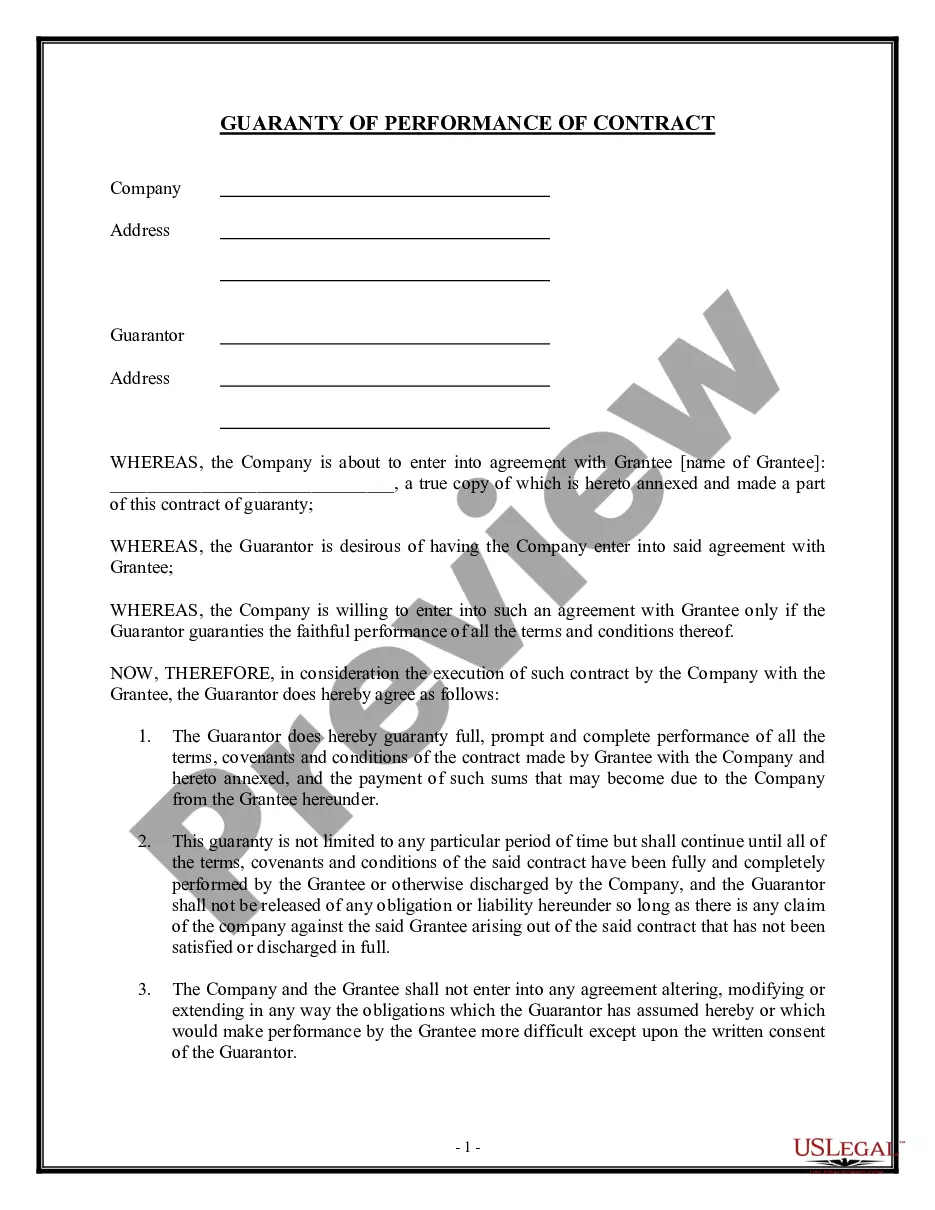

California Guaranty without Pledged Collateral

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Guaranty Without Pledged Collateral?

US Legal Forms - one of the most prominent collections of legal documents in the United States - offers a variety of legal templates that you can either download or print.

By using the website, you can discover thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the latest versions of documents like the California Guaranty without Pledged Collateral within moments.

If you already hold a subscription, Log In to download the California Guaranty without Pledged Collateral from the US Legal Forms library. The Download option will appear on every document you review. You can access all previously downloaded forms in the My documents section of your profile.

Complete the transaction. Use your Visa or Mastercard or PayPal account to finalize the payment.

Select the format and download the document to your device. Make edits. Fill out, modify, print, and sign the downloaded California Guaranty without Pledged Collateral. Every form saved to your account has no expiration date and is yours indefinitely. Therefore, if you wish to download or print another copy, simply visit the My documents section and click on the form you require. Access the California Guaranty without Pledged Collateral with US Legal Forms, the most extensive collection of legal document templates. Utilize thousands of expert and state-specific templates that meet your business or personal needs.

- If you are using US Legal Forms for the first time, follow these simple steps to get started.

- Ensure you have selected the correct form for your city/area. Click on the Review button to examine the form's details.

- Check the form description to confirm you have picked the correct document.

- If the document does not meet your requirements, utilize the Search field at the top of the screen to find one that does.

- Once you are satisfied with the document, confirm your selection by clicking the Buy now button.

- Then, choose your preferred payment plan and provide your information to register for an account.

Form popularity

FAQ

The main difference between a co-signer and a guarantor in California lies in their levels of responsibility. A co-signer shares the obligation equally with the borrower, while a guarantor only becomes liable if the borrower fails to meet the terms. Understanding these distinctions is vital when entering into agreements involving a California Guaranty without Pledged Collateral.

A personal guaranty is not enforceable without consideration In fact, no contract is enforceable without consideration. A personal guaranty is a type of contract.

A guarantee is a contract and such instruments must be in writing by virtue of the Statue of Frauds Act 1677. If the guarantee is drafted as a contract then there is a requirement to evidence consideration (for example in consideration of providing credit to the borrower).

Suretyships and guarantees although both are forms of security for a principal obligation there is a significant difference between these two forms of security. As a general principle guarantees create independent principal obligations while suretyships create accessory obligations.

A surety's undertaking is an original one, by which he becomes primarily liable with the principle debtor, while a guarantor is not a party to the principal obligation and bears only a secondary liability.2 Stated somewhat differently, the distinction between a suretyship and guaranty is that a surety is in the first

The "guarantor" is the person guarantying the debt while the party who originally incurred the debt is the "principle" and the creditor is the "guaranteed party." Under California law, if properly drafted, a guaranty is a fully enforceable obligation which allows the guaranteed party to proceed directly against the

If the guarantee is enforceable based on the points described in this guide, unfortunately, there is no way to get out of a personal guarantee. However, there are some steps you can take to protect yourself from the potentially damaging consequences of the guarantee being called in.

If you sign a personal guarantee, you are personally liable for the loan balance or a portion thereof. If your business later defaults on the loan, anyone who signed the personal guarantee can be held responsible for the remaining balance, even after the lender forecloses on the loan collateral.

As nouns the difference between pledge and guaranty is that pledge is a solemn promise to do something while guaranty is (legal) an undertaking to answer for the payment of some debt, or the performance of some contract or duty, of another, in case of the failure of such other to pay or perform; a warranty; a security.

Understanding Financial Guarantees Guarantees may take on the form of a security deposit. Common in the banking and lending industries, this is a form of collateral provided by the debtor that can be liquidated if the debtor defaults.