Arkansas Performance and Payment Bond

What this document covers

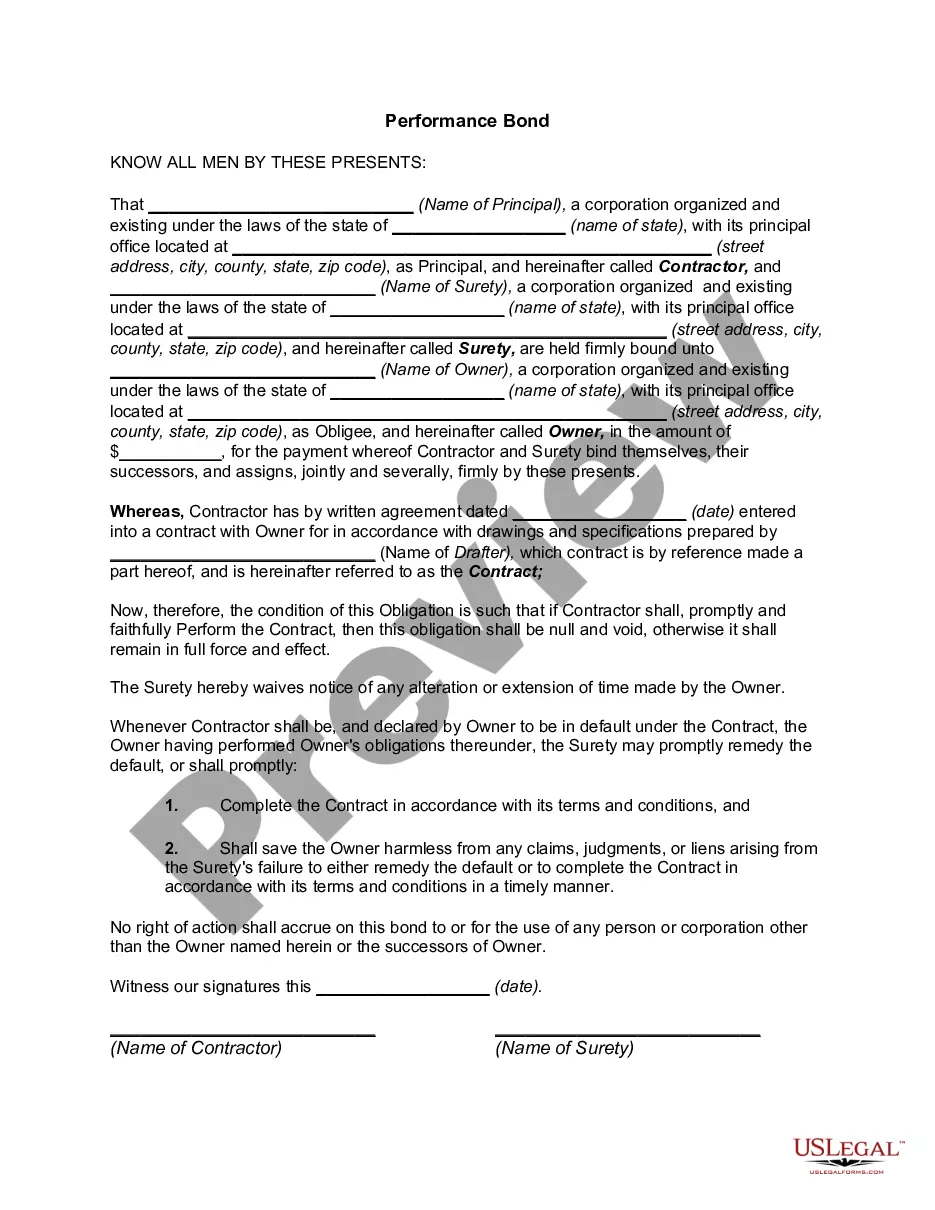

A Performance and Payment Bond is a legal document that provides a guarantee from a surety company or bank to ensure the satisfactory completion of a project by a contractor. This bond serves two primary purposes: it holds the contractor accountable for fulfilling their contractual obligations and ensures that payment is made to all proper claimants for materials and labor supplied for the project. Unlike other contracts, this bond specifically protects the owner and subcontractors by providing financial backing in case of default or non-payment.

Key parts of this document

- Parties involved: Identification of the Principal (contractor), Surety, and Obligee (owner).

- Contract details: References the specific contract related to the bond.

- Performance obligation: The Principal's commitment to complete the project as per the contract.

- Indemnification clause: Outlines the principal and surety's responsibility for any damages arising from the Principal's default.

- Payment obligations: Ensures payment for labor and materials furnished under the contract.

- Legal compliance: Affirms adherence to Arkansas laws governing bonds and contracts.

Common use cases

This form is essential when a contractor is hired for a project, particularly in construction or large service agreements. It should be used when the owner requires assurance that the project will be completed satisfactorily and that all subcontractors and suppliers will receive payment. Additionally, it is necessary in situations where state laws mandate the use of performance and payment bonds for certain types of contracts.

Who this form is for

- Contractors needing to provide assurance of their performance on a project.

- Owners of construction projects requiring financial security against contractor default.

- Subcontractors or suppliers to ensure payment for their contributions to a project.

- Surety companies acting as guarantors for contractors.

Steps to complete this form

- Identify and enter the names of all parties involved: the Principal, Surety, and Obligee (Owner).

- Specify the contract amount and the project details, including the project number.

- Include the date of the contract and the specific obligations under the Performance and Payment Bond Agreement.

- Ensure signatures are obtained from both the Principal and the Surety, along with any necessary affidavits or power of attorney documents.

- Review the form to ensure all legal requirements and state-specific provisions are fulfilled before execution.

Is notarization required?

This form does not typically require notarization unless specified by local law. However, it is advised to verify local regulations to ensure compliance, especially if specific jurisdictions have unique requirements.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to complete specific fields such as contract details and signatures.

- Inaccurately identifying the Surety or Obligee.

- Neglecting to comply with state-specific legal requirements.

- Forgetting to attach necessary documentation like power of attorney if required.

Advantages of online completion

- Immediate access to the form, enabling quick and efficient processing.

- Easy editing capabilities to tailor the document to specific needs.

- Reliable updates to ensure compliance with the latest legal standards.

- Convenient options for electronic signatures and submissions.

Legal use & context

- This bond is enforceable under contract law, providing protection to both the owner and subcontractors.

- It establishes clear obligations for the contractor, assisting in project accountability.

- The bond aids in mitigating risks associated with contractor non-performance and payment disputes.

Main things to remember

- A Performance and Payment Bond provides financial assurance for the completion of a project.

- It protects both the project owner and subcontractors from potential defaults.

- Always ensure compliance with state regulations when completing the bond.

Looking for another form?

Form popularity

FAQ

The difficulty of obtaining a performance bond often depends on the contractor's financial stability and project scope. Contractors with a solid financial background and good credit will generally find it easier to secure a bond. Utilizing US Legal Forms can streamline the process and help you meet the necessary requirements for an Arkansas Performance and Payment Bond.

To get a surety bond in Arkansas, start by researching qualified surety companies that specialize in bonds. Then, gather the necessary documentation and submit an application for evaluation. Platforms like US Legal Forms can assist with the application process, providing templates and guidance tailored to Arkansas Performance and Payment Bond requirements.

Posting a performance bond means that a contractor provides a financial guarantee to complete a project as per the contract terms. It protects the project owner from financial losses if the contractor fails to meet their obligations. For contractors in Arkansas, understanding this aspect is vital when applying for an Arkansas Performance and Payment Bond.

To release a performance bond, you must ensure that all contractual obligations are fulfilled and then notify the surety company. Providing documentation of project completion is essential in this process. The help of US Legal Forms can be invaluable in ensuring you have all the right documents prepared.

A performance bond is issued after a contractor applies through a surety company and is assessed for creditworthiness and project risk. Once approved, the surety will issue the bond, indicating their commitment to compensate the project owner if the contractor fails to perform. Understanding this process is crucial for securing an Arkansas Performance and Payment Bond.

To request the release of a performance bond, you need to submit a formal request to the surety company. This request should include documentation proving that the project has been completed as per contract specifications. Utilizing platforms like US Legal Forms can simplify this process and provide the necessary templates and guidance.

To close out a bond, you typically need to fulfill all the obligations specified in the bond agreement. This process often involves notifying the surety company and providing any necessary documentation to demonstrate that all work is complete. With the right guidance, such as from US Legal Forms, navigating this process can be easier.

To file a claim on an Arkansas Performance and Payment Bond, start by gathering all necessary documentation related to the bond, such as the bond number and any relevant contracts. Next, contact the surety company that issued the bond and notify them of your intent to make a claim. Provide them with the required information and any supporting documents to substantiate your claim. This process helps ensure that your claim is evaluated promptly and fairly.

The calculation of a performance bond typically depends on the total contract value and the risk involved in the project. Generally, bonding companies will assess factors such as the project's complexity and the contractor's financial stability. An experienced broker can help you determine the amount needed for your Arkansas Performance and Payment Bond to ensure it meets the project's requirements.

To write a performance bond, begin by clearly stating the obligations of the contractor and the holder. Include specific details regarding the project, timeline, and the bond amount. Consider consulting platforms like USLegalForms for templates that can guide you in setting up a comprehensive Arkansas Performance and Payment Bond.