Alabama Prior Lienholder's Agreement and subordination

Overview of this form

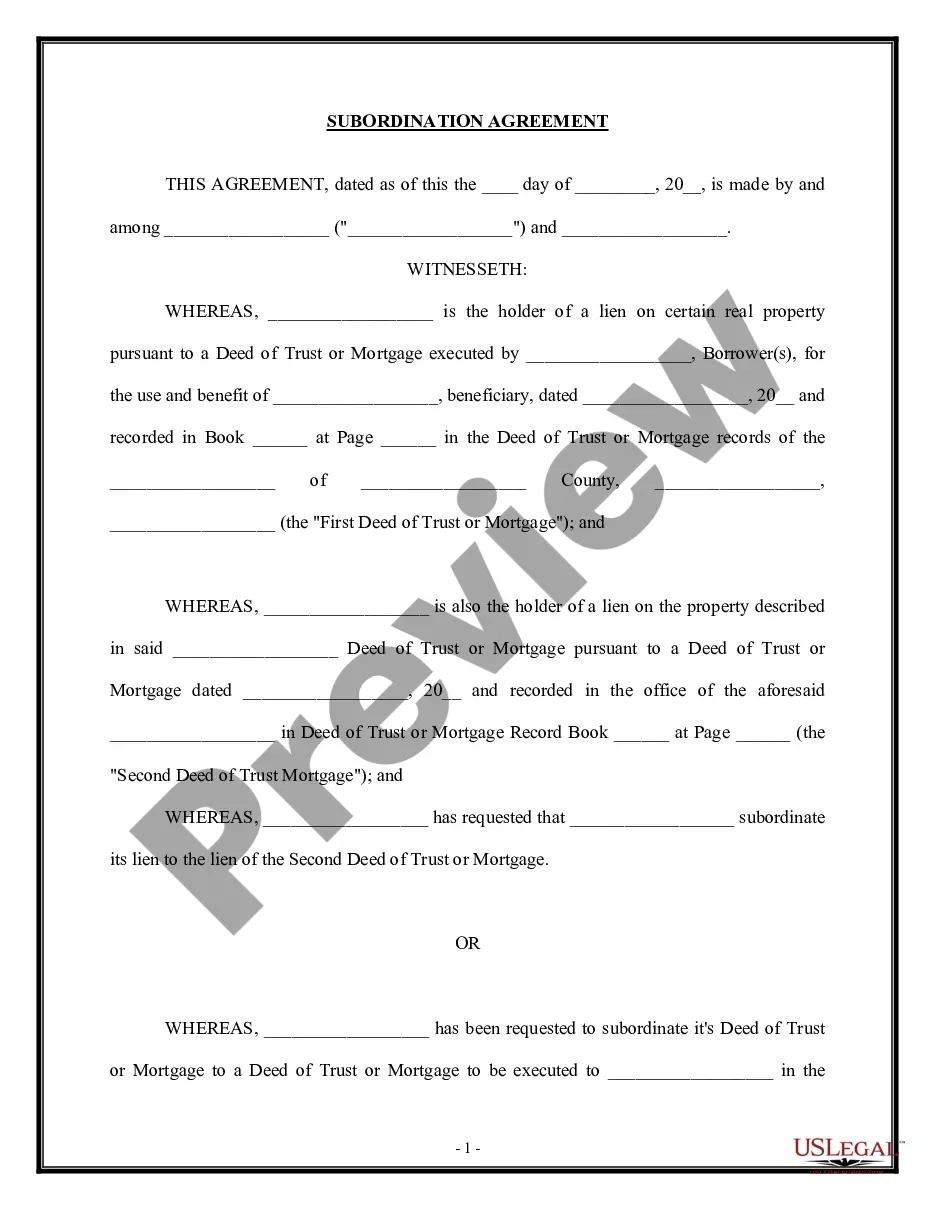

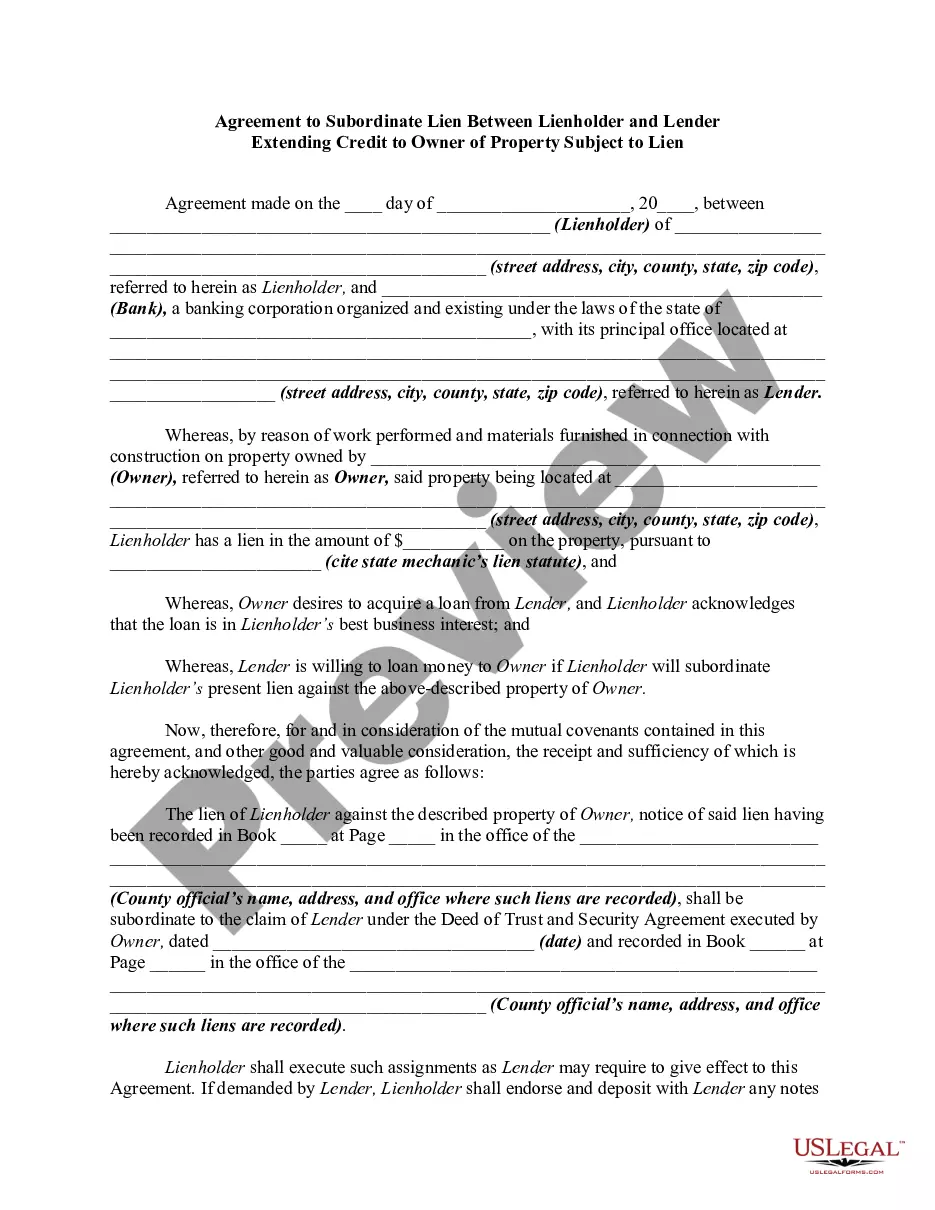

The prior lienholder's agreement and subordination is a legal document that allows an existing lender, or prior lienholder, to agree to subordinate their financial interest in a property to a new lender. This form is essential for facilitating new loans where the prior lender agrees to accept a lower priority on the property lien in exchange for receiving partial payment. It helps to clarify the order of claims against the property, particularly when additional financing is secured.

What’s included in this form

- Parties involved, including the prior lienholder, the new lender, and the borrower.

- Recitals outlining the context, including existing loans and property descriptions.

- Agreement clauses detailing the subordination of the prior lienholder's rights.

- Notice provisions for events of default and enforcement rights.

- Successors and assigns clause ensuring the agreement binds future parties.

When to use this document

This form is typically used when a borrower seeks additional financing while they have an existing loan secured by the property. If the new lender requires a first position lien on the property, the prior lienholder may need to agree to subordinate their lien. This is common in refinancing situations, construction loans, or when consolidating debt.

Who needs this form

- Prior lienholders looking to facilitate a new loan for a current borrower.

- New lenders who require a subordinate lien as part of a loan agreement.

- Borrowers intending to refinance or secure additional financing for their property.

Instructions for completing this form

- Identify the parties involved, including the prior lienholder, new lender, and borrower.

- Clearly specify the amounts of the prior loan and new loan.

- Include property details and attach legal descriptions as needed.

- Complete each clause to reflect the agreements regarding subordination and payment.

- Have all parties sign the form, ensuring acknowledgment before a notary public.

Is notarization required?

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Incomplete information about the property or loan amounts.

- Failing to have the document notarized as required.

- Not including all parties' signatures, which can render the agreement invalid.

- Neglecting to clearly outline the terms of subordination and any obligations of the parties.

Why use this form online

- Convenient access to customizable templates tailored to your needs.

- Editable form content ensures that specific details can be easily updated.

- Reliable, attorney-drafted documents provide legal assurance.

Looking for another form?

Form popularity

FAQ

But as property values are going up and the demand for refinance isn't as much, it seems that the subordination process has gotten a little easier. Typically, it takes two to three weeks to get the resubordination paperwork through, and it is likely to set you back $200 to $300.

But as property values are going up and the demand for refinance isn't as much, it seems that the subordination process has gotten a little easier. Typically, it takes two to three weeks to get the resubordination paperwork through, and it is likely to set you back $200 to $300.

Unless there is a subordination agreement, it is virtually impossible to refinance your first mortgage. The document agreeing to the subordination must be signed by the lender and the borrower and requires notarization.

A subordination fee is a fee directly related to the credit transaction. There is no comparable cash transaction to compare it to and a subordination is not a required document to perfect your lien. It's only required to perfect your lien in the position that you required as a condition of making the loan.

Subordination agreements are prepared by your lender. The process occurs internally if you only have one lender. When your mortgage and home equity line or loan have different lenders, both financial institutions work together to draft the necessary paperwork.

The signed agreement must be acknowledged by a notary and recorded in the official records of the county to be enforceable.

A subordination agreement acknowledges that one party's claim or interest is superior to that of another party in the event that the borrower's assets must be liquidated to repay the debts.

What is a Subordinate Mortgage? Subordinate mortgages are loans that have a lower priority status than any other recorded liens (or debts) against a property. When you get the loan you need to purchase your home, this loan is typically recorded as the first repayment priority on your deed after closing.