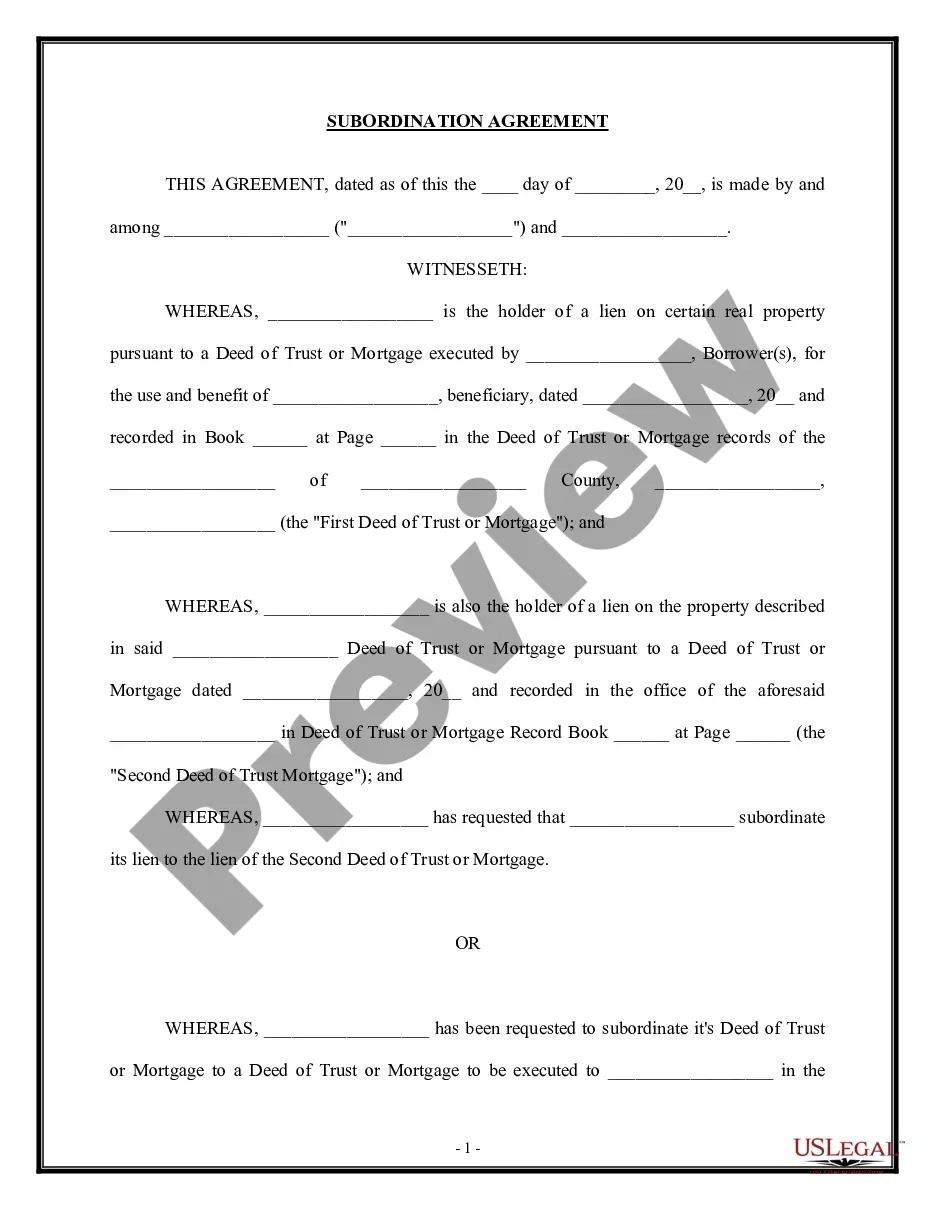

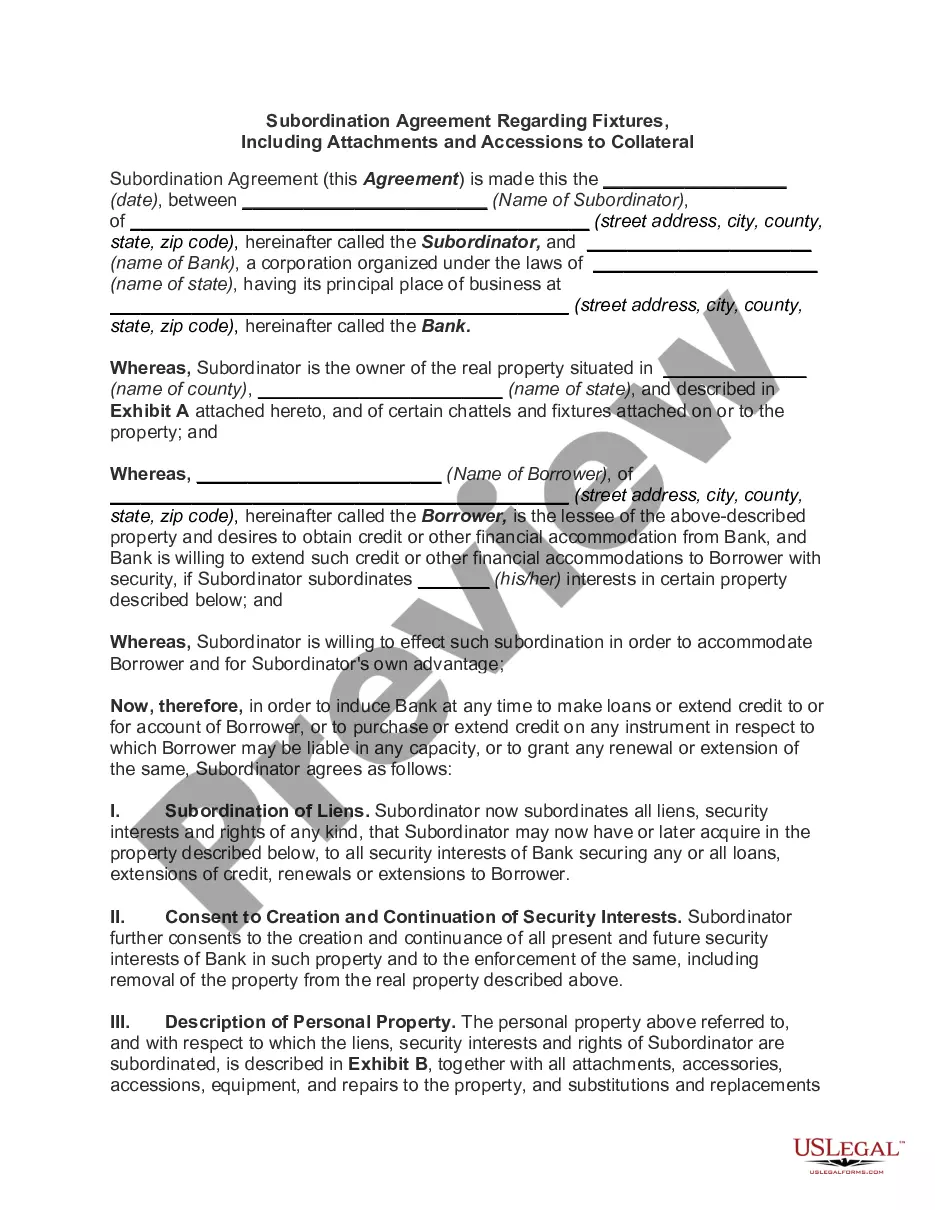

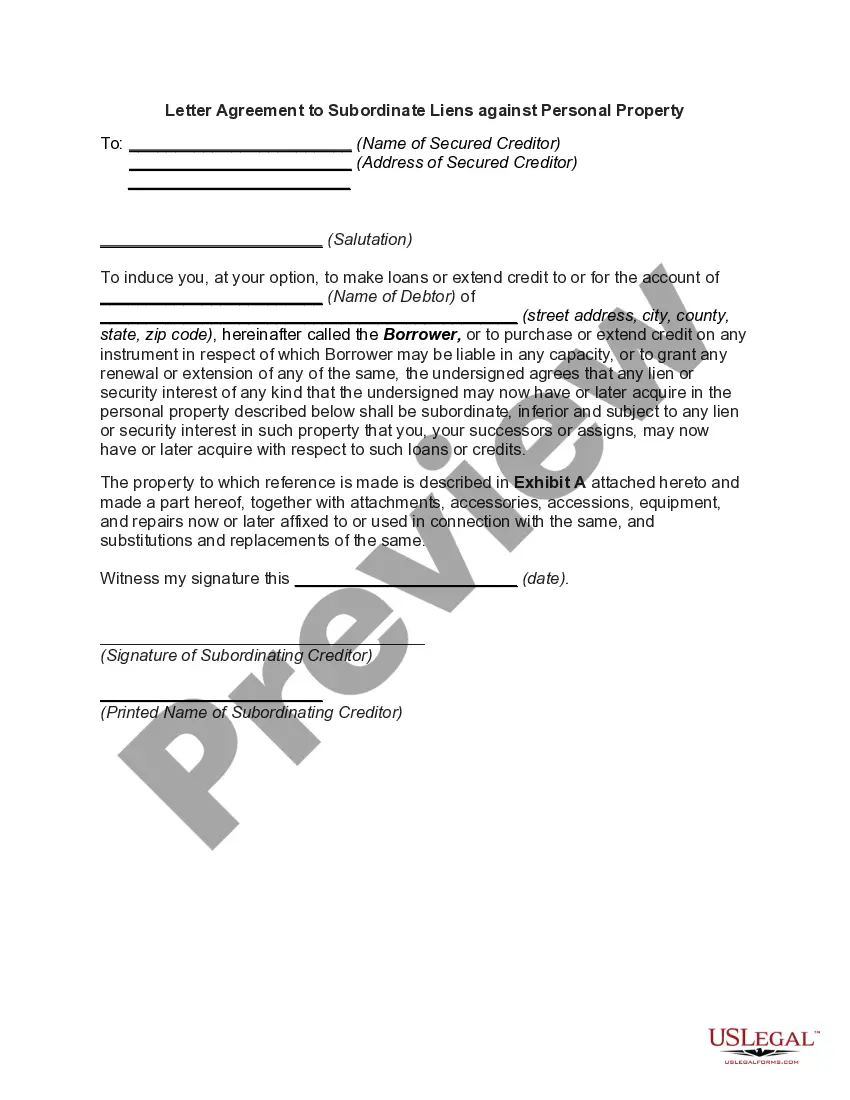

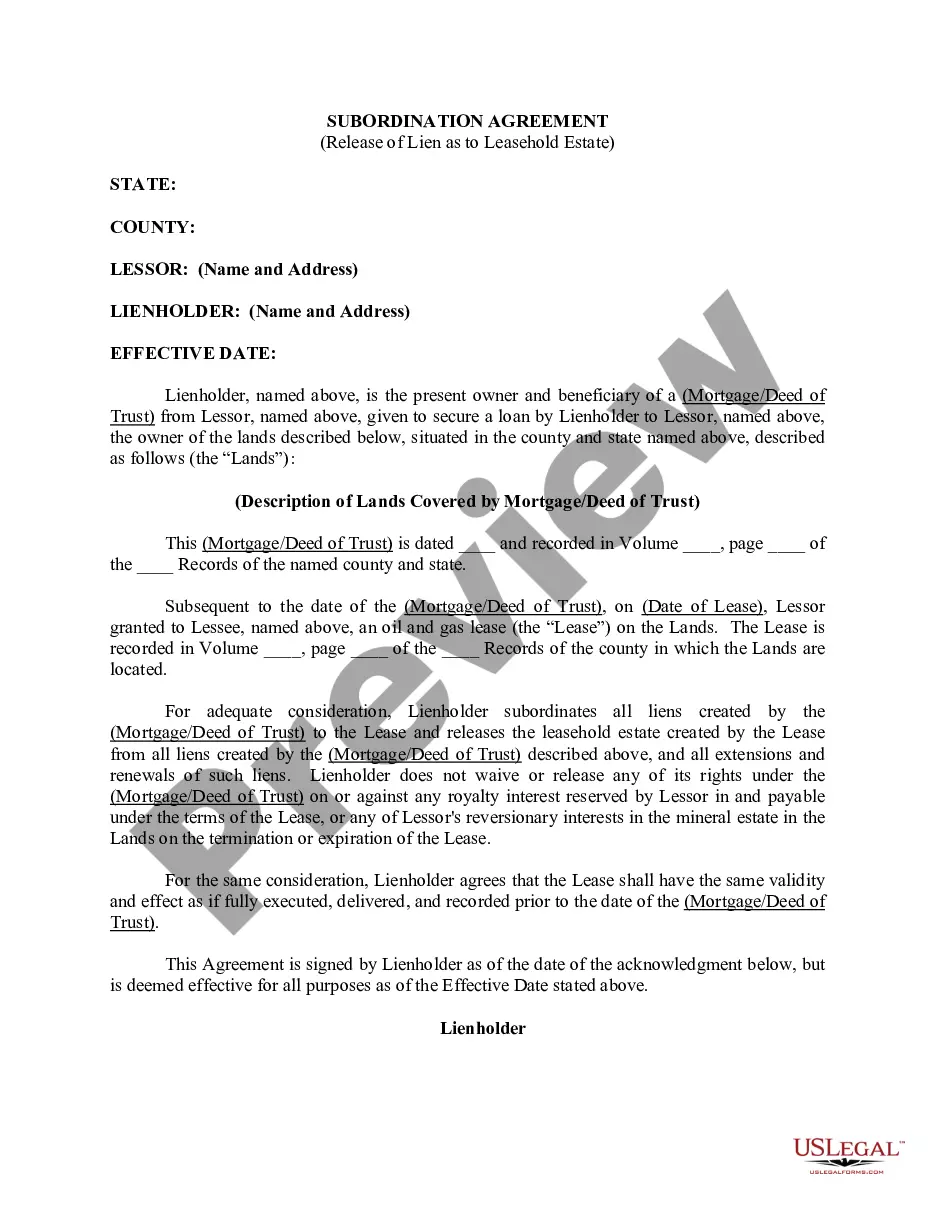

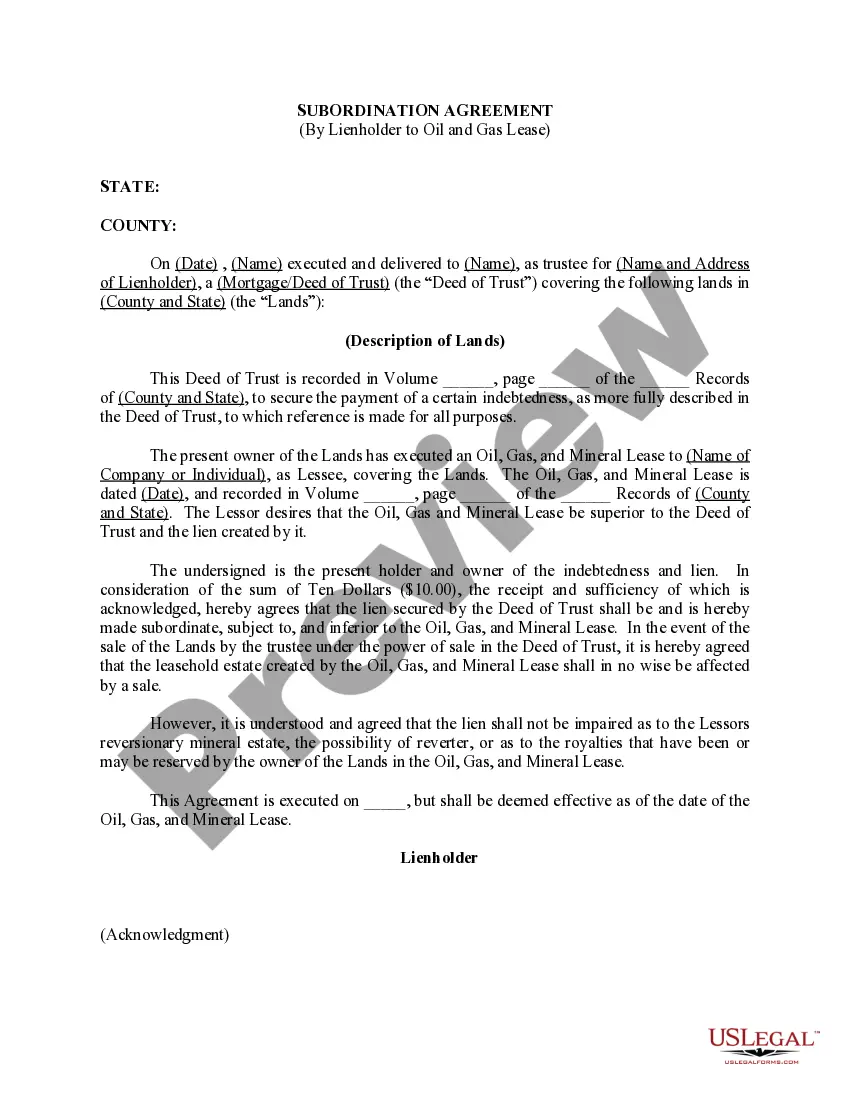

Agreement to Subordinate Lien Between Lienholder and Lender Extending Credit to Owner of Property Subject to Lien

About this form

The Agreement to Subordinate Lien Between Lienholder and Lender Extending Credit to Owner of Property Subject to Lien allows a lienholder to agree to subordinate their lien on a property. This form is essential when a homeowner seeks additional financing and needs a lender to agree to take a higher priority. This agreement differs from standard lien documentation, as it specifically addresses the subordination of existing liens for the benefit of additional credit.

Key components of this form

- Identification of the lienholder and lender, including their addresses.

- Description of the property owned by the owner.

- Details of the existing lien, including the amount and recording information.

- Agreement terms regarding the subordination of the lienholder's lien for loan provisions.

- Execution of assignments by the lienholder, if required by the lender.

- Signatures and acknowledgments from both the lienholder and lender.

When to use this document

This form is necessary when a property owner wants to obtain a new loan but has an existing lien on their property. It is particularly crucial when the lender requires assurance that their loan will have priority over other liens. Situations may include construction financing, refinancing existing loans, or securing additional credit against a property with a prior lien.

Who needs this form

- Property owners seeking to secure a new loan against their property.

- Lenders requiring a subordinate lien for the approved loan.

- Existing lienholders who are willing to subordinate their interests for the benefit of the borrower.

Instructions for completing this form

- Identify and enter the names and addresses of the lienholder and lender at the beginning of the agreement.

- Specify the property details, including the owner's name and the property address.

- State the lien amount and reference the applicable mechanics lien statute.

- Include the details of the new loan agreement and the necessary subordination terms.

- Ensure all parties sign and date the document to finalize the agreement.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to correctly identify all parties involved, including proper names and addresses.

- Not updating lien amounts or missing reference to the original mechanics lien statue.

- Omitting signatures or dates, which can render the agreement invalid.

- Not consulting local regulations that may affect the agreement requirements.

Why complete this form online

- Convenience of downloading and filling out the form at any time.

- Editability allows users to tailor the form to their specific needs.

- Access to templates drafted by licensed attorneys, ensuring legal compliance.

- No need for in-person meetings, saving time and resources.

Looking for another form?

Form popularity

FAQ

A subordination agreement acknowledges that one party's claim or interest is superior to that of another party in the event that the borrower's assets must be liquidated to repay the debts.

Subordination clauses in mortgages refer to the portion of your agreement with the mortgage company that says their lien takes precedence over any other liens you may have on your property.The primary lien on a house is usually a mortgage. However, it's also possible to have other liens.

Subordination agreements are prepared by your lender. The process occurs internally if you only have one lender. When your mortgage and home equity line or loan have different lenders, both financial institutions work together to draft the necessary paperwork.

A subordination agreement often comes up when a home has a first and a second mortgage, and the borrower wants to refinance the first mortgage. If you have two mortgages on your home and refinance the first loan, the refinancing lender might require a subordination agreement.

And many lenders charge a fee to review the subordination package, a fee that might run as high as $100. Your lender will probably pass this fee to you.

Subordination is the tenant's agreement that its interest under the lease will be subordinate to that of the lender.Attornment is the tenant's agreement to become the tenant of someone other than the original landlord and who has now taken title to the property.

Resubordination is the process of keeping the first mortgage in first place, ahead of other mortgages. When you refinance your first mortgage, the lender will insist on resubordinating the home equity loan or line of credit. The equity lender isn't required to resubordinate.

A subordination agreement is a legal document that establishes one debt as ranking behind another in priority for collecting repayment from a debtor. The priority of debts can become extremely important when a debtor defaults on payments or declares bankruptcy.

But as property values are going up and the demand for refinance isn't as much, it seems that the subordination process has gotten a little easier. Typically, it takes two to three weeks to get the resubordination paperwork through, and it is likely to set you back $200 to $300.