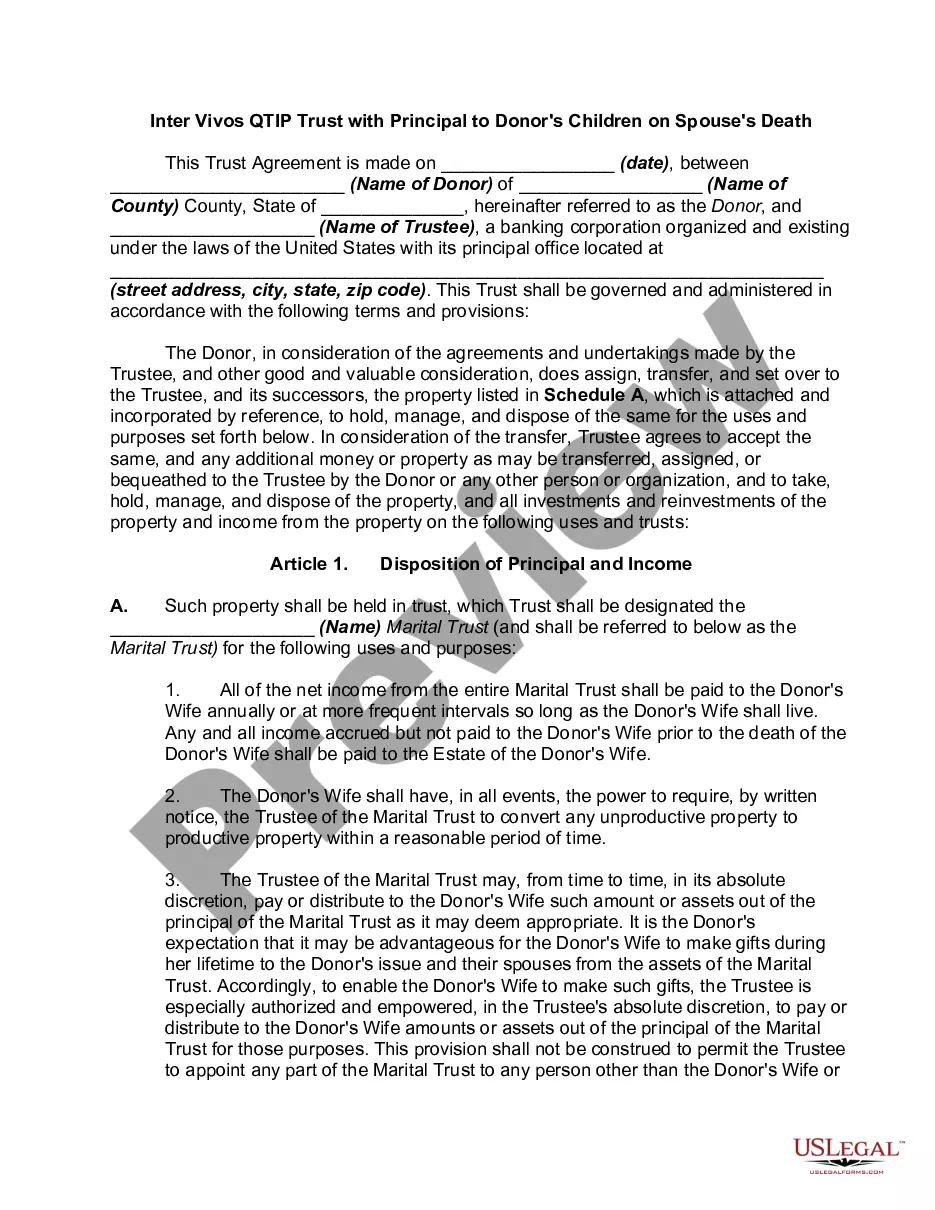

Alaska Gift of Stock to Spouse for Life with Remainder to Children

Description

How to fill out Gift Of Stock To Spouse For Life With Remainder To Children?

If you wish to accumulate, acquire, or print sanctioned document templates, utilize US Legal Forms, the most extensive collection of legal forms available online.

Take advantage of the website's straightforward and user-friendly search to locate the documents you require.

Numerous templates for corporate and personal purposes are categorized by types and regions, or keywords.

Every legal document template you acquire belongs to you permanently.

You will have access to all forms you downloaded in your account. Select the My documents section and choose a form to print or download again.

- Use US Legal Forms to find the Alaska Gift of Stock to Spouse for Life with Remainder to Children in just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Download button to acquire the Alaska Gift of Stock to Spouse for Life with Remainder to Children.

- You can also access forms you previously downloaded from the My documents tab in your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have selected the form for your correct city/state.

- Step 2. Utilize the Review option to examine the content of the form. Always remember to read the description.

- Step 3. If you are not satisfied with the form, use the Search field at the top of the screen to find other versions of your legal form template.

- Step 4. Once you have located the form you need, click the Get now button. Choose the pricing plan you prefer and enter your information to register for an account.

- Step 5. Complete the transaction. You can use your Visa or Mastercard or PayPal account to finalize the purchase.

- Step 6. Select the format of your legal form and download it to your device.

- Step 7. Fill out, edit, and print or sign the Alaska Gift of Stock to Spouse for Life with Remainder to Children.

Form popularity

FAQ

Gift splitting allows a married couple to combine their individual gift tax exemptions to help enhance the benefits of tax-free gifting. This process is not automatic and the ability to split gifts requires that certain prerequisites are met, including the consent of both spouses on a filed federal gift tax return.

Planning Tip: The assets of a properly drafted ILIT can be indirectly available during the client's lifetime if needed. With proper ILIT design, the client's spouse can be the ILIT's sole trustee.

You can give an inheritance in the form of money, real estate, personal items, or a combination of your assets. Keep in mind, if you sell an asset for less than its value, reduce interest, or charge no interest, this may also be considered a gift.

The three-year rule prevents individuals from gifting assets to their descendants or other parties once death is imminent in an attempt to avoid estate taxes.

Give now or later: The IRS doesn't care The U.S. tax code makes it fairly easy to give your children money, stocks or other investments or a piece of the family business. You can transfer up to a certain amount during your lifetime as a gift or at death through a will, free from federal gift and estate taxes.

Tax-free gifts.You can give up to $16,000 per calendar year (in 2022) per recipient without paying gift tax. You can also pay someone's tuition or medical bills, or give to a charity, without paying gift tax on the amount.

Note that certain classes of Crummey powerholders will require additional planning, including: Spouses. Spouses, as trust beneficiaries, can hold Crummey powers.

A Trust (or Marital Trust)The surviving spouse must be the only beneficiary of the trust during his/her lifetime, however, at the time of the second spouse's death, the trust can pass to any other named beneficiaries like children, grandchildren, etc.

According to federal tax law, if an individual makes a gift of property within 3 years of the date of their death, the value of that gift is included in the value of their gross estate. The gross estate is the dollar value of their estate at the time of their death.

Generally, the Gross Estate does not include property owned solely by the decedent's spouse or other individuals. Lifetime gifts that are complete (no powers or other control over the gifts are retained) are not included in the Gross Estate (but taxable gifts are used in the computation of the estate tax).