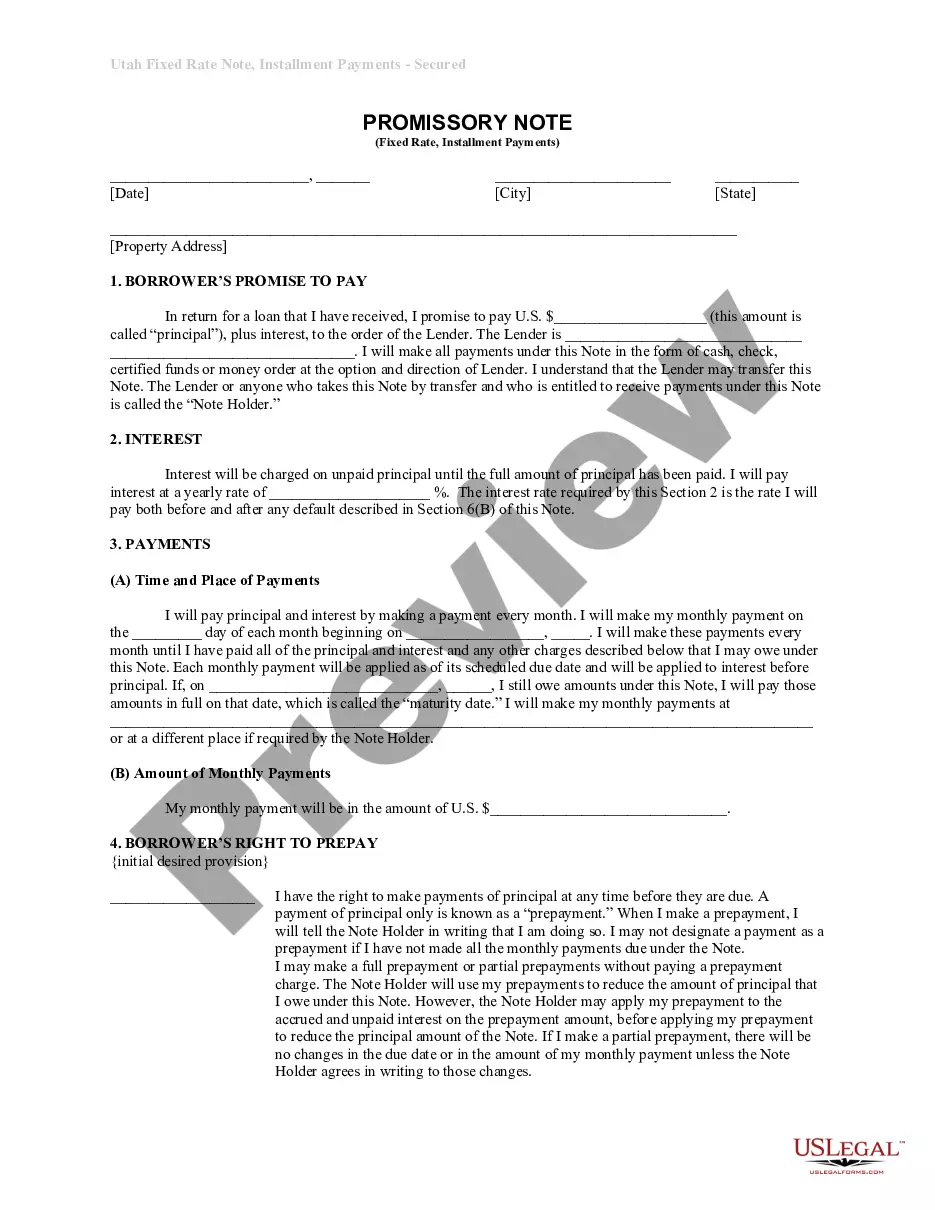

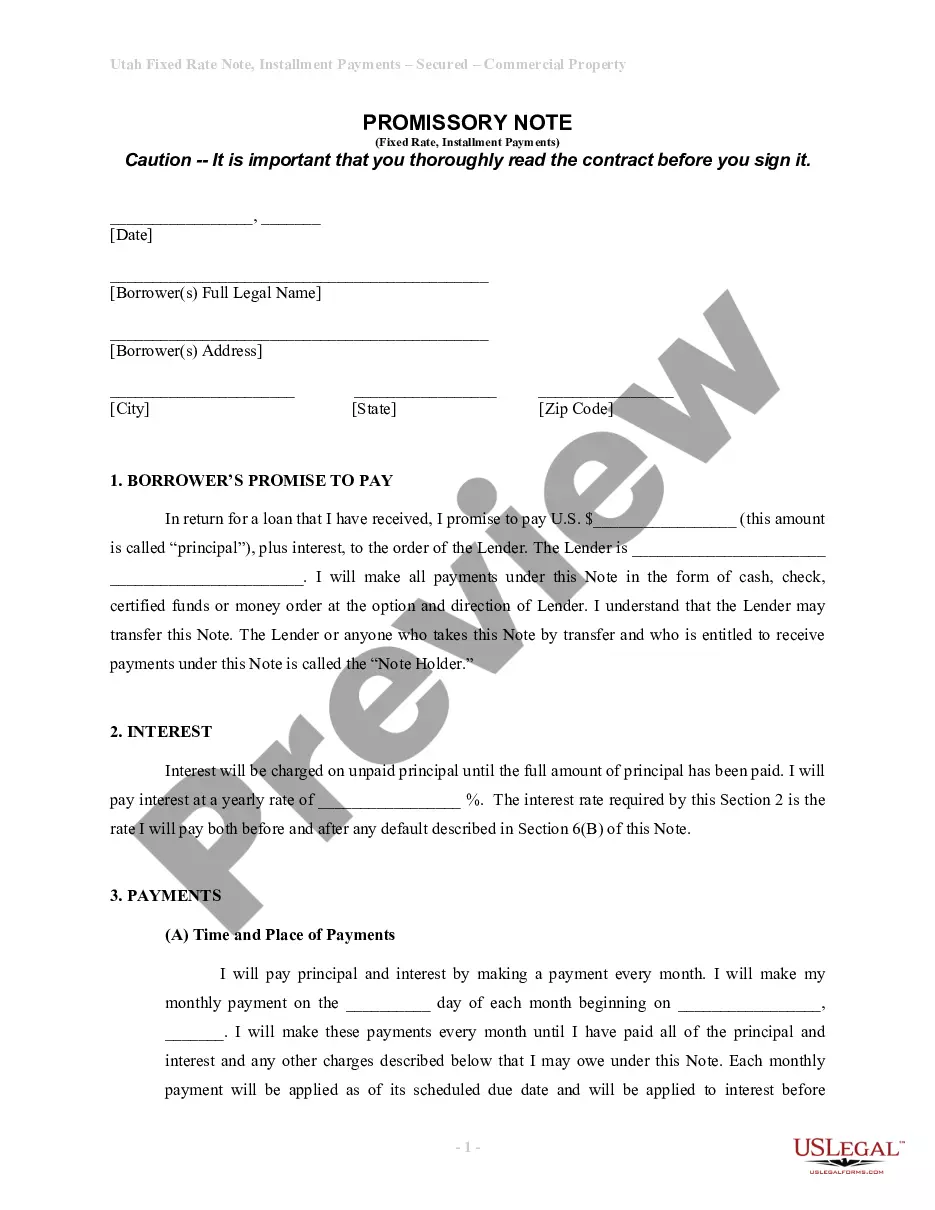

Utah Installments Fixed Rate Promissory Note Secured by Personal Property

What this document covers

The Utah Installments Fixed Rate Promissory Note Secured by Personal Property is a formal agreement between a borrower and a lender. This document outlines the borrower's promise to repay a specified loan amount, along with interest, through regular installment payments. The loan is secured by the personal property of the borrower, ensuring the lender has a claim on the property should the borrower default. This type of promissory note differs from unsecured loans by providing added security for the lender through collateral.

Form components explained

- Borrower's promise to pay: Details the principal amount, interest rate, and the lender's identity.

- Interest: Specifies the yearly interest rate applicable to the unpaid principal.

- Payments: Describes the payment schedule, including amounts due and maturity date.

- Prepayment rights: Outlines conditions under which the borrower can make early payments without penalties.

- Default provisions: States the consequences of failing to make timely payments.

- Security agreement: Details the lien on personal property that secures the note.

When this form is needed

This form is essential when borrowing money and offering personal property as collateral. It can be used in various situations, such as financing a vehicle, purchasing equipment for a business, or consolidating debts. The promissory note provides a structured repayment plan and legal protection for both parties involved.

Who this form is for

This form is suitable for:

- Individuals seeking to secure a loan with personal property.

- Businesses needing financing for operations or purchases with collateral.

- Lenders requiring assurance of repayment through secured property.

- Borrowers who want clear terms on loan repayment to avoid misunderstandings.

Completing this form step by step

To complete the Utah Installments Fixed Rate Promissory Note Secured by Personal Property, follow these steps:

- Identify the parties: Enter the names and addresses of the borrower and lender.

- Specify the loan amount: Fill in the principal sum that is being borrowed.

- Enter the interest rate: Provide the yearly interest rate on the unpaid principal.

- Outline payment details: Set the monthly payment amount and due date for the installments.

- Describe the secured property: Clarify which personal property is being used as collateral.

- Sign and date the document: Ensure both parties sign and date the form for validity.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to specify the interest rate or payment terms clearly.

- Not recognizing the implications of default outlined in the agreement.

- Omitting details about the secured property, leading to potential disputes.

- Not signing the document, which can render it unenforceable.

Why complete this form online

- Convenience of quickly downloading and filling out the form online.

- Editability allows for tailoring the form to specific loan agreements.

- Reliability, with materials drafted by licensed attorneys to ensure compliance.

- The promissory note serves as a legally binding obligation for the borrower to repay the loan.

- In case of non-payment, the lender can enforce their rights against the secured property.

- It is crucial for both parties to fully understand the terms to avoid legal disputes.

Quick recap

- The form is a binding agreement for a secured loan in Utah.

- Key components include payment terms, interest rates, and security provisions.

- It is important to avoid common mistakes for enforceability.

- Using this form online offers convenience and reliability.

Looking for another form?

Form popularity

FAQ

Writing the Promissory Note Terms You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

To write a promissory note for a personal loan, you will need to include the names of both parties, the principal balance, the APR, and any fees that are part of the agreement. The promissory note should also clearly explain what will happen if the borrower pays late or does not pay the loan back at all.

Navigate to the website: www.studentloans.gov. Click "Log In." Enter your FSA ID and Password. Click "Complete Master Promissory Note." Select the appropriate loan type. Enter Your Personal Information.

In order for a promissory note to be valid, both the lender and the borrower must sign the documentation. If you are a co-signer for the loan, you are required to sign the promissory note. Being a co-signer requires you to repay the loan amount in the instance that the borrower defaults on payment.

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

Date. The promissory note should include the date it was created at the top of the page. Amount. Loan terms. Interest rate. Collateral. Lender and borrower information. Signatures.

The lender holds the promissory note while the loan is being repaid, then the note is marked as paid and returned to the borrower when the loan is satisfied. Promissory notes aren't the same as mortgages, but the two often go hand in hand when someone is buying a home.