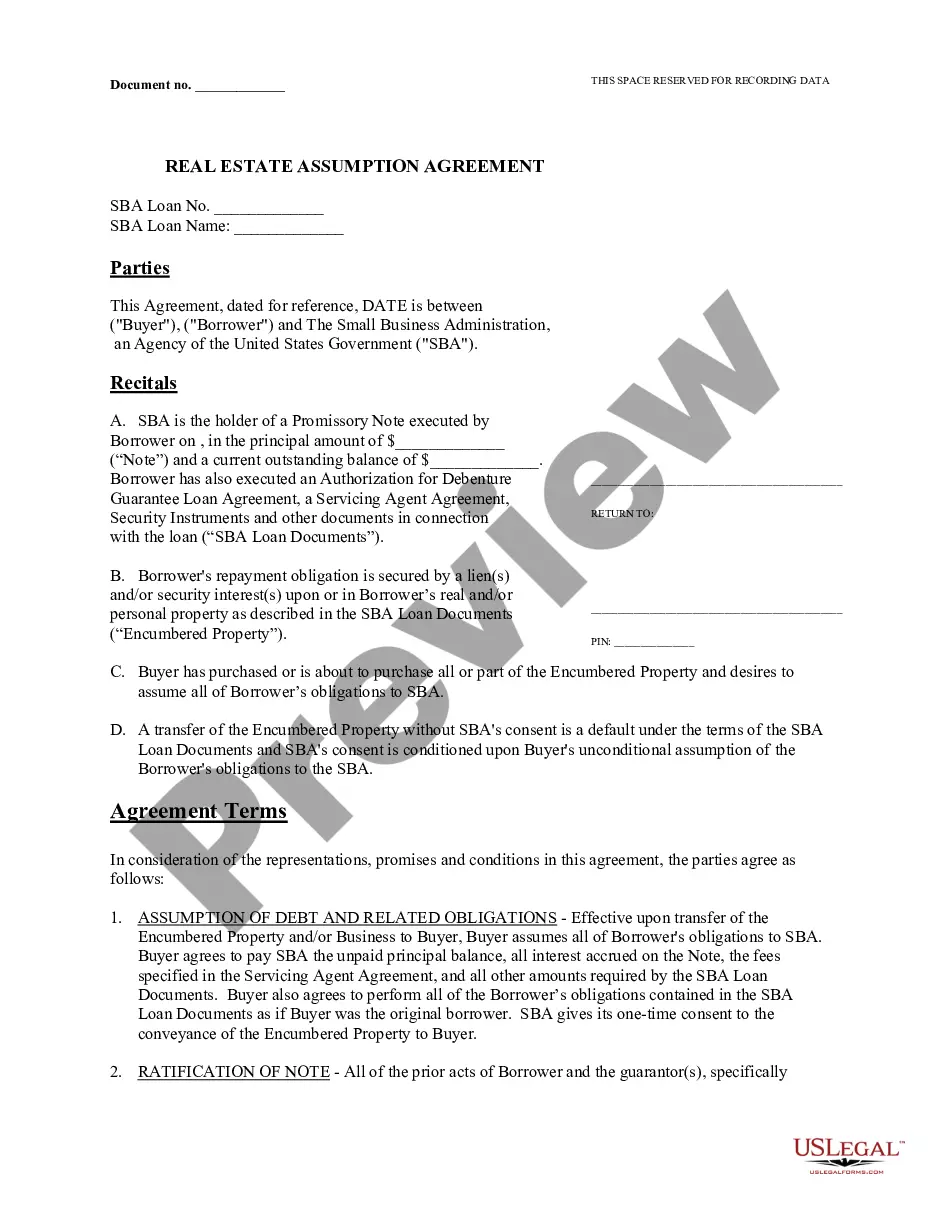

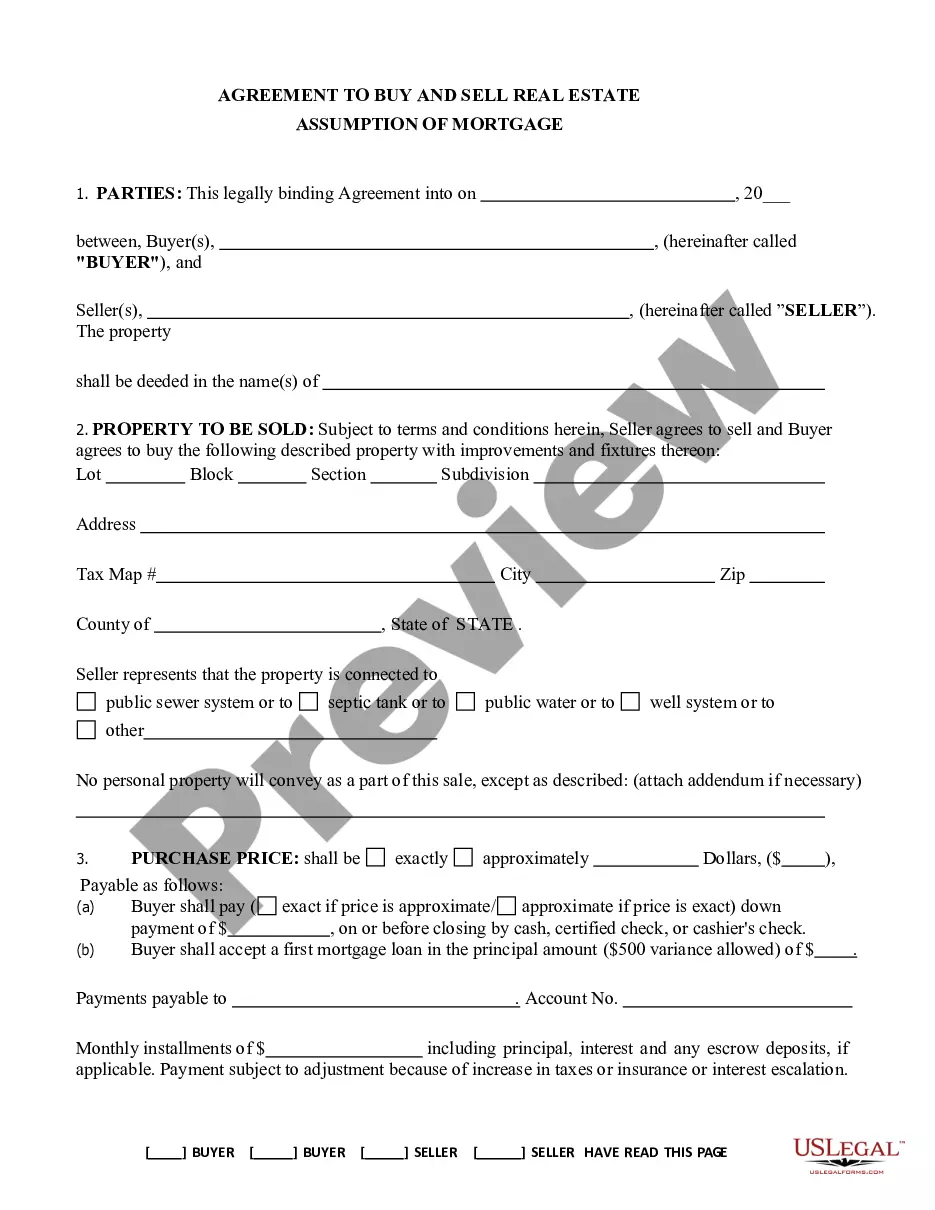

Indiana Assumption Agreement of Mortgage and Release of Original Mortgagors

About this form

This Assumption Agreement of Mortgage and Release of Original Mortgagors is a legal document that allows new purchasers of a property to assume the existing mortgage obligations from the original mortgagors. This form differs from other mortgage documents by specifically facilitating the transfer of liability from the previous owners to the new buyers, thereby releasing the original mortgagors from any future responsibility for the loan.

Main sections of this form

- Identification of the Purchaser(s) who will assume the mortgage.

- Details about the indebtedness, including the loan amount and interest rate.

- Specification of the monthly payment terms and other financial obligations.

- A clause affirming the release of the original mortgagors from future liability.

- Signature lines for all parties involved, including notary acknowledgment.

Common use cases

This form is used when a property is sold, and the buyer wishes to take over the existing mortgage of the seller. It is particularly useful in situations where the original owners want to be released from their mortgage obligations while allowing the new purchasers to continue paying off the mortgage debt. This arrangement benefits both parties and provides a clear legal framework for the transition.

Who needs this form

This form is appropriate for:

- New purchasers of property who are assuming a mortgage.

- Original mortgagors seeking to be released from their mortgage obligations.

- Lenders or mortgagees who need to formalize the transfer of liability.

Instructions for completing this form

- Identify the new Purchaser(s) who will assume the mortgage.

- Enter the total amount of indebtedness and the interest rate.

- Specify the date when monthly payments will begin.

- Complete the financial details for monthly payments, including principal, interest, and taxes.

- Have all parties sign the document and ensure notarization if required.

Does this form need to be notarized?

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to complete all financial details accurately.

- Not having the document notarized if required by local law.

- Neglecting to inform all relevant parties about the mortgage assumption.

Advantages of online completion

- Convenient downloads allow for immediate access to essential legal documents.

- Edit and customize forms easily to fit your specific needs.

- Reliable templates drafted by licensed attorneys ensure legal compliance.

Looking for another form?

Form popularity

FAQ

Unless you're assuming a loan from a relative, you generally must qualify for mortgage assumption once the home seller confirms they have an assumable loan. Generally speaking, the buyer must meet the same credit and income requirements applicable to a brand-new loan.

An assumable mortgage is an arrangement in where an outstanding mortgage and its terms can be transferred from the current owner to a buyer.

Advantages. If the assumable interest rate is lower than current market rates, the buyer saves money straight away. There are also fewer closing costs associated with assuming a mortgage. This can save money for the seller as well as the buyer.

Having an assumable loan might give a seller a marketing edge, particularly if mortgage rates have risen since the seller got the loan. For a buyer, assuming a mortgage can save thousands of dollars in interest payments and closing costs but it could require making a big down payment.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

What is a mortgage assumption agreement? It's actually pretty self-explanatory. A person who assumes a mortgage takes over a payment from the previous homeowner. Basically, the agreement shifts the financial responsibility of the loan to a different borrower.

An assumption clause is a provision in a mortgage contract that allows the seller of a home to pass responsibility for the existing mortgage to the buyer of the property. In other words, the new homeowner assumes the existing mortgage.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.