Arizona Non-Foreign Affidavit Under IRC 1445

What this document covers

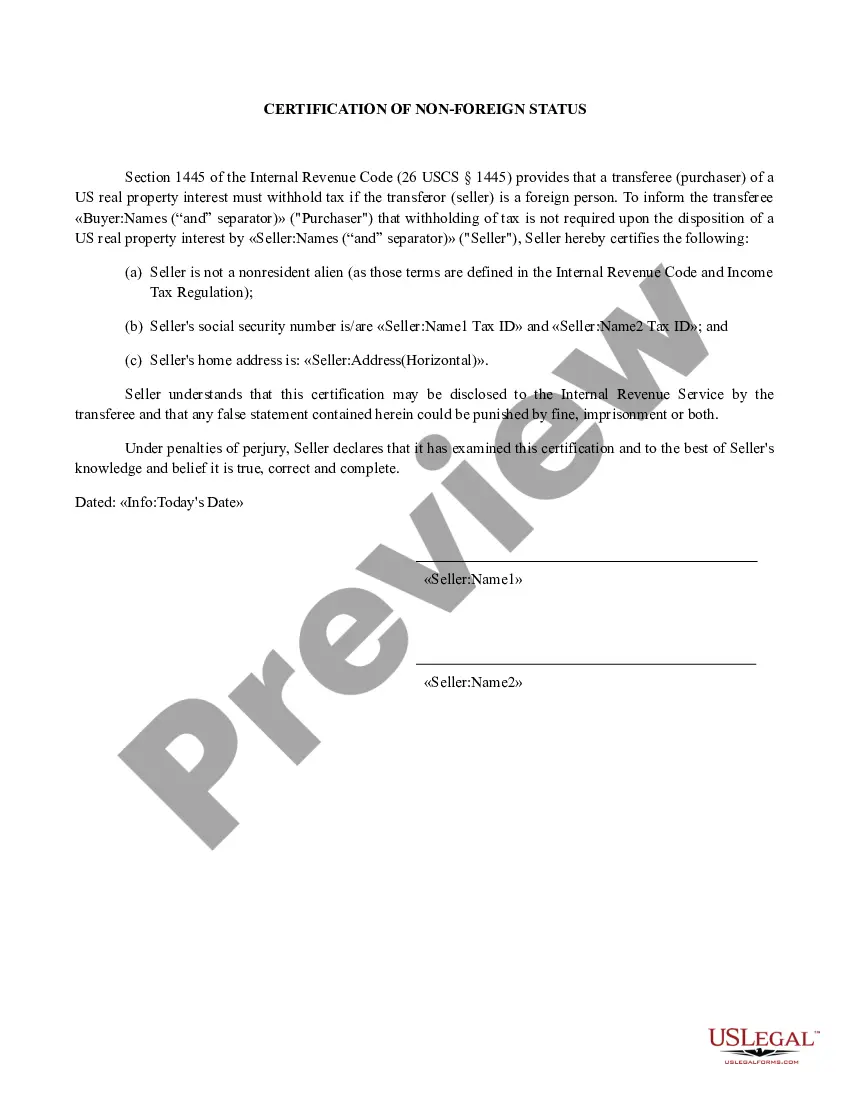

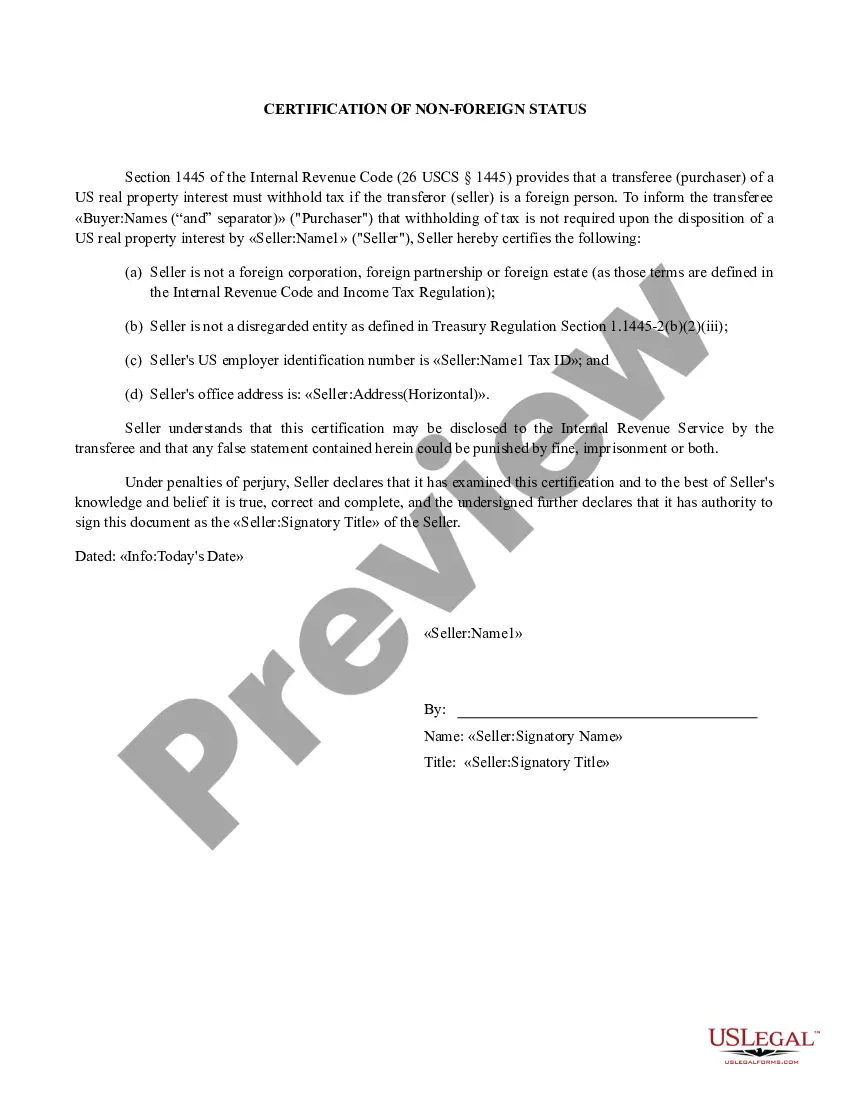

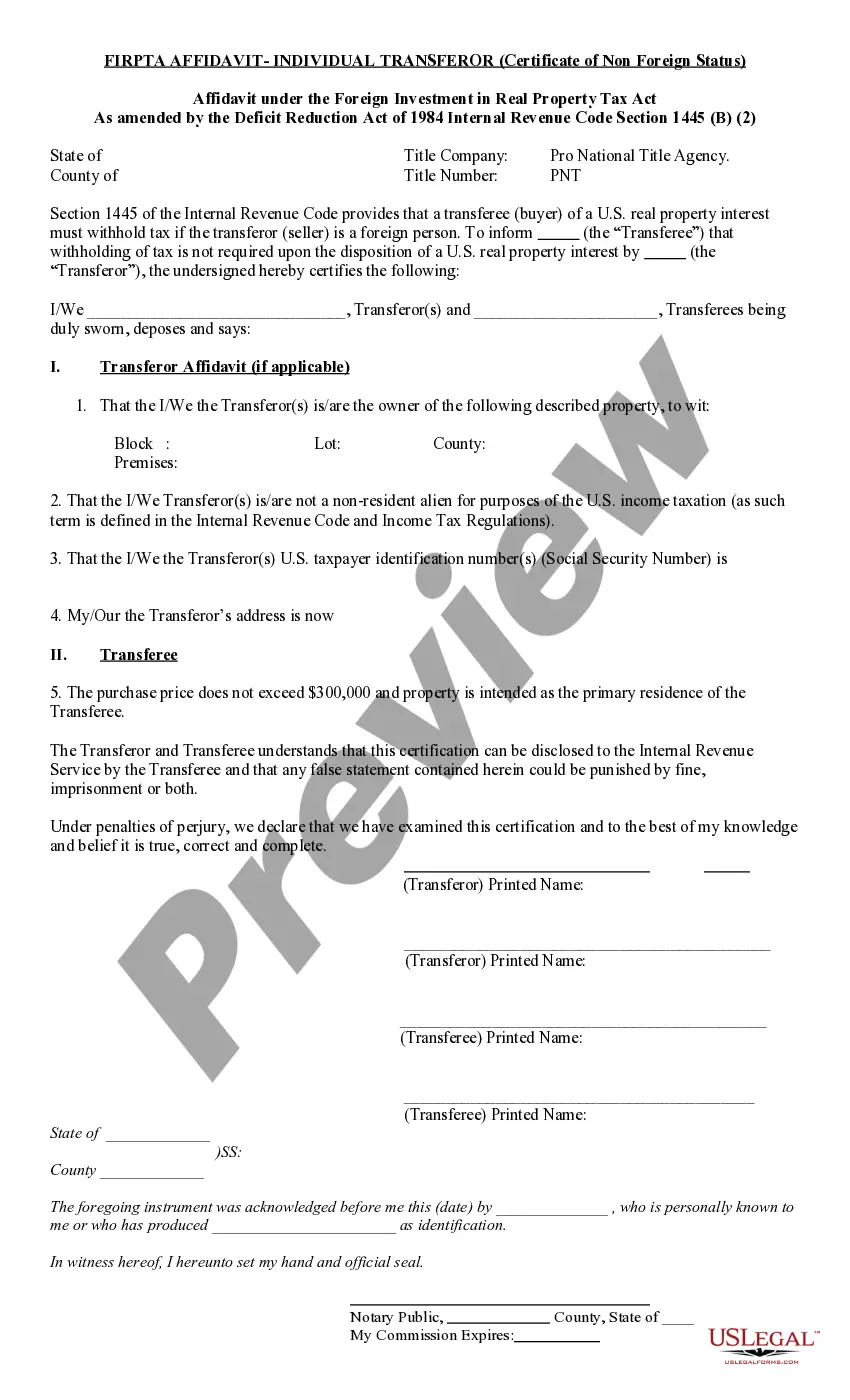

The Non-Foreign Affidavit Under IRC 1445 is a legal document that serves as a declaration from the seller of real property, affirming that they are not a foreign person as defined under Internal Revenue Code Section 26 USC 1445. This affidavit is essential for sellers to prevent withholding taxes on the sale of their property, as it verifies their status as a U.S. taxpayer. Unlike other property documents, this form specifically addresses the foreign person classification, thereby helping to facilitate smoother real estate transactions.

Key parts of this document

- Identifying information of the seller(s), including names, taxpayer identification numbers, and addresses.

- Details of the property being transferred, such as location, legal description, and parcel number.

- Affirmation of non-foreign status as outlined in Internal Revenue Code Section 1445.

- Signature lines for the seller(s), which must be accompanied by notarization.

When to use this form

This form is used when a U.S. resident sells real property and needs to certify their status to avoid withholding taxes on the proceeds of the sale. When the seller is not a foreign person, securing this affidavit establishes exemption from the withholding requirements under IRC 1445, which is particularly important when dealing with buyers or real estate transactions that involve large sums of money.

Who this form is for

This affidavit should be used by:

- Individuals selling residential or commercial real estate in the U.S.

- Parties involved in real estate transactions who are U.S. citizens or resident aliens.

- Sellers who want to ensure compliance with IRS regulations regarding foreign persons and withholding taxes.

How to prepare this document

- Enter the names of the seller(s) in the designated area.

- Provide the property address, including the city, county, and state.

- Fill in your taxpayer identification number and complete your address.

- Affirm that you are not a foreign person by checking the relevant section.

- Sign and date the affidavit in the presence of a notary public.

Is notarization required?

Yes, this form must be notarized to be legally valid. The notarization process involves the seller(s) signing the affidavit in the presence of a notary public, which helps in authenticating the document. US Legal Forms offers integrated online notarization services, making it convenient to complete your affidavit securely via video call without needing to travel.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to provide correct taxpayer identification numbers.

- Not fully completing property details, leading to incomplete descriptions.

- Neglecting to sign in front of a notary, which can invalidate the affidavit.

Why complete this form online

- Convenient access to pre-drafted and attorney-reviewed templates.

- Editable forms that can be tailored to individual transaction needs.

- Streamlined process that saves time compared to manual drafting.

- Secure storage of forms for future reference and compliance checks.

Key takeaways

- The Non-Foreign Affidavit Under IRC 1445 is essential for sellers to affirm their non-foreign status.

- This form helps prevent unnecessary withholding taxes during real estate transactions.

- Accurate completion and notarization are crucial for the affidavitâs legal validity.

Looking for another form?

Form popularity

FAQ

Section 1221 of the Internal Revenue Code defines what constitutes capital assets for tax purposes. This section outlines which assets are subject to capital gains tax or ordinary income tax, impacting how profits from sales are reported. Understanding this section aids taxpayers in making informed financial decisions. For foreign sellers of real estate, the Arizona Non-Foreign Affidavit Under IRC 1445 can help navigate the complexities surrounding these assets.

The amount a transferor realizes on the transfer of U.S. real property interest can be zero in certain circumstances, such as a gift or a significant reduction in property value. In these scenarios, the seller may not receive immediate compensation for their interest. It is crucial to understand how these transactions impact tax implications. For clarity and compliance, the Arizona Non-Foreign Affidavit Under IRC 1445 plays an important role.

A seller is classified as a foreign person based on their citizenship status and residency. If they are not a U.S. citizen or do not meet specific residency requirements, they fall into this category. Recognizing a seller's classification is essential for tax withholding purposes. Utilizing the Arizona Non-Foreign Affidavit Under IRC 1445 can help clarify a seller's status and facilitate the transaction.

The Internal Revenue Code (IRC) is a comprehensive set of tax laws in the United States, established and enforced by the Internal Revenue Service (IRS). It includes various sections that cover different tax principles, including income tax, property tax, and employment tax. Section 1445 specifically addresses the withholding tax for foreign sellers of U.S. real estate. Utilizing the Arizona Non-Foreign Affidavit Under IRC 1445 can simplify compliance with these regulations.

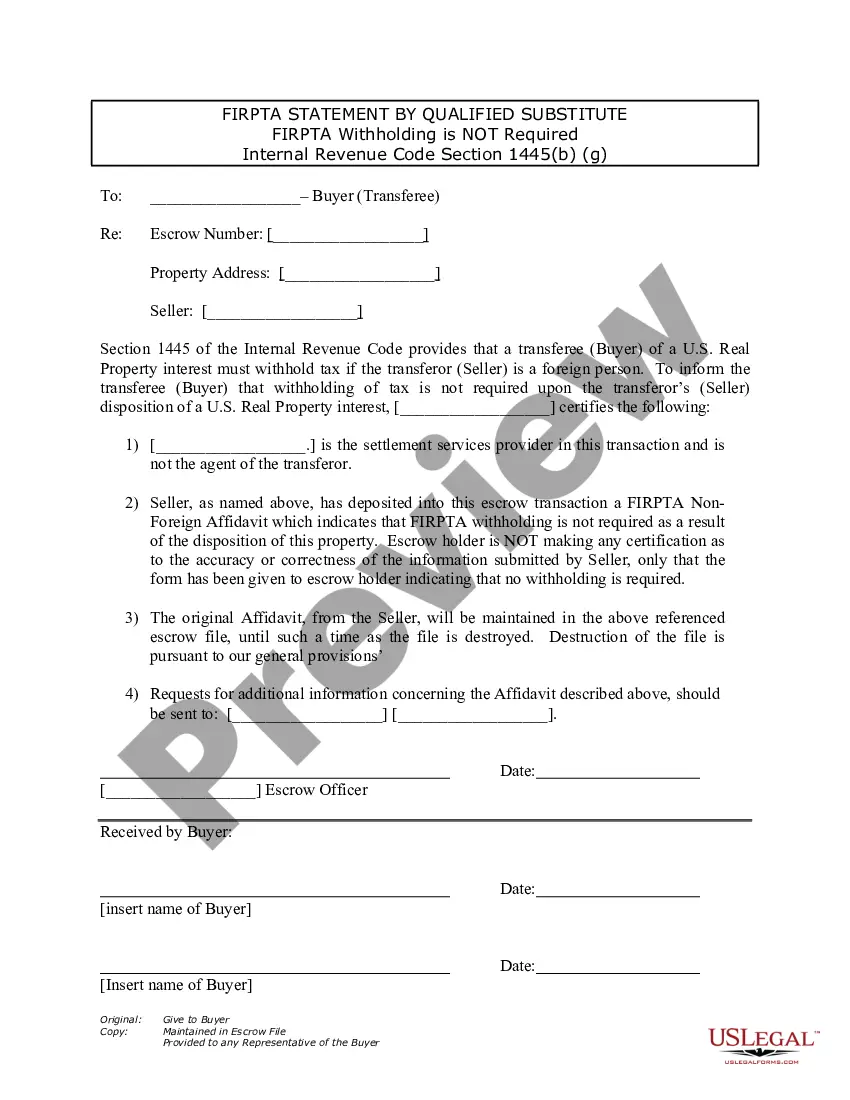

FIRPTA withholding is required to be submitted to the IRS within 20 days of the closing together with IRS Form 8288, U.S. Withholding Tax Return for Disposition by Foreign Persons of U.S. Real Property Interests, and Form 8288-A, Statement of Withholding on Dispositions by Foreign Persons of U.S. Real Property

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to income tax withholding (IRC section 1445). The transferee is the withholding agent.If the transferor is a foreign person and you fail to withhold, you may be held liable for the tax.

The address of the property being transferred (or sold) The seller or transferor's information: Full name. Telephone number. Address. Social Security Number, Federal Employer Identification Number, or California Corporation Number.

This document, included in the seller's opening package, requests that the seller swears under penalty of perjury that they are not a non-resident alien for purposes of United States income taxation. A Seller unable to complete this affidavit may be subject to withholding up to 15%.

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA) income tax withholding. FIRPTA authorized the United States to tax foreign persons on dispositions of U.S. real property interests.

You or a member of your family must have definite plans to reside at the property for at least 50% of the number of days the property is used by any person during each of the first two 12-month periods following the date of transfer.