Fcra Law For Student Loans

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

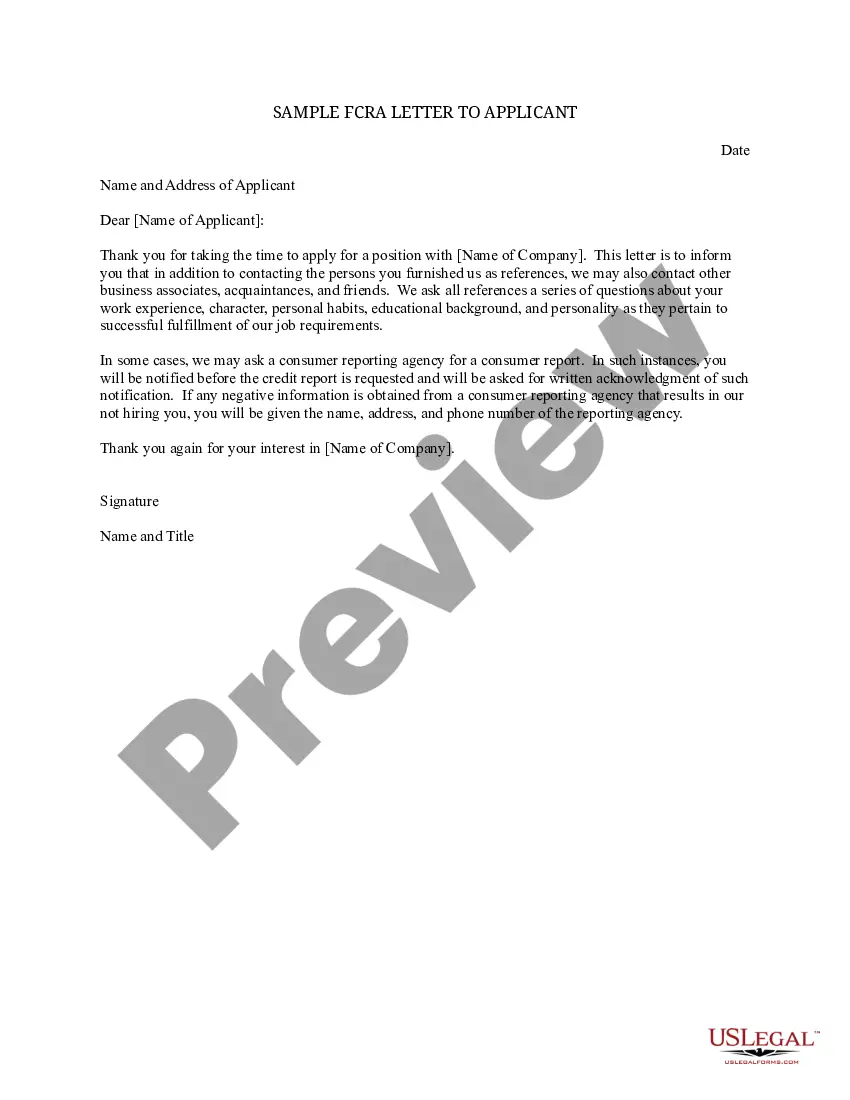

How to fill out FCRA Certification Letter To Consumer Reporting Agency?

- If you're a returning user, log in to your account, ensuring your subscription is active. Click the Download button to get the required form.

- For new users, start by reviewing the form preview and description carefully to choose the appropriate document that fits your needs.

- If you don't find a suitable form, utilize the Search tab to discover other options that comply with your local jurisdiction.

- Select your desired document and click on the Buy Now button, followed by choosing a subscription plan that works for you. Create an account to unlock the essential resources.

- Finish your purchase by entering your credit card information or opting for PayPal.

- After payment, download the form to your device for completion. You can access it anytime via the My Forms section in your profile.

With US Legal Forms, you gain access to an extensive library of more than 85,000 fillable and editable legal templates. This robust collection ensures you find exactly what you need at a competitive cost.

Empower your legal document process today by harnessing the benefits of US Legal Forms. Start your journey towards effective document management now!

Form popularity

FAQ

To have student loans removed from your credit report, start by checking for any inaccuracies in your report. Then, utilize the dispute process under the FCRA law for student loans to request corrections. If you need assistance, USLegalForms offers resources to help you draft the necessary documents for disputes. Taking these steps can help ensure your credit report reflects only accurate information.

In some cases, you can remove student loans from your credit report, especially if they were reported inaccurately. It’s essential to understand the FCRA law for student loans, which mandates that only accurate information remains on your report. If you find inaccuracies, you can dispute those with the reporting agency, potentially leading to their removal. Approaching this process thoughtfully can make a significant difference.

Yes, the Fair Credit Reporting Act (FCRA) applies to student loans. Under this law, lenders must report accurate information about your student loans to credit reporting agencies. When you understand the FCRA law for student loans, you can better protect your credit report from errors related to your student loans. This protection enables you to maintain a healthy credit score.

FCRA permission to pull credit means that lenders and credit agencies must obtain your consent before accessing your credit report. This permission ensures that you are aware of who is reviewing your financial information, which is particularly important when managing student loans. Having clarity on the FCRA law for student loans enables you to control your financial data while exploring various lending options.

The new law regarding medical bills on credit reports simplifies the way these debts affect your credit score. It offers protection for consumers by preventing medical debt from immediately impacting your credit profile. By understanding how the FCRA law for student loans interacts with medical collections, you can make informed decisions that protect your financial health.

The new FCRA law introduces updates to how consumer credit information is reported and handled, aiming for more accuracy and fairness. This law impacts student loans by ensuring clearer communication and requiring lenders to offer more favorable terms after certain conditions are met. By familiarizing yourself with the FCRA law for student loans, you can better protect your rights and enhance your credit profile.

The 7 year rule for student loans refers to the time frame in which negative information, like defaults, can remain on your credit report. After seven years, these negative marks typically fall off, which can significantly improve your credit score. Understanding the FCRA law for student loans helps you navigate this timeline effectively, allowing you to prepare for better financial opportunities as your credit report clears.

Under the FCRA law for student loans, you have the right to access your credit report and dispute inaccuracies. This law ensures that credit reporting agencies maintain accurate information about you. Additionally, you can seek damages if a creditor improperly denies you credit based on erroneous data. Understanding your rights can empower you to take control of your financial future.

Student loans typically do not get written off automatically based on age alone. However, under certain circumstances, like disability or death, loans may be forgiven. Understanding the FCRA law for student loans is crucial, as it can protect your credit report and provide additional insights into managing your loans. It's essential to explore all options and consult with a professional to navigate your specific situation effectively.