Difference Between Fcra And Facta

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

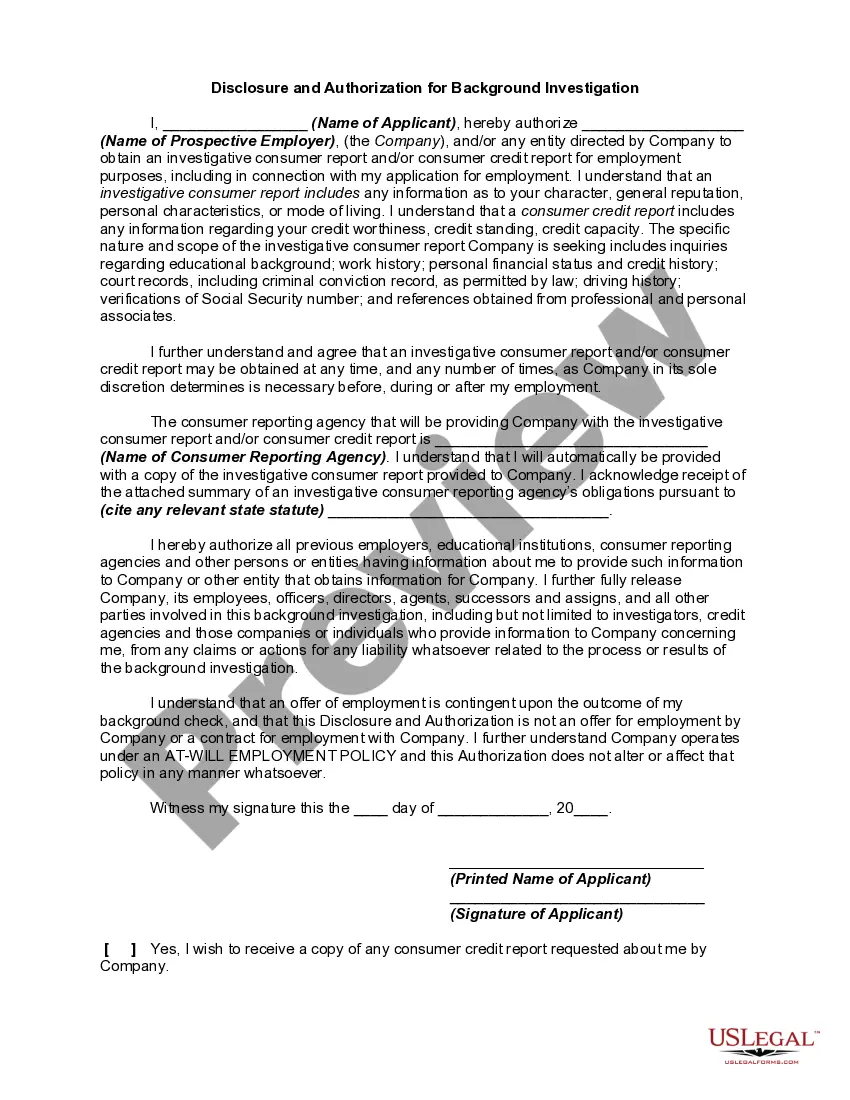

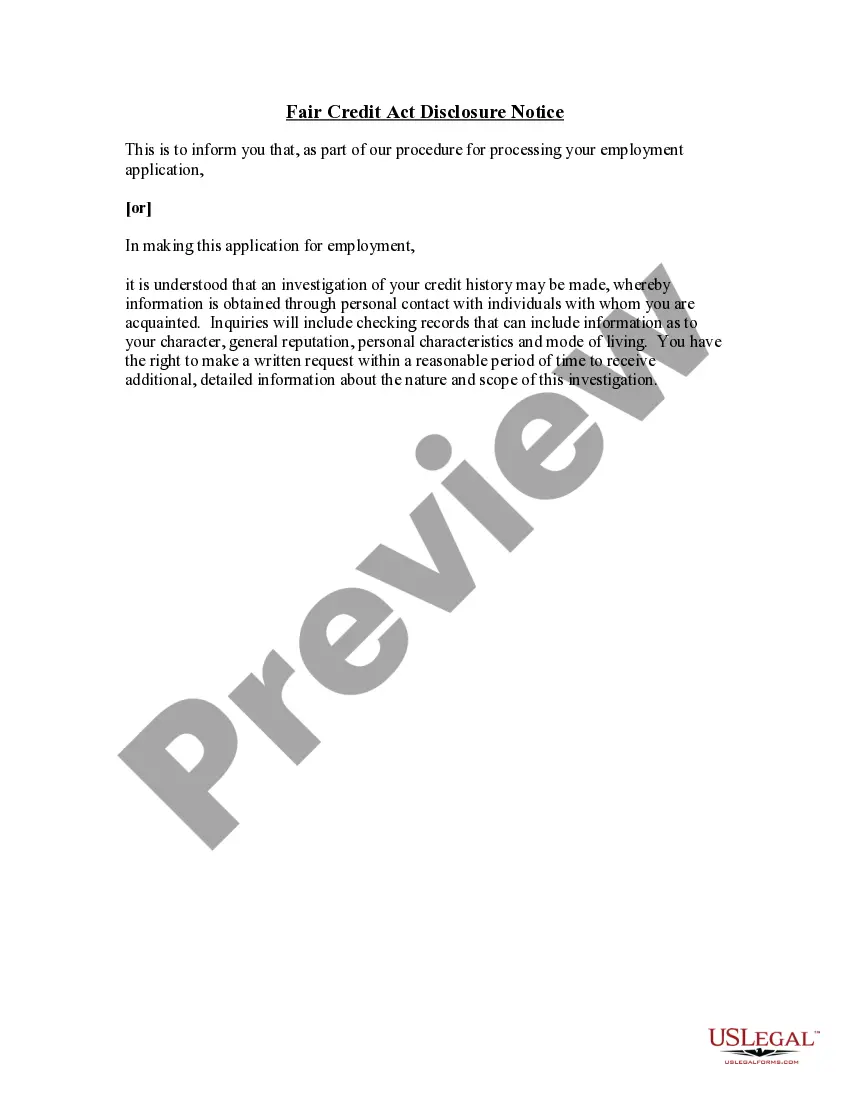

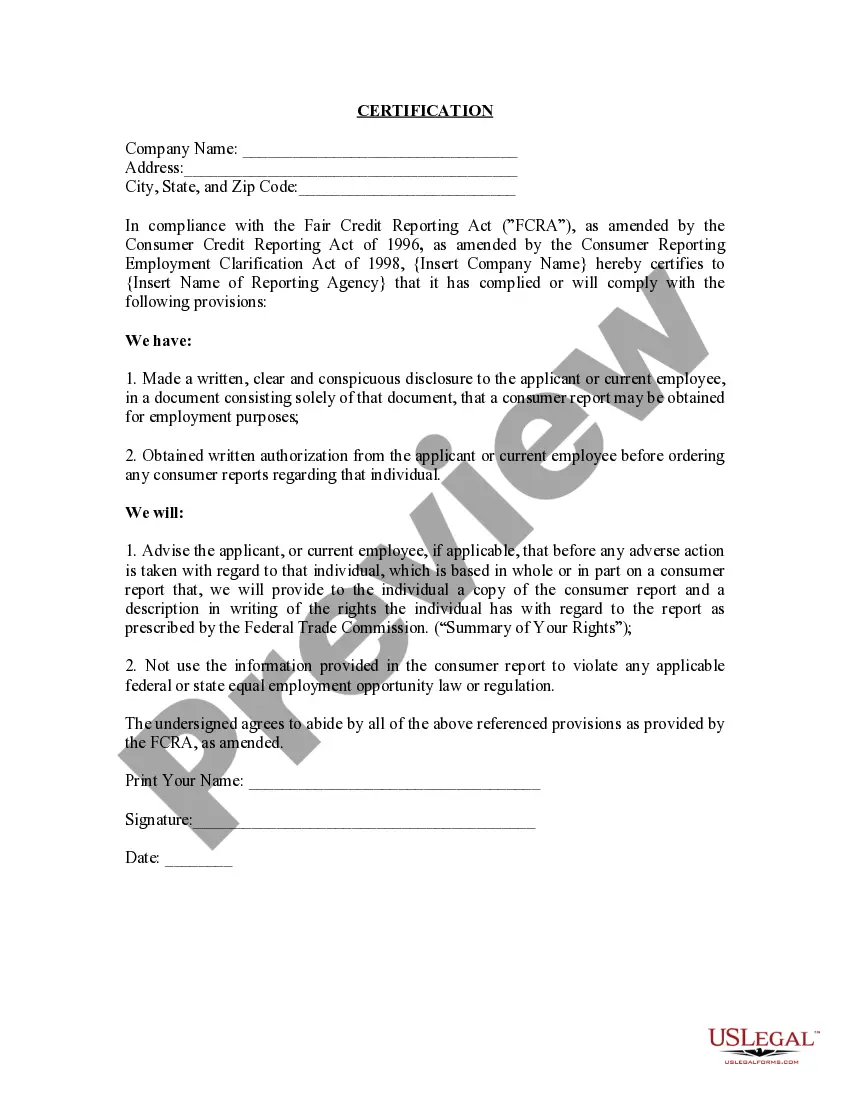

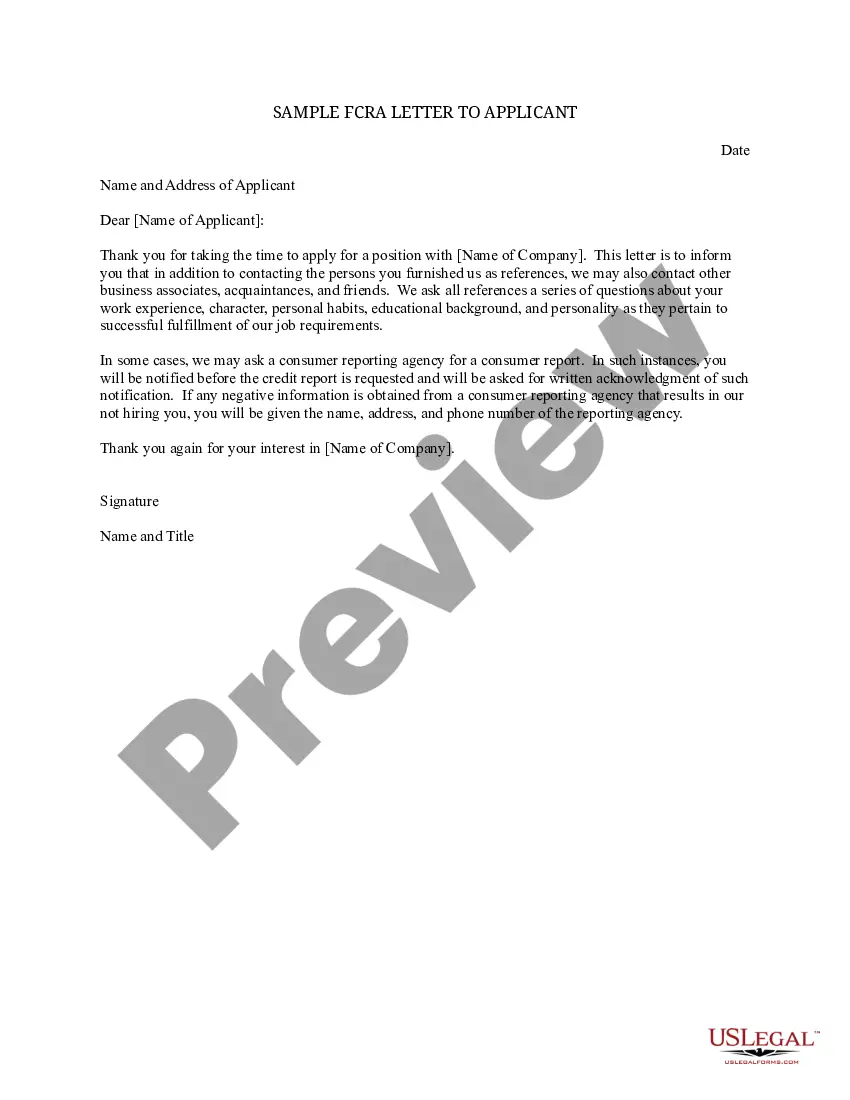

How to fill out FCRA Disclosure And Authorization Statement?

The Discrepancy Between Fcra And Facta you observe on this site is a reusable formal blueprint crafted by expert attorneys in accordance with federal and state statutes.

For over 25 years, US Legal Forms has supplied individuals, organizations, and legal specialists with more than 85,000 validated, state-specific documents for any business and personal situation. It’s the quickest, most straightforward, and most dependable way to acquire the paperwork you require, as the service ensures bank-level data protection and anti-malware safeguards.

Subscribe to US Legal Forms to have verified legal templates for every aspect of life readily available.

- Search for the document you require and assess it.

- Look over the sample you searched and preview it or examine the form description to verify it meets your requirements. If it does not, use the search bar to find the correct one. Click Buy Now once you have located the template you want.

- Register and Log In.

- Select the pricing option that fits you and create an account. Use PayPal or a credit card to make a swift payment. If you already possess an account, Log In and check your subscription to proceed.

- Obtain the fillable template.

- Choose the format you wish for your Discrepancy Between Fcra And Facta (PDF, Word, RTF) and download the example onto your device.

- Finish and endorse the document.

- Print out the template to complete it manually. Alternatively, use an online multi-functional PDF editor to quickly and accurately fill out and sign your form with a valid signature.

- Redownload your documents.

- Utilize the same document again whenever necessary. Access the My documents tab in your profile to redownload any previously retrieved forms.

Form popularity

FAQ

The Fair and Accurate Credit Transactions Act (FACTA) is intended to help prevent identity theft and credit-related fraud in an increasingly online economy. The law requires creditors and reporting agencies to protect consumers' identifying information and take steps to guard against identity theft.

Key Takeaways Investigative consumer reports contain information on an individual that is not in their credit report, including their "character, general reputation, personal characteristics, or mode of living" and are most often used by employers to check on job applicants.

FACTA amends the Fair Credit Reporting Act (FCRA) to: help consumers combat identity theft; establish national standards for the regulation of consumer report information; assist consumers in controlling the type and amount of marketing solicitations they receive; and.

It gives consumers the right to one free credit report a year from the credit reporting agencies, and consumers may also purchase, for a reasonable fee, a credit score along with information about how the credit score is calculated.

FACTA (Fair and Accurate Credit Transactions Act) is a federal law and amendment to the FCRA (Fair Credit Reporting Act). It was added to primarily protect consumers from identity theft.