Llc Stands For Limited Liability Corporation

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

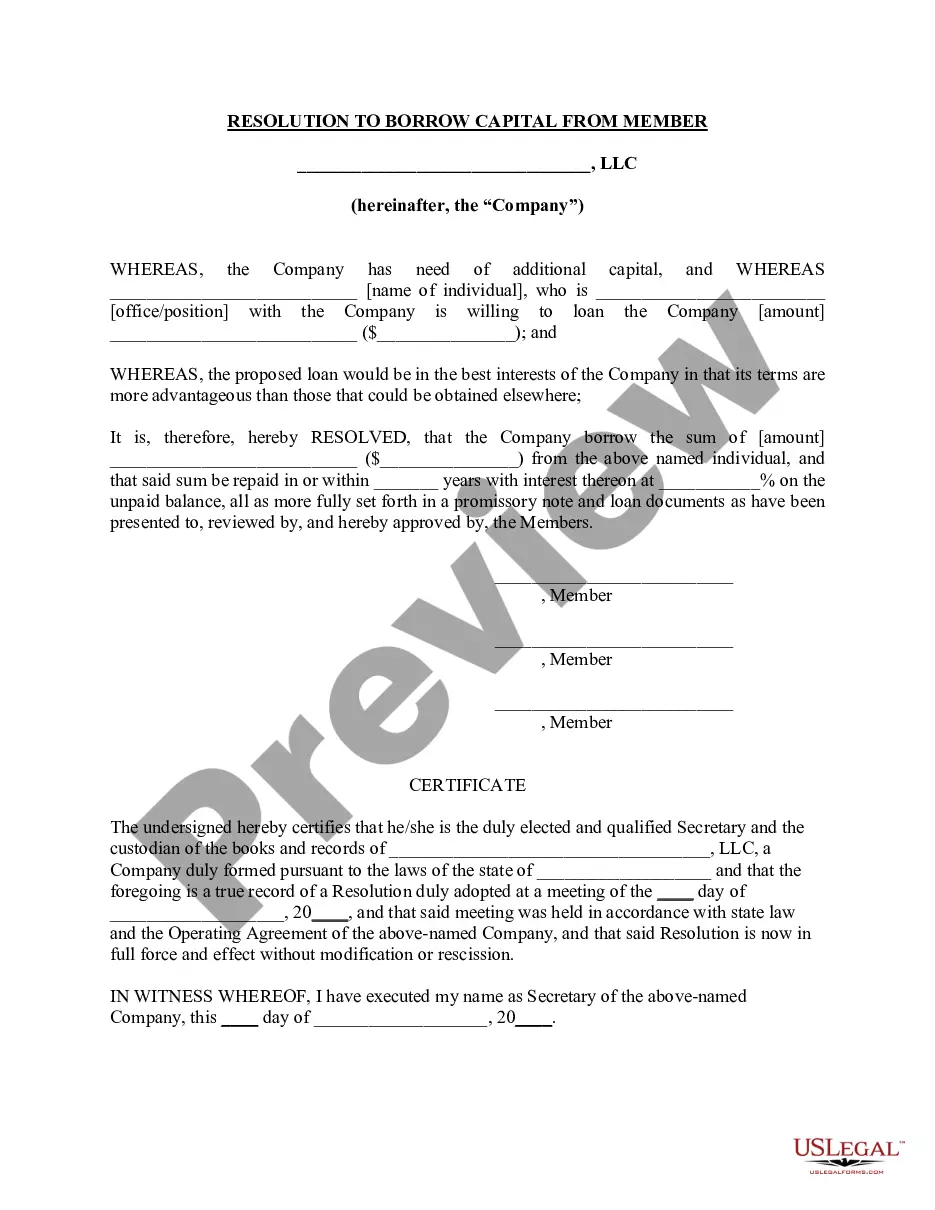

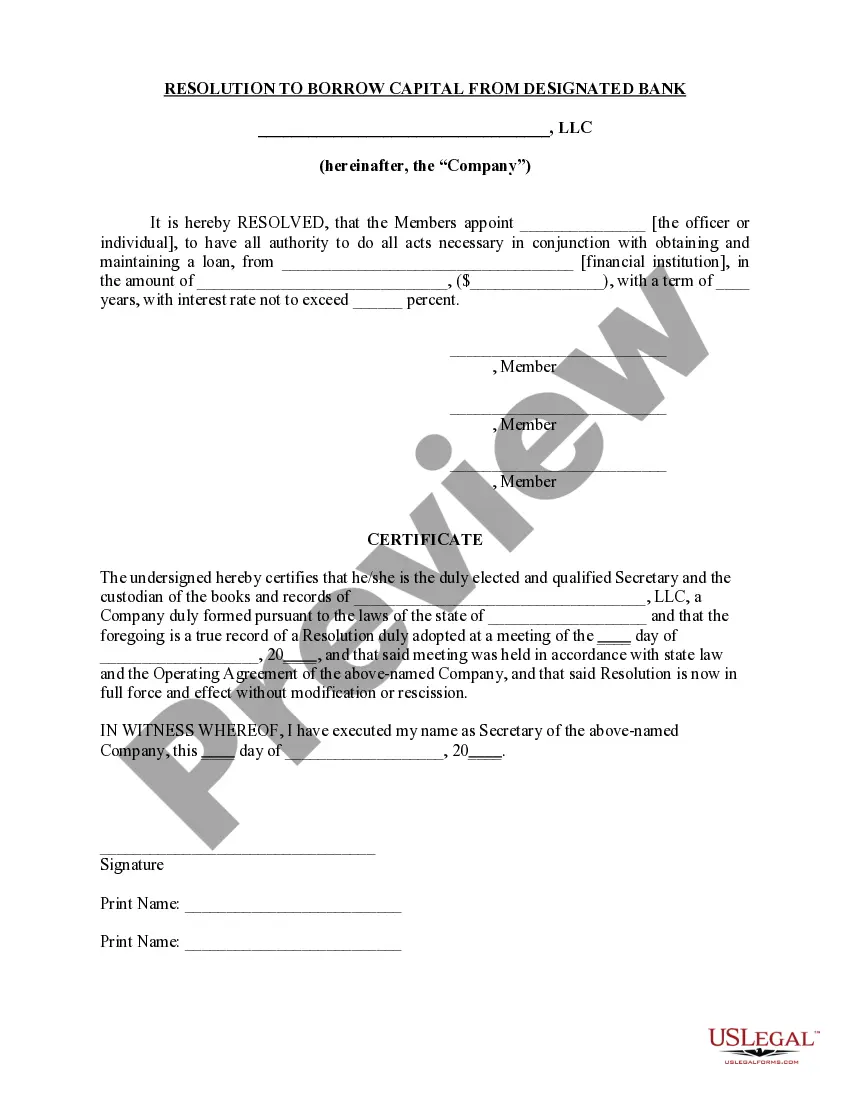

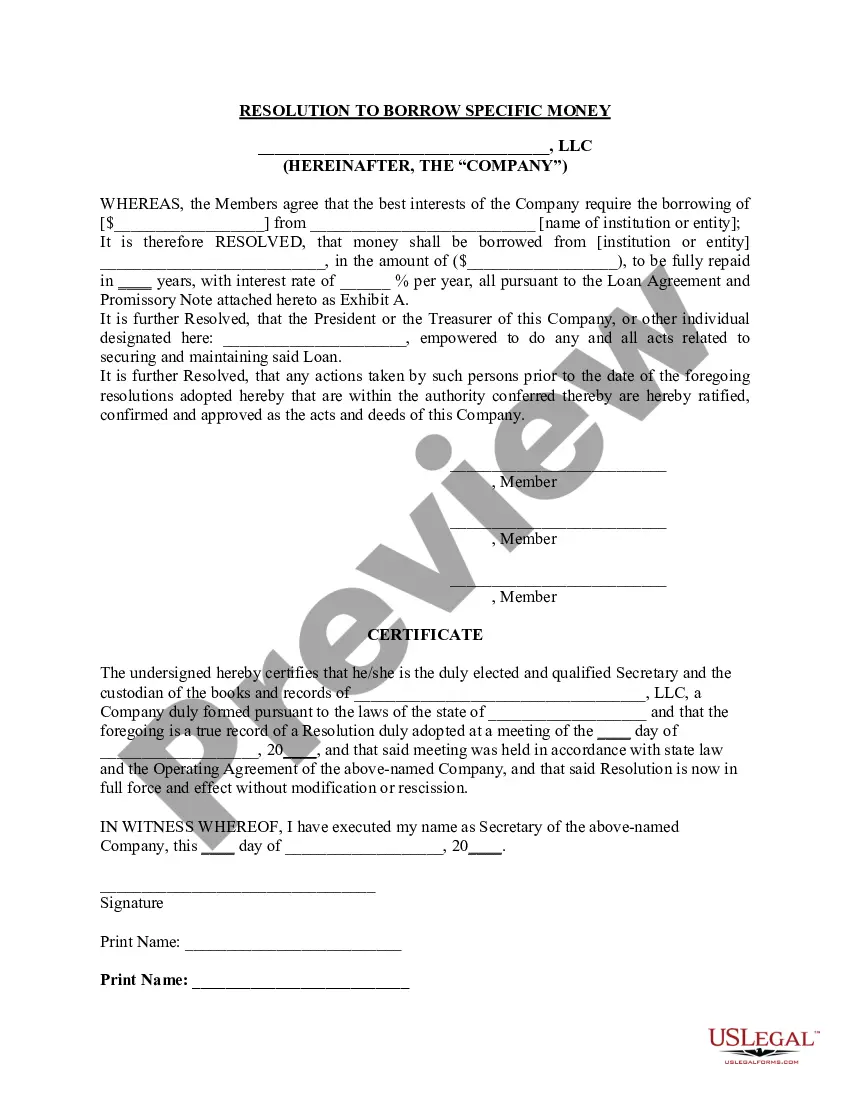

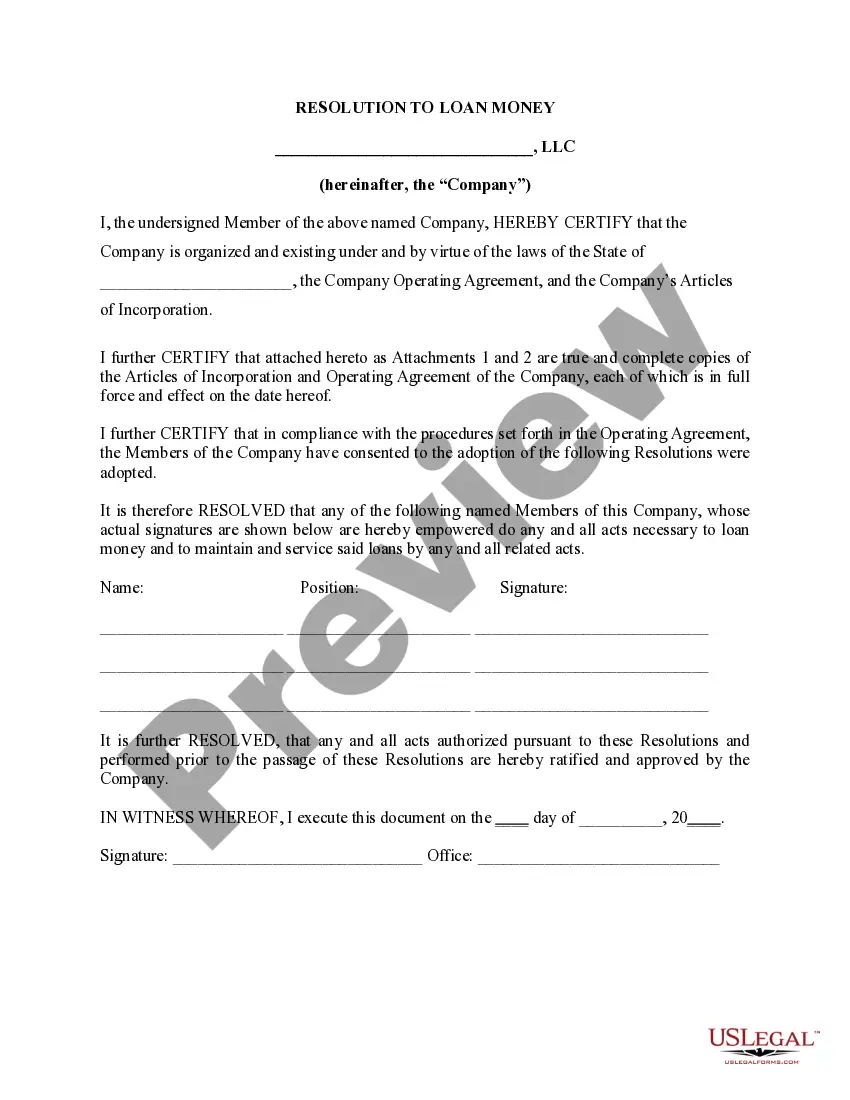

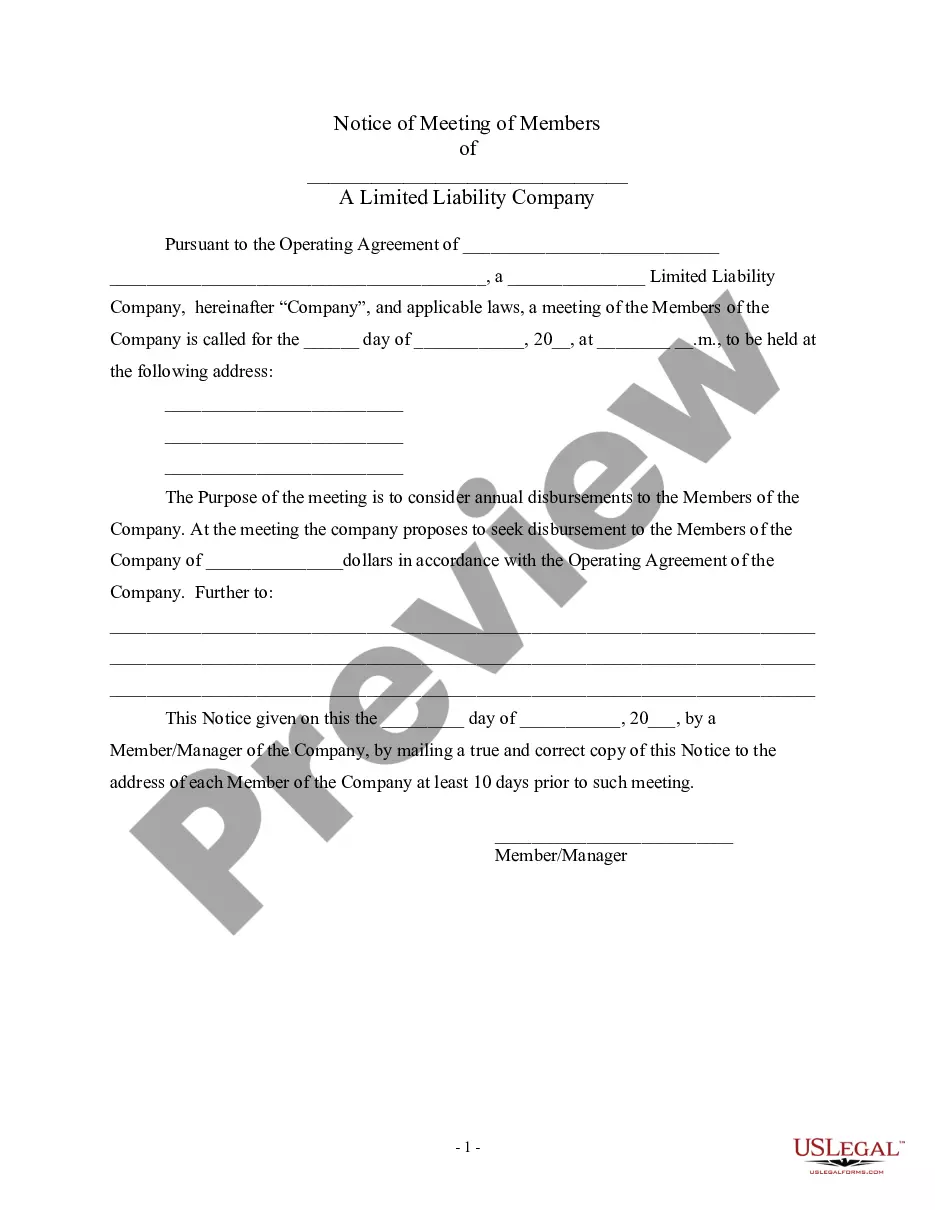

How to fill out Resolution Of Meeting Of LLC Members To Borrow Money?

- Preview the selected form and review its description to ensure it meets your requirements and local jurisdiction regulations.

- If you don't find the right template, utilize the Search tab to explore more options that fit your needs.

- Choose your preferred subscription plan and click the 'Buy Now' button to initiate the purchase process.

- Complete your payment using your credit card or PayPal account to finalize your transaction.

- Download the document to your device. You can access it later in the 'My Forms' section of your account.

By using US Legal Forms, not only do you gain access to a comprehensive collection of legal documents, but you also benefit from expert assistance for completing forms accurately.

Start your journey toward hassle-free legal documentation today! Visit US Legal Forms and empower yourself with the right tools for your business.

Form popularity

FAQ

LLC stands for limited liability corporation, but it is often referred to as a limited liability company. This designation provides owners with protection from personal liability for business debts, fostering an environment of entrepreneurship. Understanding the terminology is crucial for anyone considering starting a business entity. If you want to learn more about forming an LLC, consider exploring the vast resources available on the U.S. Legal Forms platform.

No, your LLC is not automatically classified as an S Corp. By default, LLCs are taxed as pass-through entities unless you elect to be taxed as an S Corporation through the IRS. To make this election, you need to file Form 2553 with the IRS. Remember that LLC stands for limited liability corporation, and understanding your tax classification can have significant implications for your business finances.

To determine if a company is an LLC or a C Corp, check the business name registration or state database for the entity type. LLCs typically include 'LLC' in their name, while C Corporations might include 'Inc.' or 'Corp.' However, this can vary by state, so verify with the appropriate state agency. It's important to clarify this distinction, as LLC stands for limited liability corporation, which provides different legal protections compared to a C Corporation.

Identifying whether your LLC is an S Corp or C Corp involves checking your IRS election forms. If you filed Form 2553 with the IRS, you've elected S Corporation status, while not filing this form generally means your LLC is taxed as a C Corporation by default. Additionally, your tax returns will reflect your elected status. Remember, LLC stands for limited liability corporation, and knowing your taxation classification can be vital for your financial planning.

To determine the classification of your LLC, you should review the formation documents filed with your state. Typically, an LLC can be classified as either a sole proprietorship or a partnership, based on the number of owners. Additionally, if you elected to be taxed as an S Corp or C Corp, that will also be noted in your tax filings. Keep in mind that LLC stands for limited liability corporation, and understanding your classification is key to managing taxes and legal protections.

To determine if your LLC is classified as an S or C corp, you will need to examine your tax election and business formation details. Keep in mind that an LLC is generally considered a limited liability corporation but can change its tax treatment. If you have filed for S corp status with the IRS, your LLC could be classified as such.

Deciding if your startup should be an S corp or C corp will depend on factors like your investment goals, the number of shareholders, and your future plans. An LLC, which stands for limited liability corporation, may offer a simpler tax structure but could benefit from the S corp election for certain startups. It’s wise to consult with a financial advisor or tax professional to make an informed decision.

To find out whether your LLC is classified as a C corp or S corp, review your tax elections and filings with the IRS. Remember, an LLC stands for limited liability corporation and does not automatically fall into either category. If you elected S corp status by filing Form 2553, it will reflect on your tax return.

Determining whether you are an S corporation or an LLC requires understanding your business structure. If your business is organized as an LLC, it stands for limited liability corporation and may choose to be taxed as an S corp. You should check your formation documents and any relevant tax filings to clarify your designation.

Choosing between an LLC and an LP (Limited Partnership) largely depends on your business goals. An LLC stands for limited liability corporation and offers personal liability protection to all its members. In contrast, an LP can expose general partners to personal liability, making LLCs a safer choice for many entrepreneurs.