Estate Distribution

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

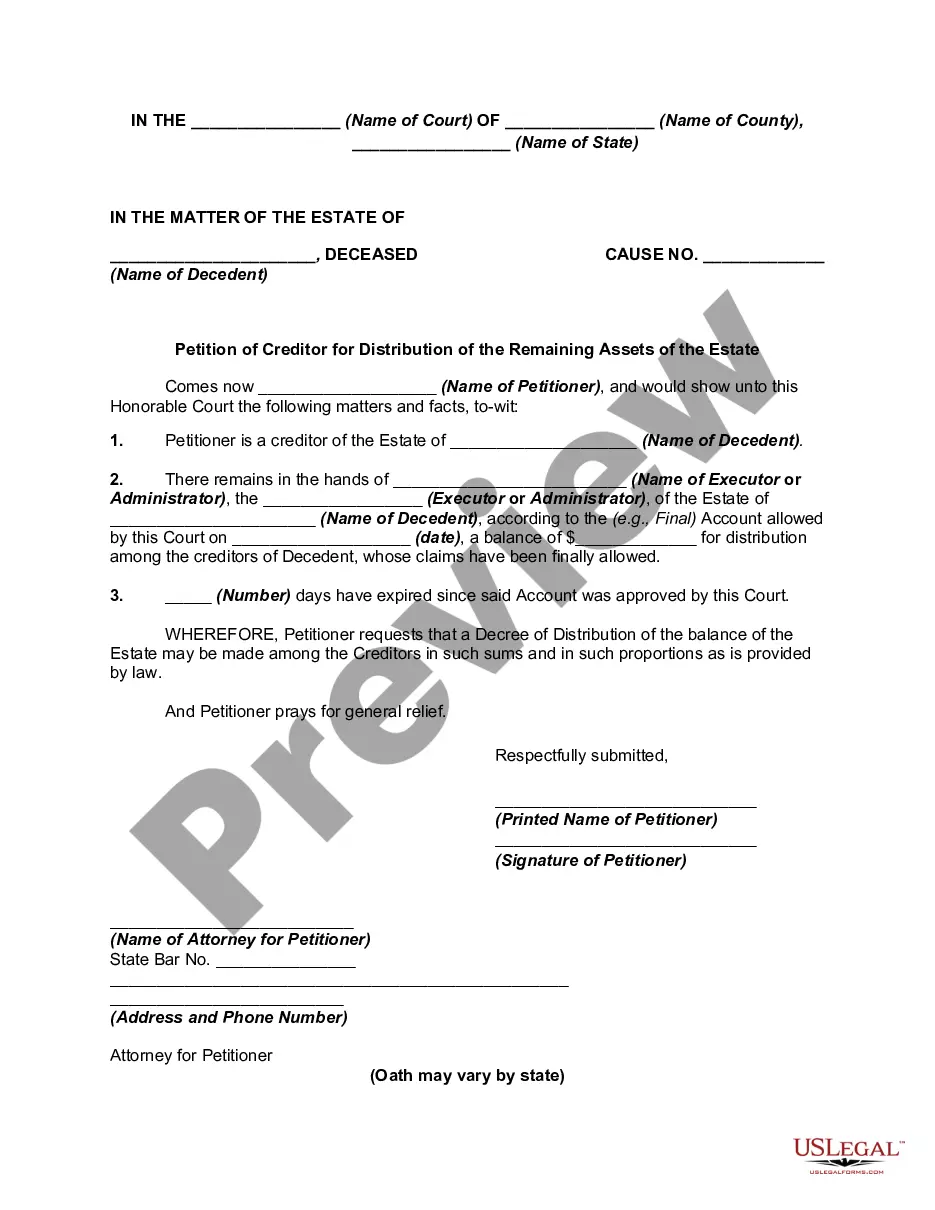

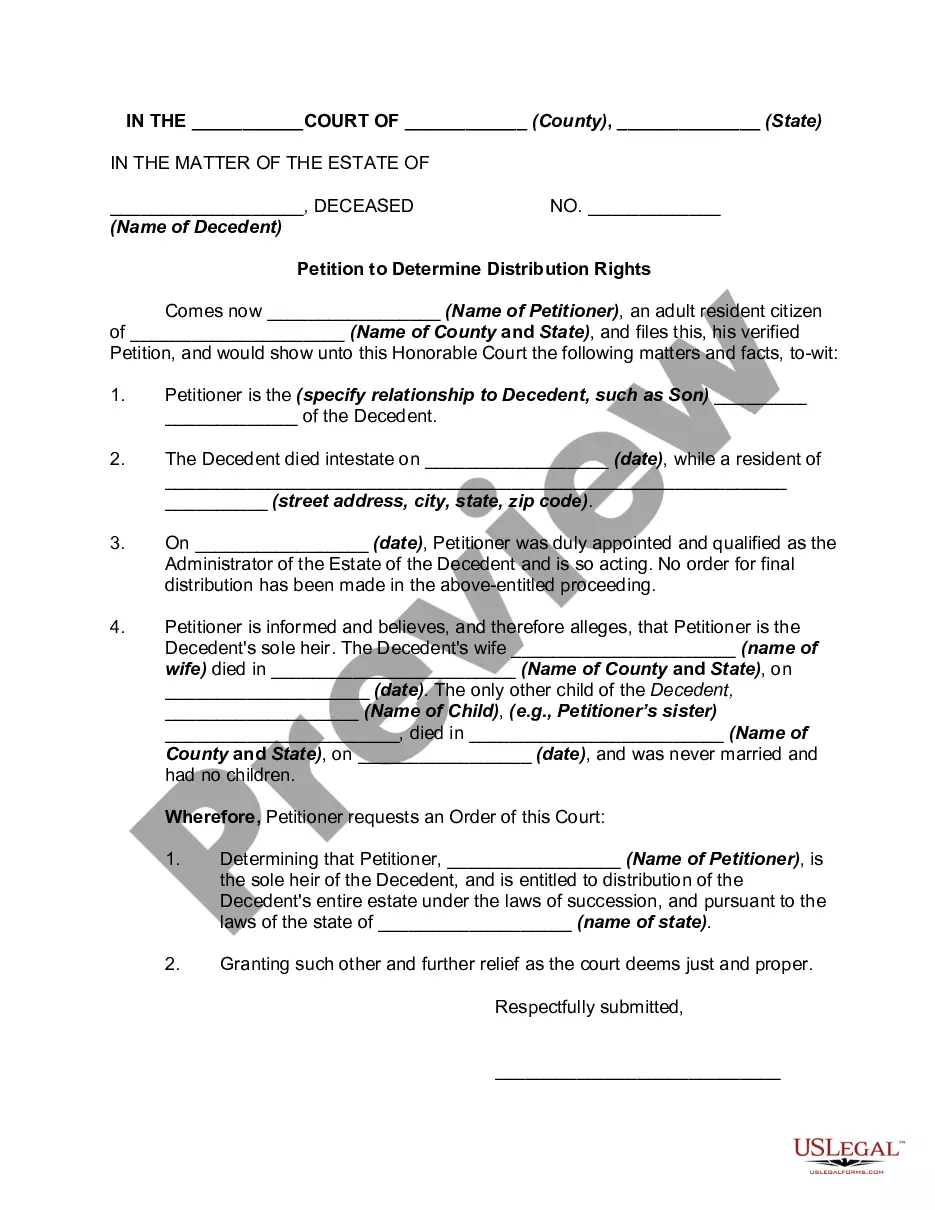

How to fill out Petition For Partial And Early Distribution Of Estate?

- Log in to your account on the US Legal Forms website. Ensure your subscription is current; if not, renew it based on your payment plan.

- If you're a new user, first review the form descriptions and preview modes to find the document that best fulfills your estate distribution needs.

- If necessary, utilize the search function to locate alternative templates that may align better with your requirements.

- Purchase the selected document by clicking the Buy Now button and choosing the subscription that best suits your needs. You’ll need to register for an account if you haven’t already.

- Complete your purchase by entering your payment information through credit card or PayPal.

- Download your form to your device, where you can also access it anytime from the My Forms section in your profile.

By utilizing US Legal Forms, you can ensure that your estate distribution documentation is handled with precision and in accordance with your local jurisdiction's requirements.

Don't hesitate to start your journey toward efficient estate planning—visit US Legal Forms today!

Form popularity

FAQ

When someone passes away, the executor usually has about nine months to file an estate tax return if the estate exceeds the federal thresholds. During this time, the estate distribution process begins, ensuring assets and debts are properly managed. It's advisable to consult with a legal expert to navigate the requirements effectively.

As of now, individuals can inherit up to $12.92 million without facing federal estate taxes, thanks to estate distribution exemptions. This threshold applies to the overall value of the estate, not each individual heir. It is essential to stay informed about any changes in tax laws that could affect future inheritances.

You typically do not need to report an inheritance to the IRS as income since inheritance is not considered taxable income. However, the estate distribution process may involve tax obligations for the estate itself, especially if it surpasses certain thresholds. If the estate is subject to taxes, then it is crucial to understand how this might affect the overall distribution to beneficiaries.

In general, you do not receive a 1099-S for inheritance unless you sell the inherited property. When you inherit property, the estate distribution does not trigger a 1099-S form. However, if you choose to sell that property later, the IRS requires the reporting of the sale, and that's when you might receive a 1099-S.

Estate distribution is the process of dividing and transferring assets from a deceased person's estate to the designated beneficiaries or heirs. This process can be straightforward if a valid will is in place, guiding the executor in fulfilling the wishes of the deceased. Familiarizing yourself with the estate distribution process can help clarify rights and expectations during this sensitive time.

Distributions from an estate can have tax implications, but they are typically not considered income for the beneficiaries. However, certain assets may generate taxes, such as capital gains or income generated from estate assets. To navigate these complexities, consulting with a tax advisor who understands estate distribution is highly recommended.

The best way to distribute estate assets often involves clear communication and planning among the beneficiaries. Using a structured approach, such as creating a detailed inventory and addressing any outstanding debts or taxes, helps streamline the estate distribution process. Platforms like uslegalforms can provide valuable resources and templates to assist in managing these distributions effectively.

The distribution of the estate of the deceased means allocating the assets held in the estate according to the will or state laws. Executors or administrators are responsible for this distribution, ensuring that all debts are settled before assets are transferred to beneficiaries. This process is central to estate management and helps maintain harmony among heirs.

The distribution of inheritance refers to the process through which an individual receives their share of a deceased person's estate. This distribution can occur through a will or by intestate succession laws if no will exists. Understanding your rights and the procedures associated with inheritance distribution is vital for a smooth transition of assets.

Generally, distributions from an estate do not count as taxable income for the beneficiaries. Instead, they represent a transfer of property, not earnings. However, tax implications may arise depending on the type of asset received, so it’s important to consult with a tax professional to understand any potential tax obligations related to estate distribution.