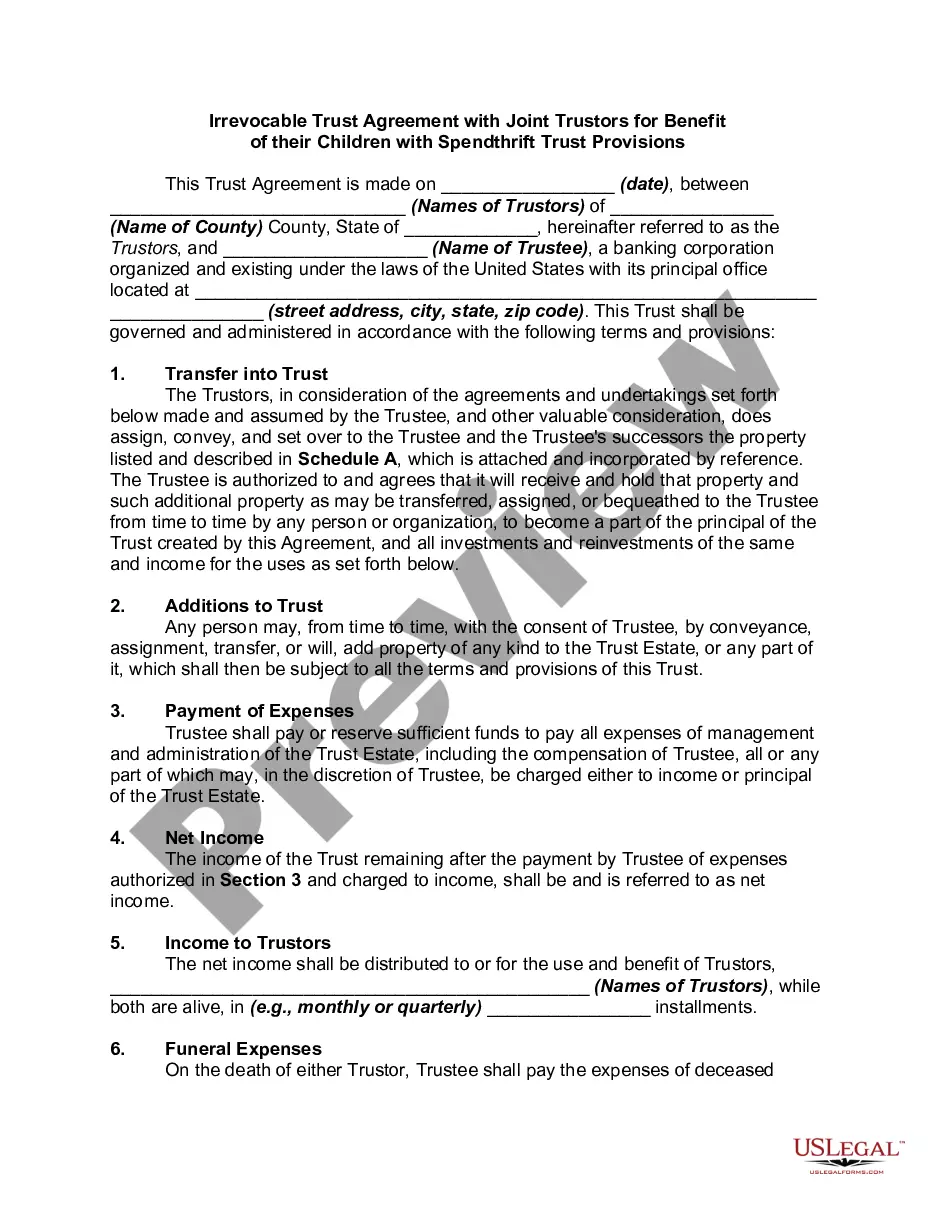

Irrevocable Living Trusts With Us

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Irrevocable Trust Agreement For Benefit Of Trustor's Children And Grandchildren With Spendthrift Trust Provisions?

- Visit the US Legal Forms website and log in to your existing account. Ensure your subscription is current to access all features.

- For new users, start by checking the preview mode and form details to find the right irrevocable living trust template that suits your local legal requirements.

- If you need additional forms, use the search bar to locate alternatives that fit your criteria.

- Once you've found the correct document, click on the 'Buy Now' button and select your preferred subscription plan. Registration may be required to proceed.

- Complete your purchase by entering your payment information, either through credit card or PayPal.

- Download the form to your device, allowing you to fill it out at your convenience. You can also access it anytime from the 'My Forms' section of your account.

By using US Legal Forms, you benefit from a rich collection of over 85,000 legal forms and packages, ensuring you find exactly what you need.

Start your estate planning today with us and secure your future. Don't wait, visit US Legal Forms now!

Form popularity

FAQ

Yes, you can file your own irrevocable trust, but it's crucial to do so correctly to avoid legal headaches. You must follow specific steps, like drafting the trust document and obtaining an EIN, and make sure it meets your state’s regulations. By utilizing irrevocable living trusts with us, you gain valuable insights and tools that can streamline your filing process, making it less overwhelming.

While it is possible to create an irrevocable trust without an attorney, it is not recommended due to the complexities involved. Legal guidance ensures that the trust meets all legal requirements and properly reflects your intentions. With irrevocable living trusts with us, you can access resources and templates that simplify the process, making it easier for you to establish a solid legal foundation.

To file an irrevocable trust with the IRS, you need to obtain an Employer Identification Number (EIN) for the trust. After that, you must file Form 1041 for income tax purposes if the trust generates income. Working with irrevocable living trusts with us can help you manage this process effectively, ensuring you comply with all IRS regulations and deadlines.

An irrevocable trust does not always have to be filed with the court, but some states may require it to be registered. Generally, you should keep the trust document in a safe place, as it provides legal proof of the trust's existence and its terms. If you're using irrevocable living trusts with us, we can guide you through any filing requirements specific to your state, ensuring compliance with local laws.

Yes, you can set up an irrevocable trust for yourself. However, once you've created it, you cannot change its terms or reclaim the assets you transferred into it. This type of trust allows you to manage your assets while securing them from taxes and probate, providing financial benefits for your beneficiaries. Explore irrevocable living trusts with us to simplify this process and protect your legacy.

Avoiding inheritance tax with a trust in the USA is possible when you strategically structure your irrevocable living trusts with us. By placing your assets in an irrevocable trust, you can effectively remove them from your taxable estate. This not only safeguards your wealth for your heirs, but also minimizes potential tax liabilities, ensuring a smoother inheritance process for your loved ones.

The 5-year rule for irrevocable living trusts with us refers to the period during which assets transferred into the trust must remain there to be exempt from Medicaid's look-back requirement. If you apply for Medicaid benefits within five years of transferring your assets, your eligibility may be affected. Understanding this rule helps you plan your asset transfers strategically to protect your wealth from future care costs.

One major disadvantage of irrevocable living trusts with us is that once assets are transferred into the trust, you can't remove them or make changes without the consent of the beneficiaries. This can limit your control over your assets and financial flexibility. Additionally, these trusts may have higher legal fees and administrative costs compared to revocable trusts, making it essential to weigh the benefits against the potential downsides.

The recent changes in regulations surrounding irrevocable living trusts with us primarily focus on tax implications and reporting requirements. Many states have updated their laws to enhance transparency and compliance for trust administration. As such, it's crucial to stay informed about these changes to ensure your trust remains compliant and beneficial for your estate planning.

Yes, irrevocable living trusts with us can protect your assets from being depleted due to nursing home costs. Once your assets are placed in an irrevocable trust, they are no longer considered part of your personal estate, which helps shield them from Medicaid spend-down requirements. This strategy allows you to maintain your wealth while ensuring that you can receive long-term care without losing everything you've worked for.