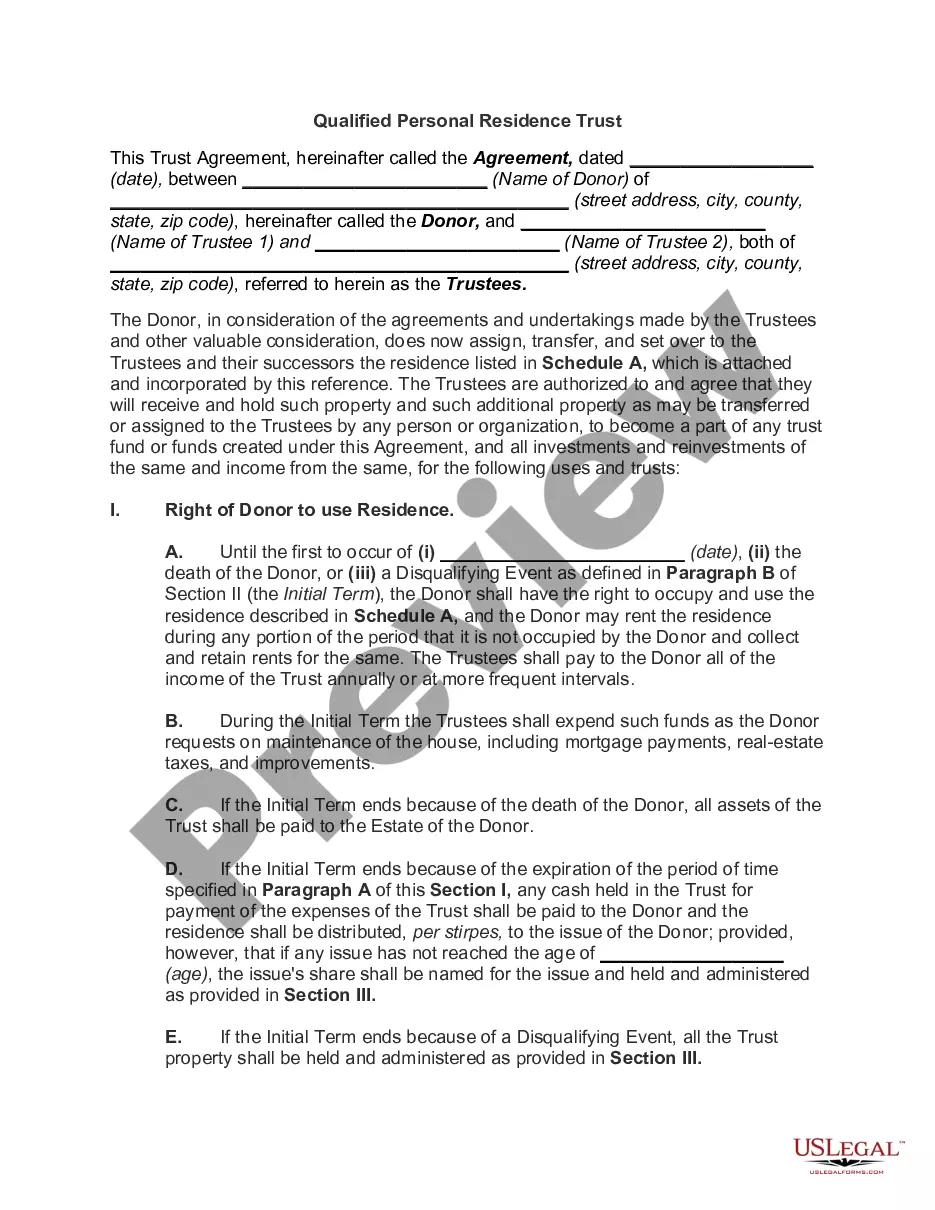

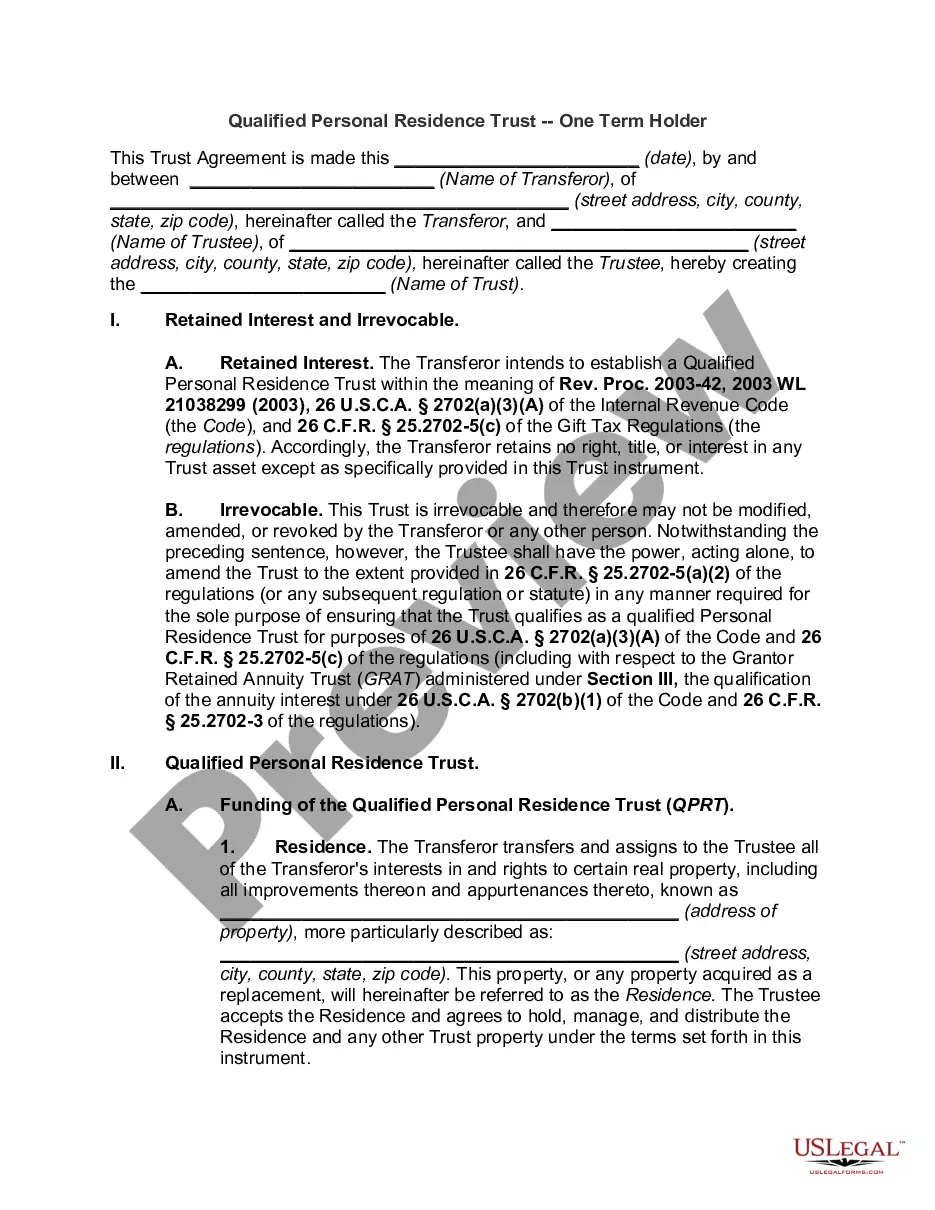

Trust Personal Residence With Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Personal Residence Trust?

The Trust Personal Residence With Trust you see on this page is a multi-usable formal template drafted by professional lawyers in line with federal and local laws and regulations. For more than 25 years, US Legal Forms has provided people, organizations, and attorneys with more than 85,000 verified, state-specific forms for any business and personal occasion. It’s the fastest, simplest and most reliable way to obtain the paperwork you need, as the service guarantees bank-level data security and anti-malware protection.

Acquiring this Trust Personal Residence With Trust will take you just a few simple steps:

- Browse for the document you need and check it. Look through the file you searched and preview it or review the form description to verify it fits your needs. If it does not, utilize the search bar to get the appropriate one. Click Buy Now once you have found the template you need.

- Subscribe and log in. Choose the pricing plan that suits you and create an account. Use PayPal or a credit card to make a prompt payment. If you already have an account, log in and check your subscription to proceed.

- Get the fillable template. Choose the format you want for your Trust Personal Residence With Trust (PDF, Word, RTF) and download the sample on your device.

- Fill out and sign the paperwork. Print out the template to complete it by hand. Alternatively, use an online multi-functional PDF editor to quickly and precisely fill out and sign your form with a valid.

- Download your paperwork one more time. Make use of the same document again anytime needed. Open the My Forms tab in your profile to redownload any earlier saved forms.

Subscribe to US Legal Forms to have verified legal templates for all of life’s situations at your disposal.

Form popularity

FAQ

Most QPRTs do not generate any income and an income tax return is not typically required. If the property generates income, a Grantor Trust Tax Return, Form 1041, may be required.

One of the main disadvantages of a QPRT is the loss of stepped-up basis. When you own real estate and you pass it to a beneficiary through your Will, your beneficiary receives it with an income tax basis equal to the fair market value of the house at the time of death.

All appreciation from the date of your acquisition through the date of your death disappears. This is called a ?stepped-up basis?. When the beneficiary sells the property, he or she only pays capital gain on the appreciation (adjusted for capital improvements) from the date of your death through the date of sale.

The principal residence exclusion under section 121 allows an individual or married couple to exclude up to $250,000 or $500,000 of gain on the sale of a primary residence. But since an irrevocable trust is not a natural person, it is typically not allowed to use this exclusion. However, there are a few exceptions.

The key disadvantages of placing a house in a trust include the following: Extra paperwork: Moving property in a trust requires the house owner to transfer the asset's legal title. This involves preparing and signing an additional deed, and some people may consider this cumbersome.