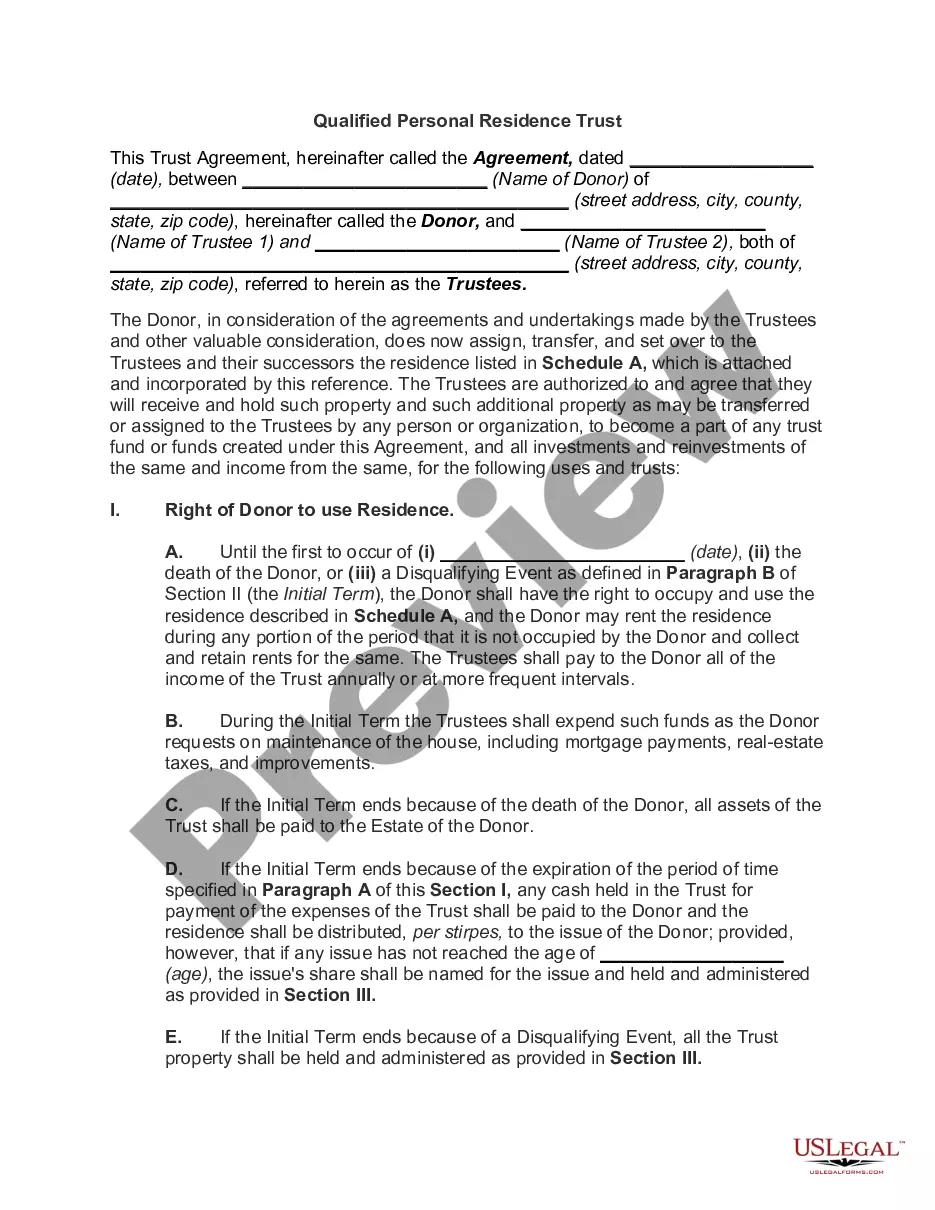

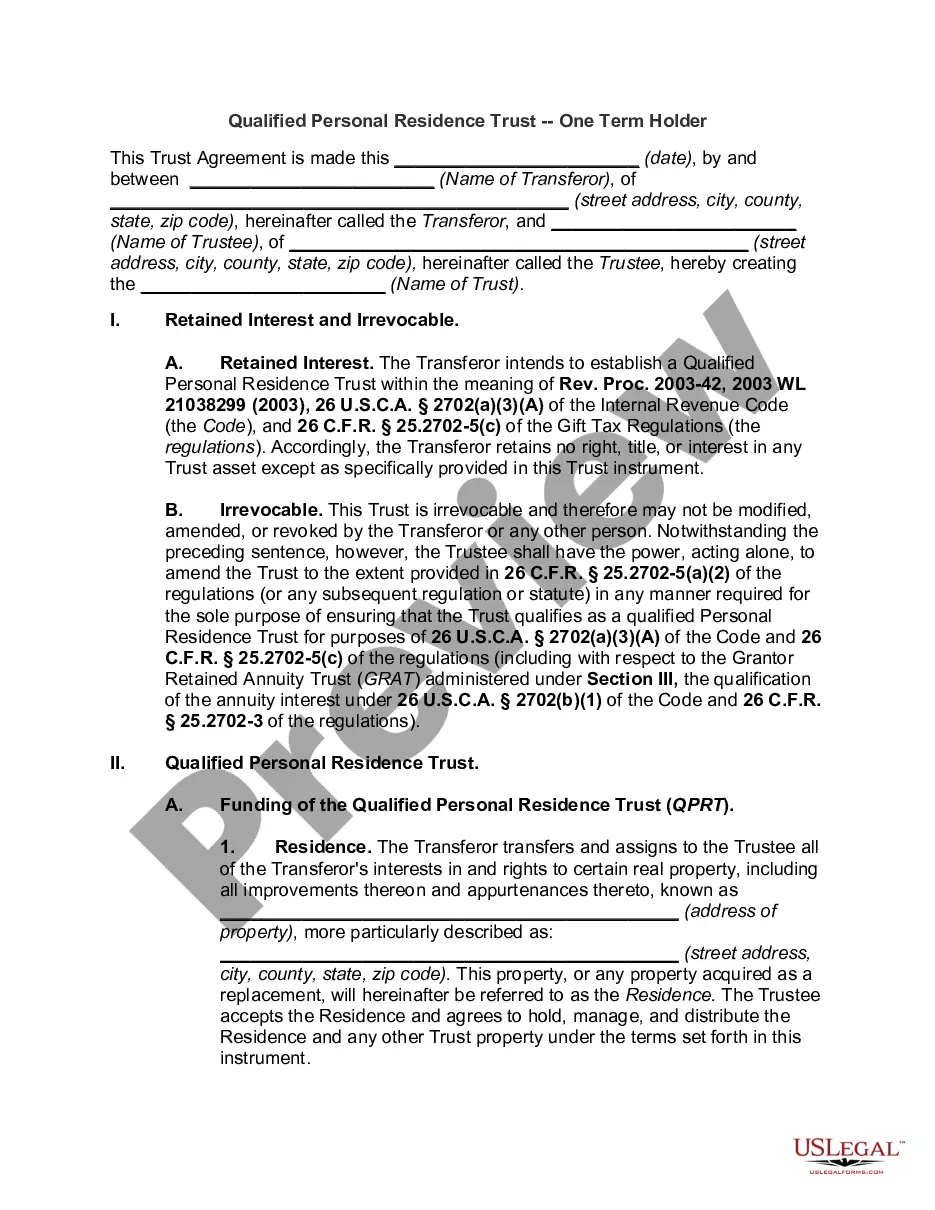

Personal Residence Real For Sale

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Personal Residence Trust?

Finding a reliable location to obtain the latest and pertinent legal templates is a significant part of navigating through bureaucracy.

Selecting the appropriate legal documents requires precision and meticulousness, which is why it is essential to source Personal Residence Real For Sale samples only from trustworthy providers, such as US Legal Forms. An incorrect template could waste your time and delay your current situation.

Once you have the form on your device, you can modify it using the editor or print it out to complete it by hand. Eliminate the complications associated with your legal documents. Browse through the extensive US Legal Forms library, where you can find legal samples, assess their applicability to your circumstances, and download them right away.

- Use the library navigation or search box to find your template.

- Access the information of the form to determine if it meets the regulations of your state and locality.

- Preview the form, if available, to confirm it is the one you need.

- Return to the search function and seek out the suitable template if the Personal Residence Real For Sale does not align with your requirements.

- If you are confident about the form's applicability, download it.

- As a verified customer, click Log in to validate and access your selected forms in My documents.

- If you haven't created an account yet, click Buy now to obtain the template.

- Choose the pricing option that best fits your needs.

- Proceed with the registration to complete your purchase.

- Finalize your transaction by selecting a payment method (credit card or PayPal).

- Select the document format for downloading Personal Residence Real For Sale.

Form popularity

FAQ

When you sell your personal residence real for sale, you need to report the transaction on Schedule D of your tax return, which details capital gains and losses. If you meet certain conditions, you might qualify to exclude part of the gain from your income. The IRS allows you to exclude up to $250,000 of gain if you are single, and up to $500,000 if you are married and filing jointly. For accuracy and ease, consider using tools from US Legal Forms to help with your tax reporting.

The 3 year rule for capital gains highlights a specific timeframe for payment exemptions when selling your primary residence. This rule can apply if you only meet certain criteria during the ownership period. Familiarizing yourself with this is crucial as you explore personal residence real for sale, ensuring you capitalize on potential tax savings. Proper planning can enhance your financial outcome when selling your home.

The 2 5 year rule states that you may exclude capital gains on the sale of your primary home if you have lived there for at least 2 out of the last 5 years. This rule is essential when considering your options in the real estate market, especially when browsing personal residence real for sale. It provides significant tax benefits for homeowners looking to sell. By understanding the nuances of this rule, you can maximize your financial gain from selling your property.

The 6 year rule allows homeowners to exclude capital gains from the sale of their personal residence if they owned and lived in the home for at least 2 of the 5 years prior to the sale. This rule is especially beneficial when you are looking for personal residence real for sale, as it enables sellers to keep more profit from their property. It encourages stability in homeownership and promotes investment in real estate. Understanding this rule can help you make informed decisions when selling your property.

To prove your primary residence for capital gains, gather documentation that shows your occupancy. You can use utility bills, tax returns, or your driver's license to establish that this is where you live. These documents help demonstrate that your home meets the criteria for a personal residence real for sale. Additionally, keeping records of your time spent at the property can strengthen your case.

Yes, the sale of personal property typically must be reported if it generates income. If you sell personal belongings for a profit, it is advisable to report it on your tax return. To ensure compliance and keep everything clear, document all transactions related to the sale of personal residence real for sale and all other personal property.

You can avoid capital gains on the sale of your personal residence by taking advantage of the home sale tax exclusion, which allows you to exclude significant gains if you meet certain ownership requirements. Documenting your renovations and improvements can also lower your taxable gain. Use tools and resources from platforms like uslegalforms to navigate the paperwork involved in selling personal residence real for sale.

To report the sale of your primary residence to the IRS, you’ll need to complete Schedule D and Form 8949, in addition to including any gains or losses on your Form 1040. It is essential to accurately calculate your adjusted basis, and ensure you apply any exclusions correctly. Properly reporting the sale of personal residence real for sale will help you avoid unwanted taxes and provide clarity for future transactions.

Yes, you typically must report the sale of your primary residence to the IRS unless you qualify for the home sale tax exclusion. Even if you do not owe taxes on a gain, the sale may still need to be reported. Failing to report can cause issues later, so always disclose the sale of personal residence real for sale when filing your taxes.

The sale of real estate is reported to the IRS using Form 1099-S, which reports the proceeds from the sale. Both the seller and the buyer may receive a copy of this form. To correctly file, you will need to include this information when you report the sale of personal residence real for sale on your tax return. This ensures transparency and compliance with IRS regulations.