Form For Irrevocable Life Insurance Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

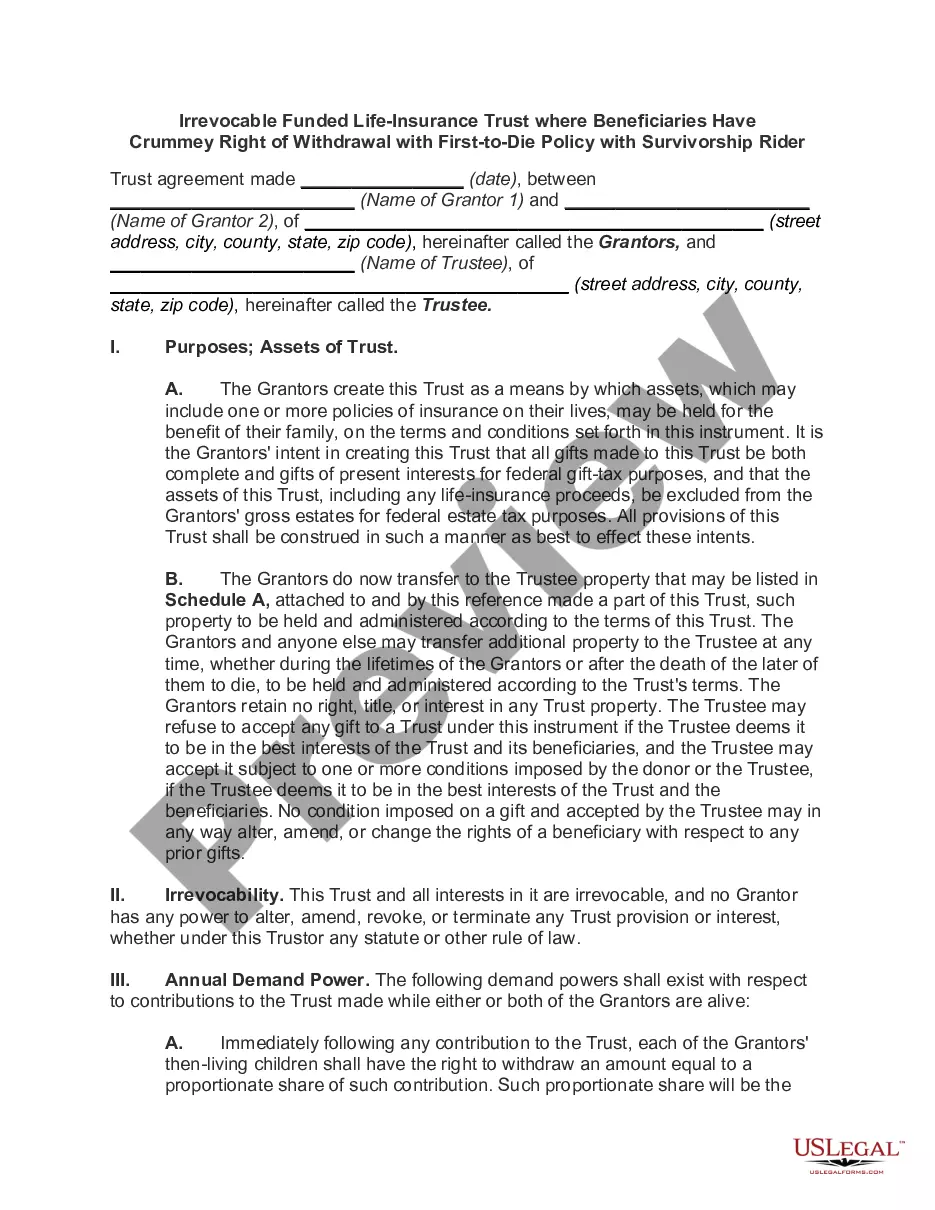

The primary disadvantage of an irrevocable life insurance trust is the lack of control over the assets once they are transferred. Moreover, establishing one can involve complex legal and financial considerations. You must also prepare for potential tax obligations. Exploring a form for irrevocable life insurance trust can help you navigate these disadvantages effectively.

An irrevocable life insurance trust can be a beneficial estate planning tool. It helps to protect your assets from taxes and creditors while providing for your beneficiaries. However, it is crucial to assess your individual situation before deciding. A form for irrevocable life insurance trust can guide you in evaluating your options.

Filling out an irrevocable trust involves several steps, such as clearly identifying the trustors, beneficiaries, and the assets involved. It is essential to provide detailed information to ensure the trust meets your objectives. Utilizing a form for irrevocable life insurance trust simplifies this process, guiding you through each section.

Yes, you typically need to file a tax return for an irrevocable life insurance trust, especially if it generates income. The trust itself is responsible for any applicable taxes. Using a form for irrevocable life insurance trust can help you organize necessary information for accurate tax filing.

An irrevocable trust can limit your control over assets once established. This means you cannot make changes or revoke the trust easily. Additionally, if not set up correctly, it may lead to unintended tax implications. Consider using a form for irrevocable life insurance trust to help mitigate these risks.

A common mistake parents make when setting up a trust fund is not clearly defining the trust's terms or not communicating the purpose to their heirs. Without clear guidance, beneficiaries may misunderstand their roles, leading to disputes. To avoid this, use the form for irrevocable life insurance trust with detailed provisions that reflect your wishes, ensuring clarity for all involved.

Yes, an irrevocable life insurance trust must file a tax return if it earns income above a certain threshold. Since the trust is a separate legal entity, it has its own tax obligations. Be sure to keep accurate records of any income or expenses associated with the trust. Utilizing our form for irrevocable life insurance trust can help clarify these requirements.

Yes, you can prepare your own irrevocable trust if you have a good understanding of legal requirements. However, it is advisable to consult with a legal professional to ensure all aspects are properly addressed. Using a reliable platform, like uslegalforms, can provide you with the right template. The form for irrevocable life insurance trust simplifies the process and minimizes the risk of errors.

The main downside of an irrevocable trust is the loss of control over the assets placed in the trust. Once you establish it, you cannot modify or revoke it without the consent of the beneficiaries. This means you must be confident in your decisions when creating the trust. However, the benefits often outweigh the drawbacks, especially for estate planning purposes.

To create an irrevocable life insurance trust, start by selecting a trustee who will manage the trust. Next, draft the trust document, specifying the terms and beneficiaries. You'll then transfer ownership of a life insurance policy to the trust, using our easy-to-use form for irrevocable life insurance trust. This structured approach helps you protect your assets effectively.