Modify Interest Rate With Credit Card

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

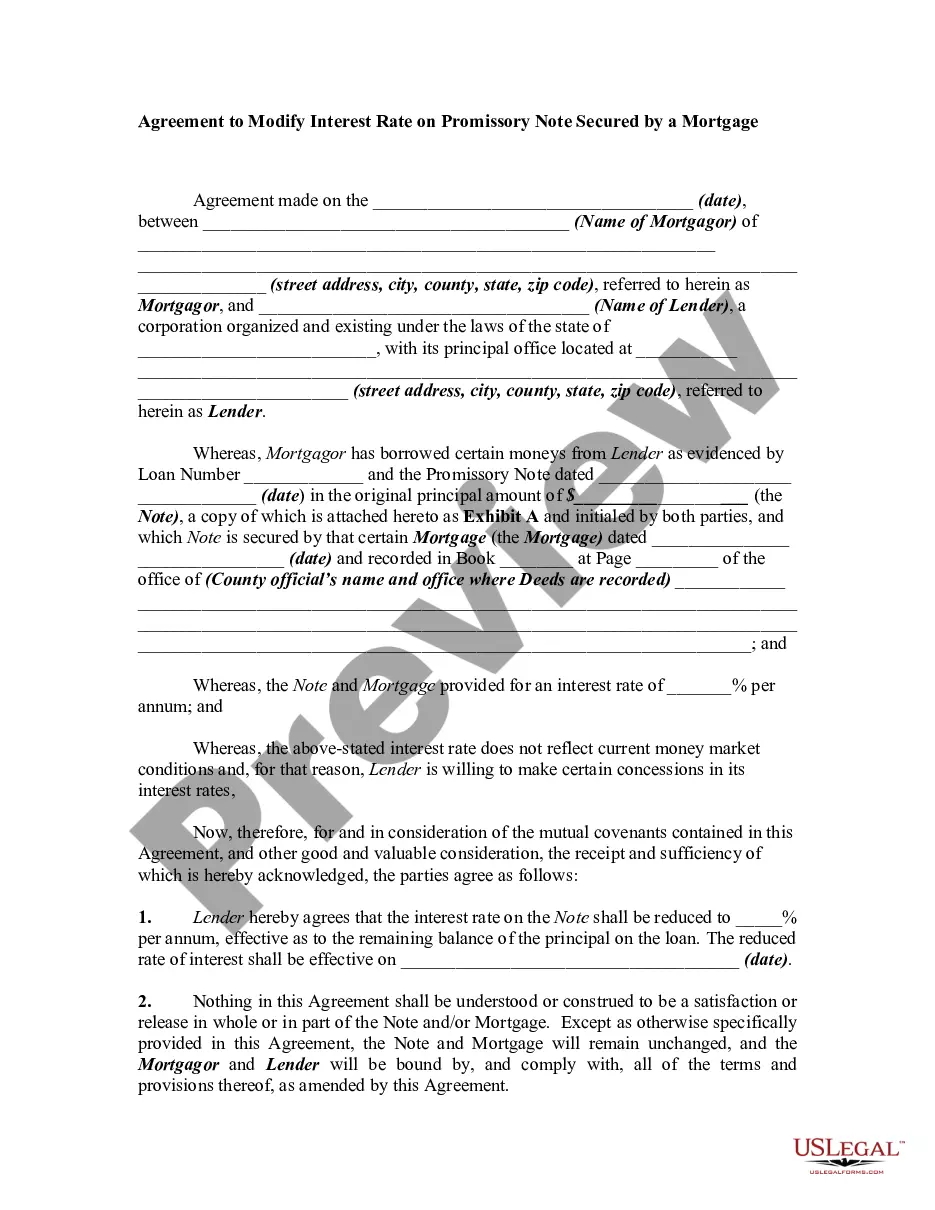

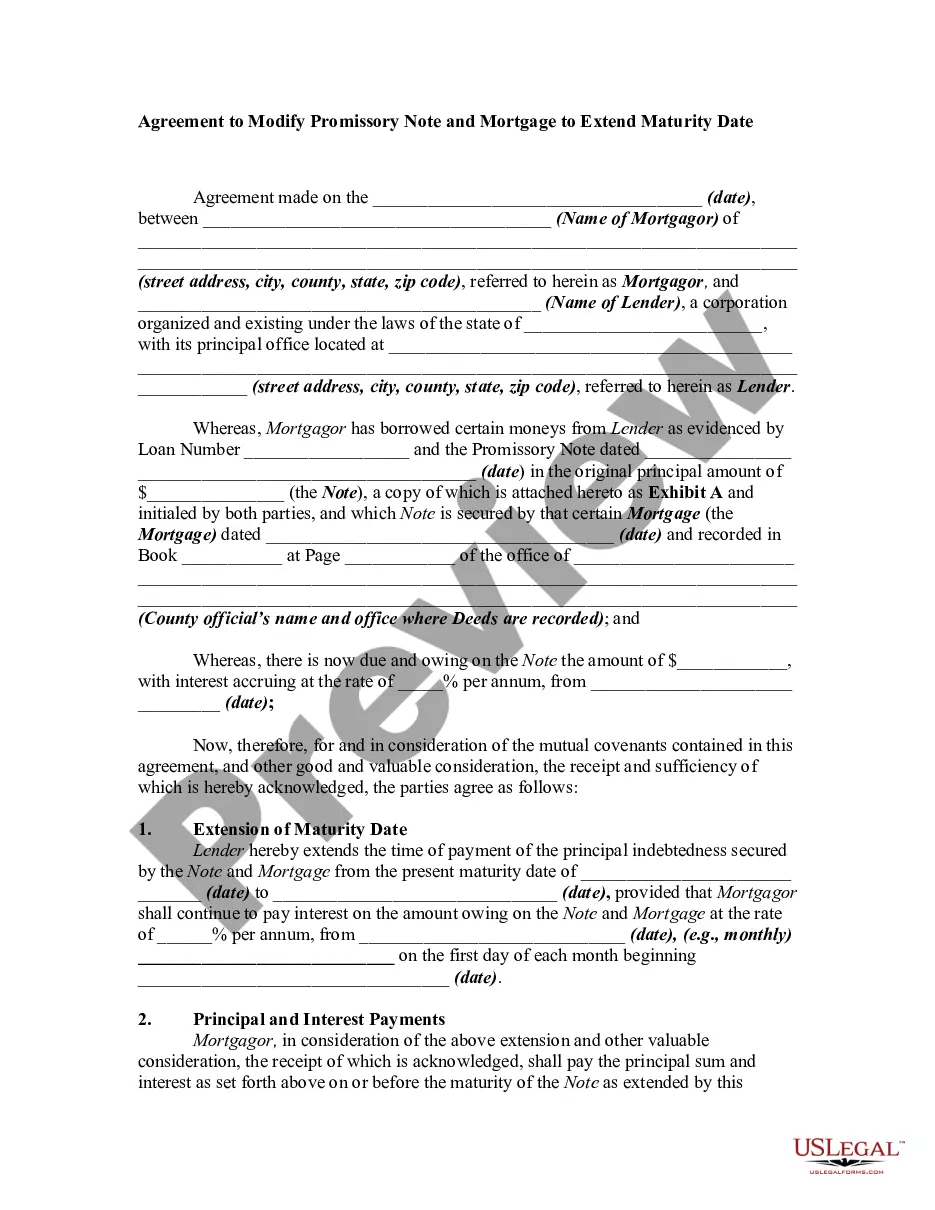

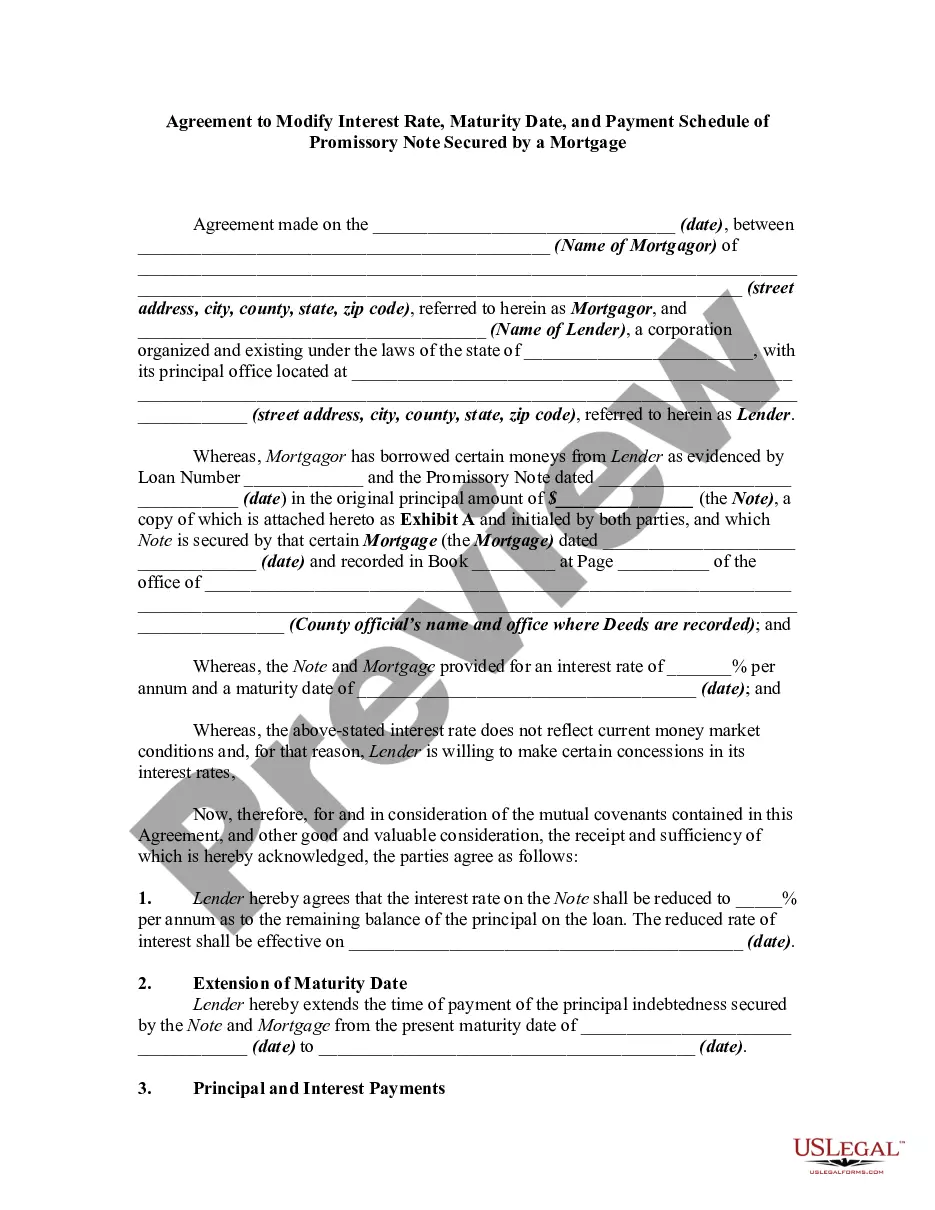

How to fill out Agreement To Change Or Modify Interest Rate, Maturity Date, And Payment Schedule Of Promissory Note Secured By A Deed Of Trust?

The Adjust Interest Rate With Credit Card you see on this page is a versatile legal template crafted by expert attorneys in accordance with federal and state laws and regulations.

For over 25 years, US Legal Forms has offered individuals, organizations, and legal professionals more than 85,000 validated, state-specific forms suitable for any business and personal scenario. It’s the quickest, simplest, and most reliable means to acquire the documents you require, as the service assures the utmost level of data security and anti-malware safeguards.

Select the format you prefer for your Adjust Interest Rate With Credit Card (PDF, DOCX, RTF) and download the specimen onto your device.

- Search for the document you require and examine it.

- Review the file you searched through and preview it or assess the form description to confirm it suits your requirements. If it doesn’t, utilize the search feature to find the correct one. Click Buy Now once you have located the template you need.

- Register and Log In.

- Choose the pricing plan that caters to your needs and set up an account. Use PayPal or a credit card for quick payment. If you already possess an account, Log In and verify your subscription to continue.

- Acquire the editable template.

Form popularity

FAQ

If you're unhappy with your credit card's interest rate, also known as an APR, securing a lower one may be as simple as asking your credit card issuer. It may decline your request, but it doesn't hurt to ask.

Your credit card company must send you a notice 45 days before they can increase your interest rate; change certain fees (such as annual fees, cash advance fees, and late fees) that ap- ply to your account; or make other significant changes to the terms of your card.

Your card issuer generally must give you 45 days of advanced notice before it raises your credit card interest rate for new purchases you make with that card. Card companies are generally restricted from raising the interest rate for your existing balance, but there are certain exceptions.

Before calling up your credit card company and starting a negotiation, we recommend some advance preparation. Figure out your credit score. ... Compare competing offers. ... Call your card provider. ... Don't settle if your request is denied. ... Ask for a different benefit. ... Request a temporary rate reduction.

1. Pay Your Bill in Full Every Month. Most credit cards offer a grace period, which lasts at least 21 days starting from your monthly statement date. During this time, you can pay your full balance without incurring interest on your purchases.