Escrow Instructions in Short Form

Understanding this form

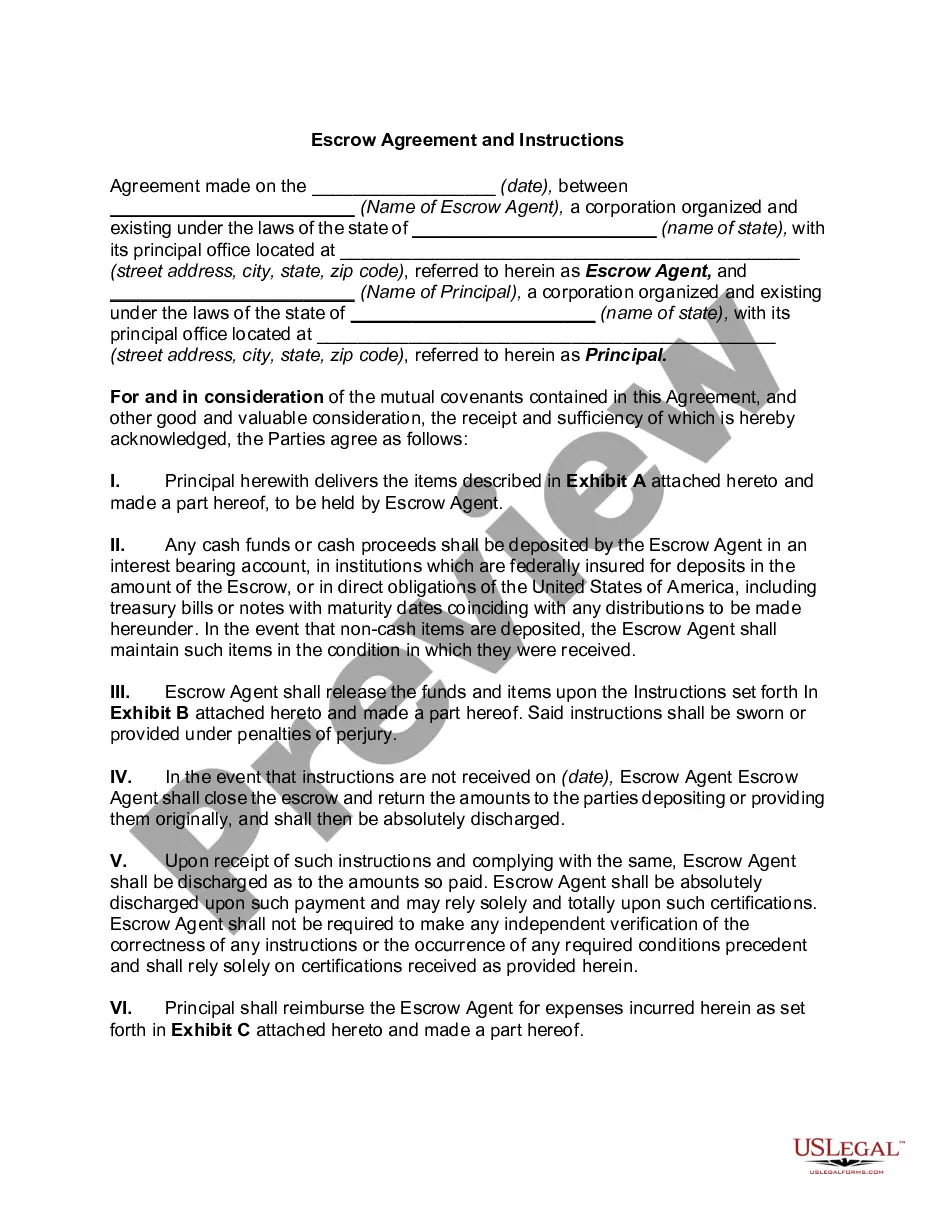

The Escrow Instructions in Short Form is a legal document that outlines the responsibilities and tasks assigned to an escrow agent in a real estate transaction. This form serves as a guide for the escrow agent, detailing the specific duties they must carry out on behalf of the buyer and seller. Unlike other complex escrow agreements, this short form provides a simplified structure, making it easier for users to customize it according to their unique circumstances.

Key parts of this document

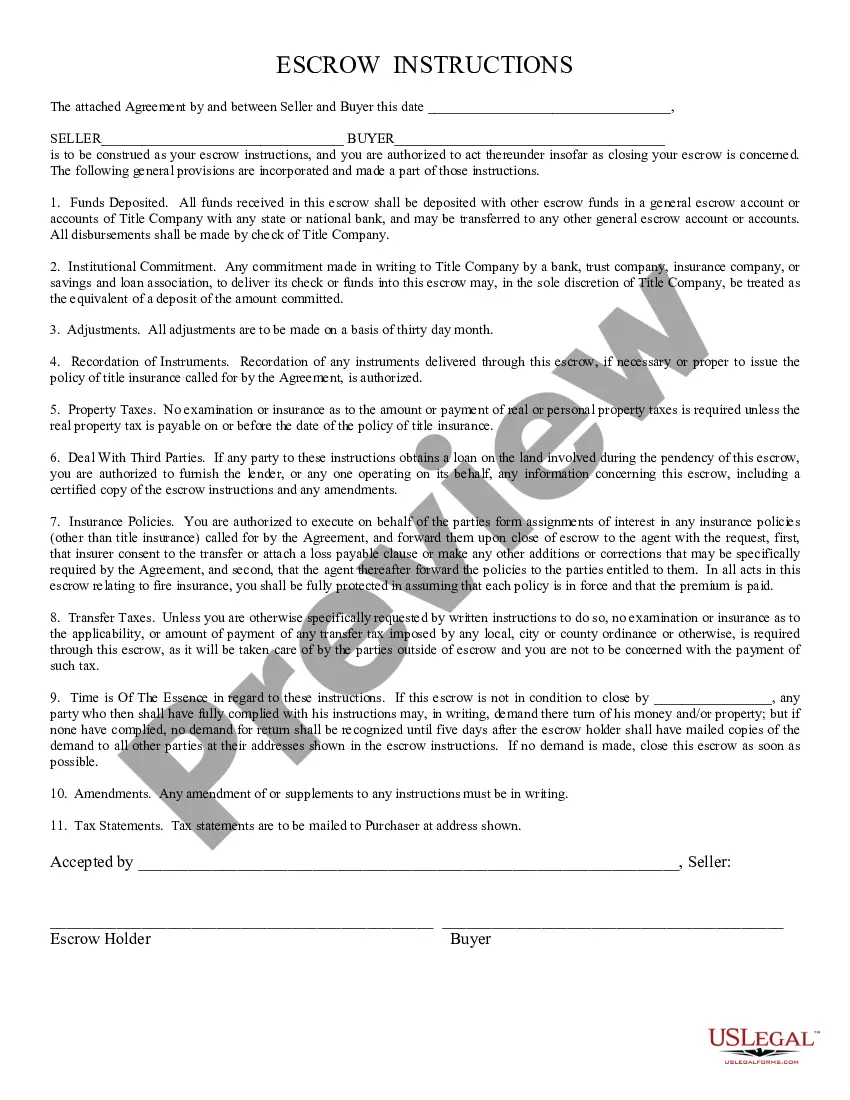

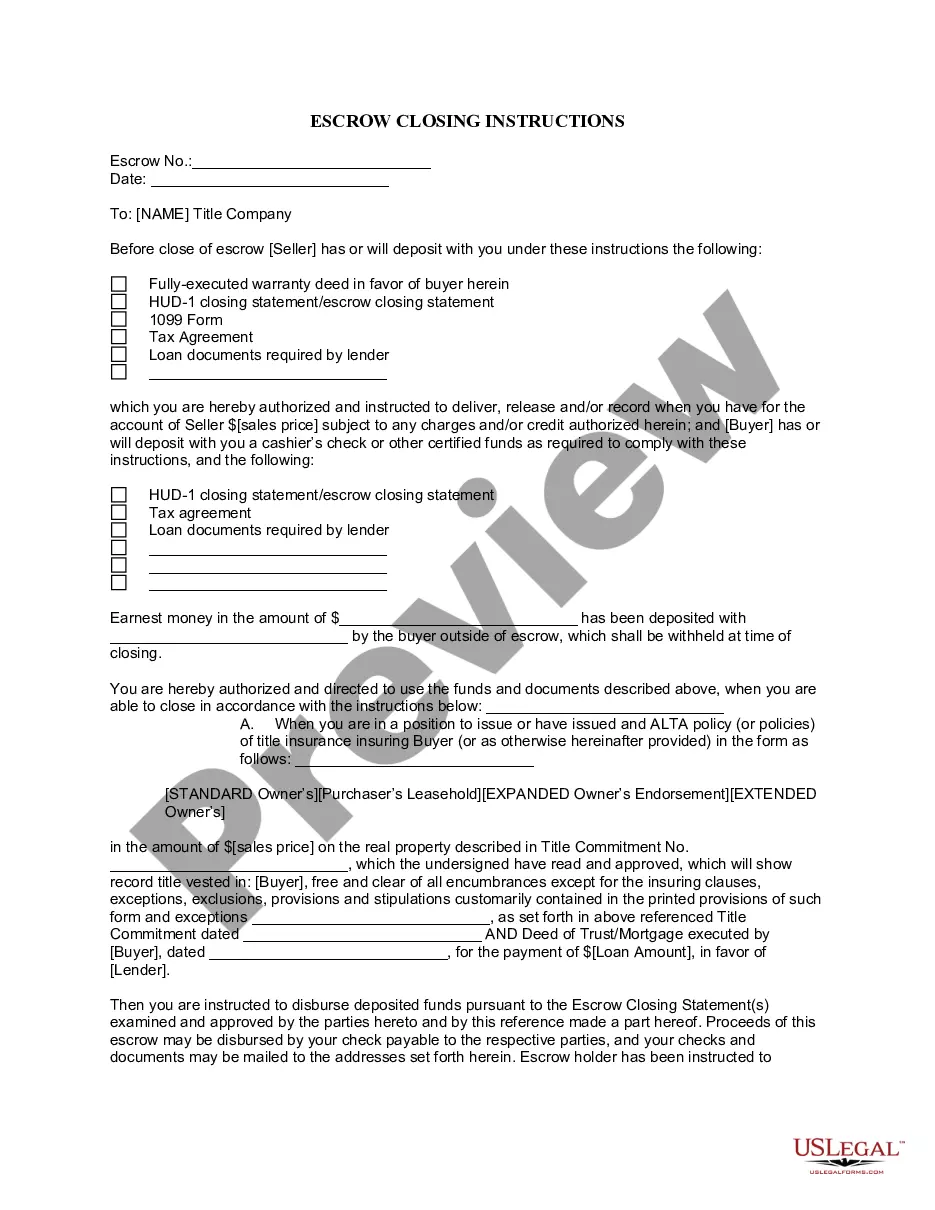

- Date and contact information of the escrow holder and officers.

- Details regarding the purchase price and deposit amounts.

- Provisions for title transfer and title insurance requirements.

- Instructions for handling closing costs and tax prorations.

- Commission fees for listing and selling brokers.

- Specific closing dates and additional instructions.

Situations where this form applies

This form is used during real estate transactions where parties require an escrow agent to manage the distribution of funds and title documents. It is particularly useful when multiple financing sources are involved, such as loans and cash deposits. If you are buying or selling property and need to establish clear guidelines for escrow management, this form is an appropriate choice.

Who should use this form

- Real estate buyers and sellers involved in a property transaction.

- Real estate agents and brokers handling transactions.

- Escrow agents who need clear instructions for their responsibilities.

- Individuals who want a straightforward escrow agreement without legal jargon.

How to complete this form

- Fill in the date and contact information for the escrow holder and officer.

- Specify the details of the property transaction, including purchase price and deposit amounts.

- Enter the title information and any additional fees associated with the sale.

- Outline the responsibilities regarding closing costs and any prorations.

- Review and sign the document, ensuring all parties agree to the terms outlined.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, always check state requirements to ensure compliance with any specific notarization mandates.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Leaving out important details such as lender information or property descriptions.

- Not specifying how closing costs will be divided between parties.

- Failing to confirm the contact details of all involved parties.

- Ignoring state-specific regulations that may apply to escrow instructions.

Why complete this form online

- Convenience of downloading and customizing the form at your own pace.

- Editability allows for easy adjustments to meet particular transaction needs.

- Access to professionally drafted templates, ensuring legal reliability.

Legal use & context

- This form outlines the obligations of the escrow agent, fostering trust between buyers and sellers in real estate transactions.

- It helps to avoid misunderstandings regarding the management and distribution of funds and documents.

- Ensure that all parties understand their rights and responsibilities in relation to the escrow process.

What to keep in mind

- The Escrow Instructions in Short Form streamlines the process of managing an escrow agreement.

- Proper completion of the form helps ensure a smooth real estate transaction.

- Customizing the form as per individual needs and local regulations is crucial for its effectiveness.

Looking for another form?

Form popularity

FAQ

If your escrow account's balance is negative at the time of the escrow analysis, the lender may have used its own funds to cover your property tax or insurance payments. In such cases, the account has a deficiency. If the amount exceeds one month's escrow payment, the lender may give you two to 12 months to repay it.

Generally, an escrow account is a prerequisite if you're not putting at least 20% down on a home. So unless you're bringing a sizable chunk of cash to the closing table, escrow may be unavoidable. FHA loans, for example, always require buyers to set up escrow accounts.

PayPal does not work this way; they do not hold funds in escrow.Once the item has been shipped, it's too latethe scammer will get an item that they never paid for, and the seller will eventually realize that PayPal was never holding money for them.

PayPal does not work this way; they do not hold funds in escrow. The scammer is hoping that the seller will rush to ship the item and send over a tracking number in order to receive the money.

There are some advantages to going without an escrow service your money can earn you interest and you may be eligible for early payment discounts for some bills. But, the disadvantages are obvious you are required to pay your tax bills and insurance payments on time or risk losing your house.

Escrow is the use of a third party, which holds an asset or funds before they are transferred from one party to another. The third-party holds the funds until both parties have fulfilled their contractual requirements.

The major advantage of a mortgage escrow is that the lender assumes responsibility for paying your property taxes and homeowners insurance. This is also the major disadvantage. In addition, with an escrow the lender gets to keep the interest on your account.

Escrow is when a neutral third party holds on to funds during a transaction. In real estate, it's used as a way to protect both the buyer and seller during the home purchasing process.

Your mortgage lender or servicer is allowed to collect the amount of your homeowners insurance and property tax payments, plus a cushion, month in and month out, in escrow. While it's nice to not have to think about making these payments, this pro can be a con for savers who may be able to put the funds to better use.