Irrevocable Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

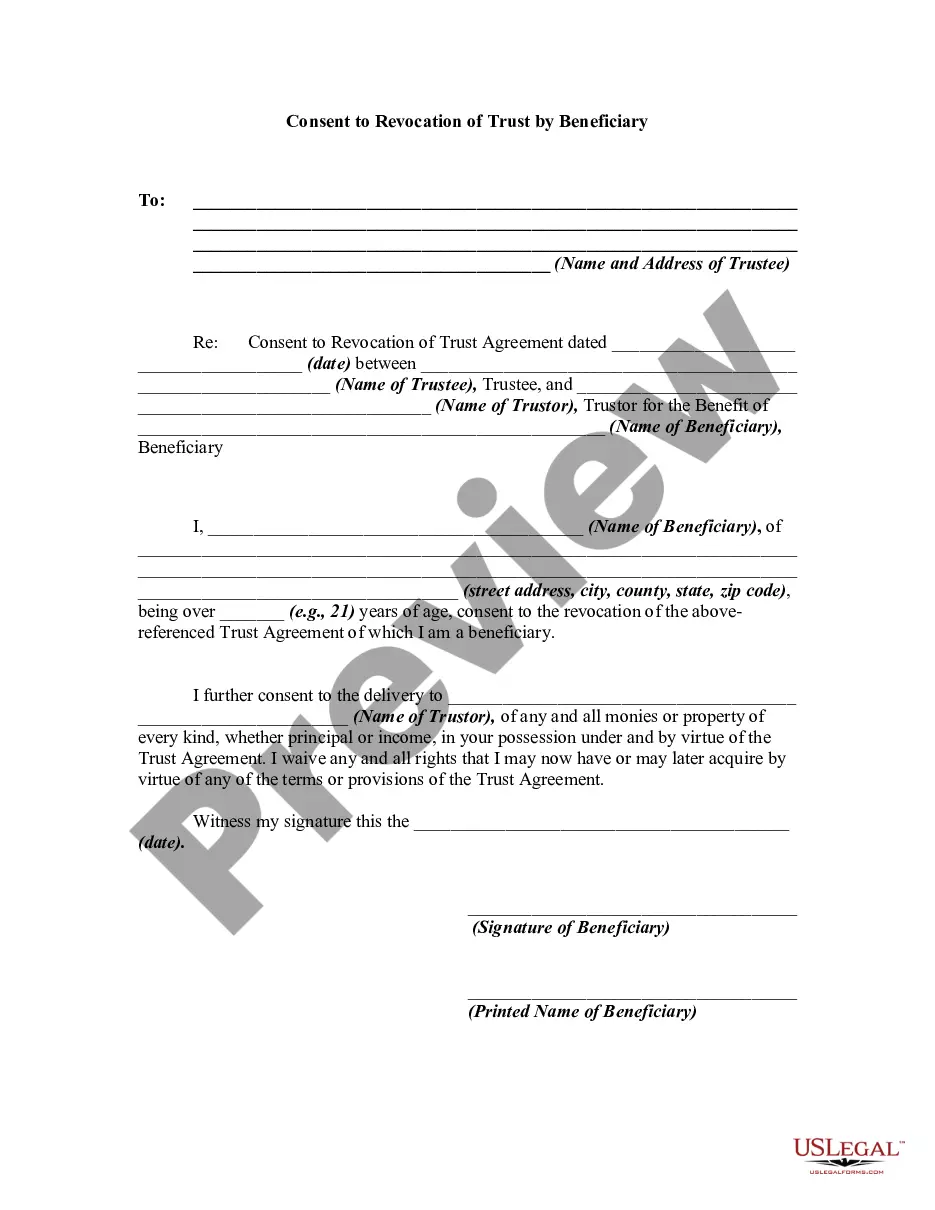

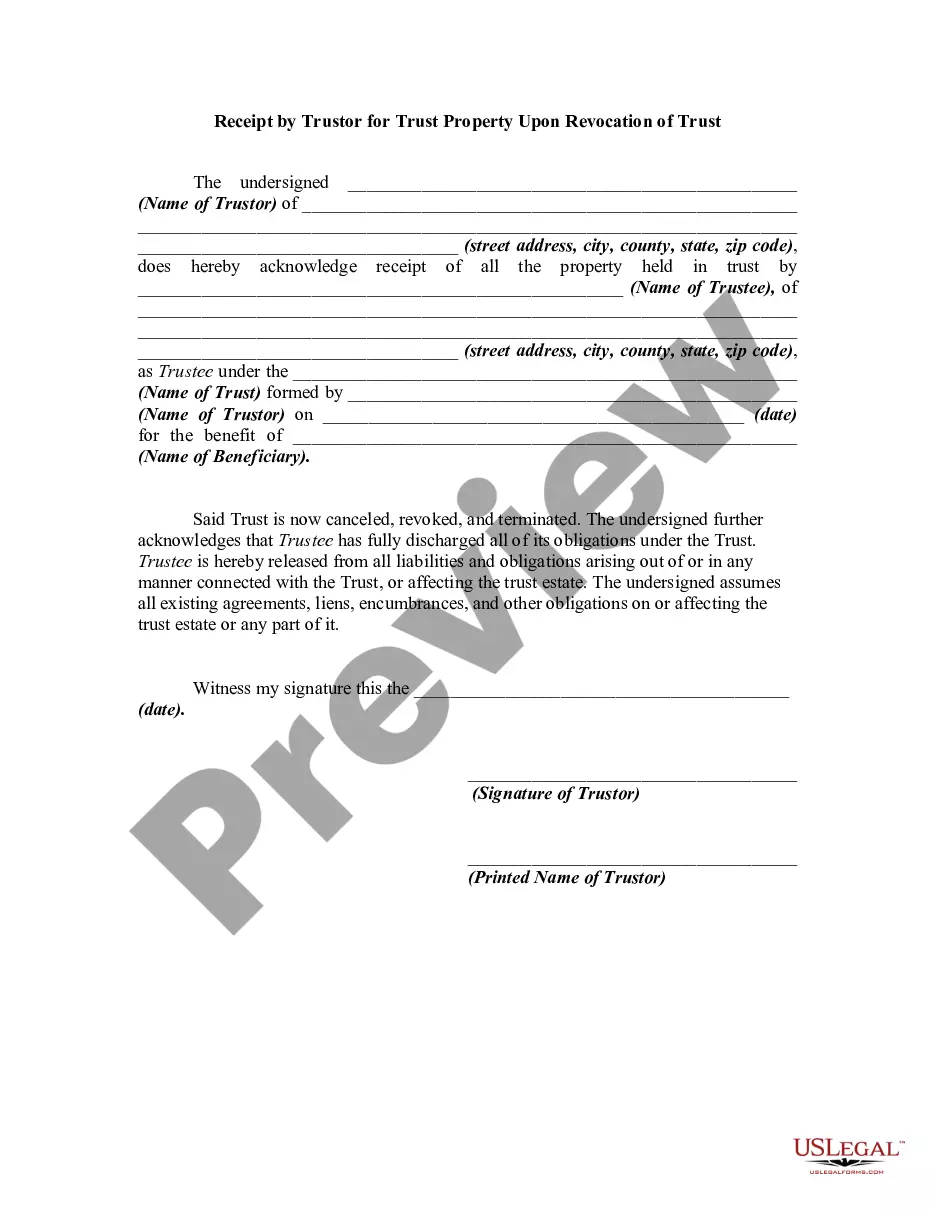

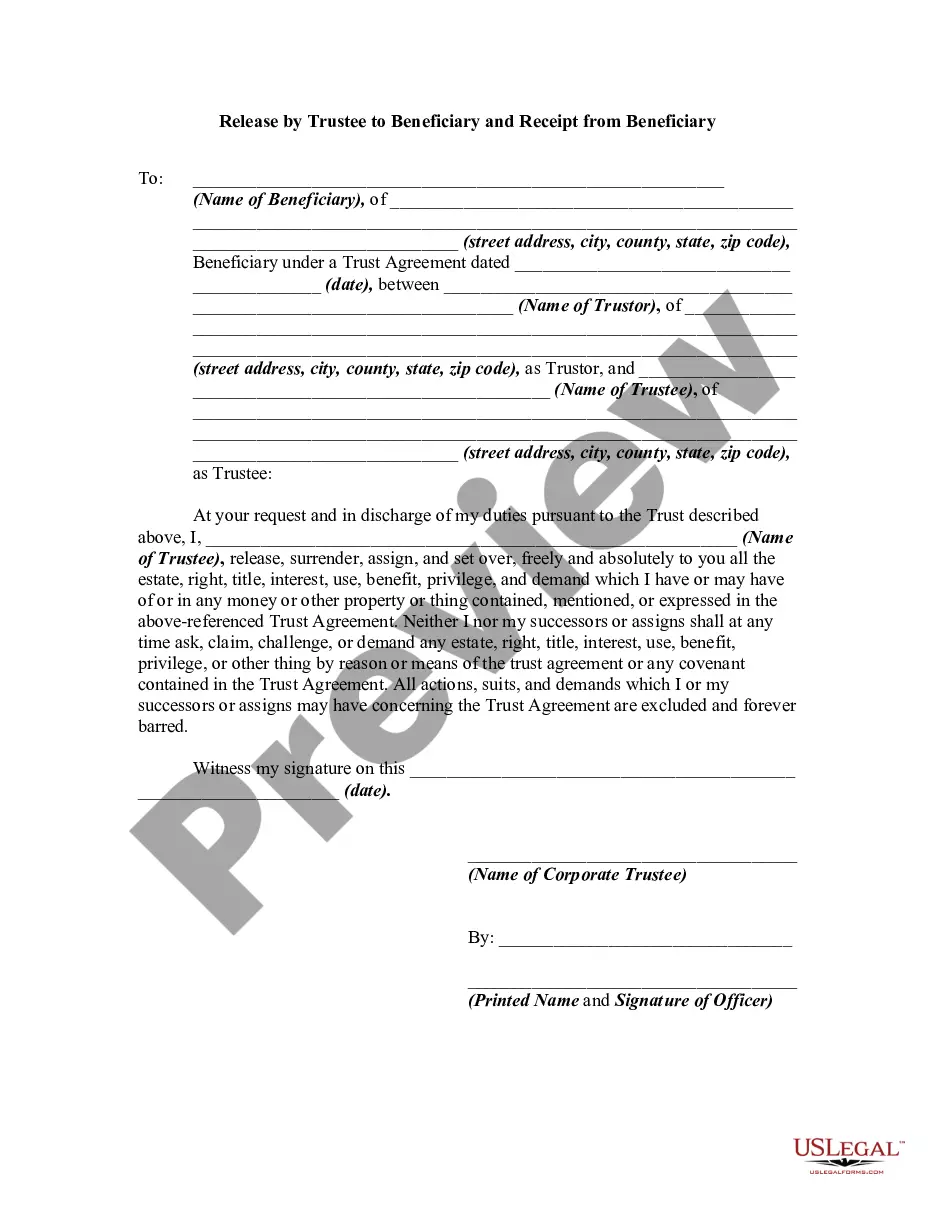

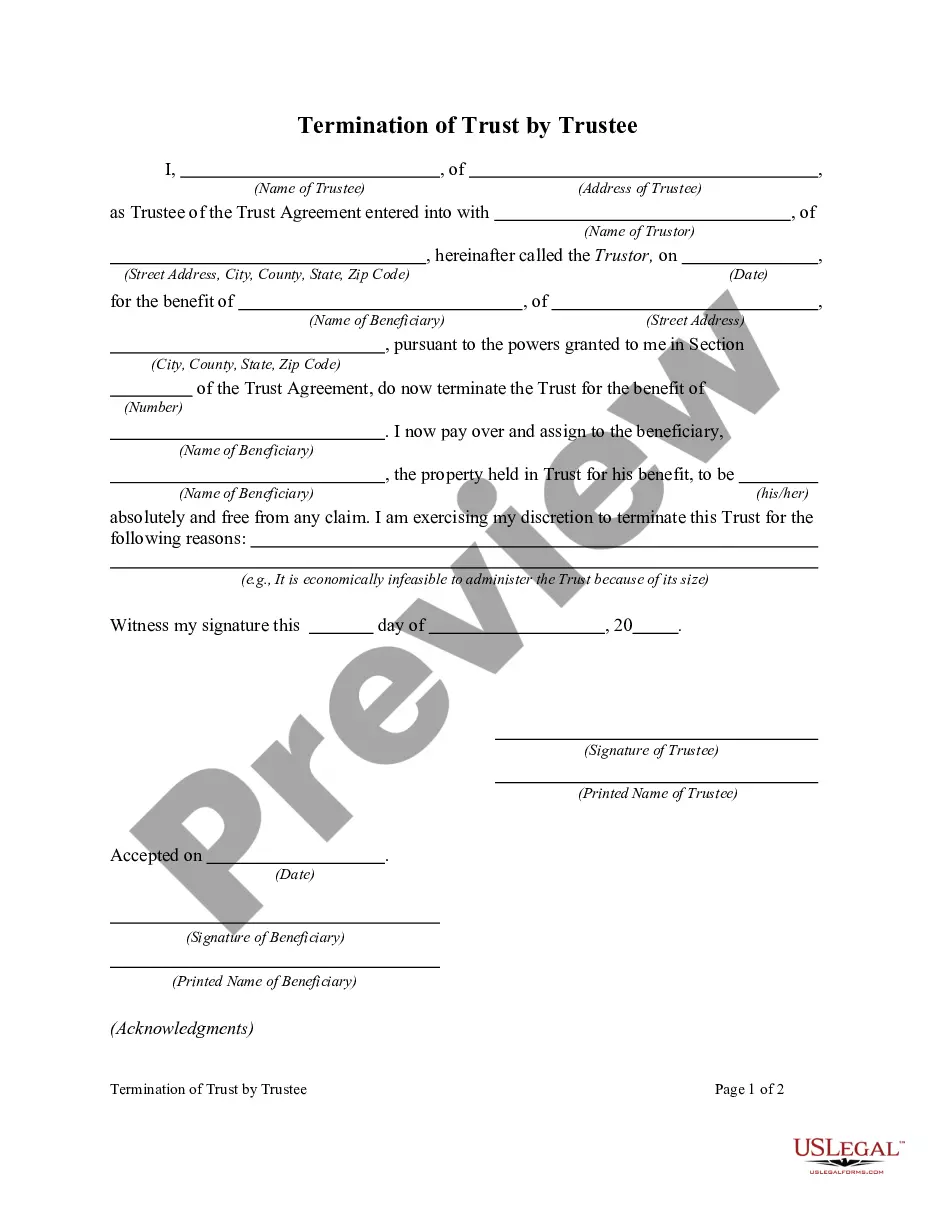

How to fill out Termination Of Trust By Trustee And Acknowledgment Of Receipt Of Trust Funds By Beneficiary?

- Start by logging into your account if you are a returning user. Ensure that your subscription is up to date by checking your account status.

- If you're new to US Legal Forms, review the relevant form descriptions and previews to find the irrevocable trust template that matches your requirements.

- If the template doesn't meet your needs, use the search function to find alternative forms that are compliant with your local jurisdiction.

- Once you select a suitable document, click the 'Buy Now' button and choose a subscription plan that fits your needs. You will need to create an account to access the library.

- Complete the payment process by entering your credit card information or using PayPal to secure your subscription.

- Finally, download the irrevocable trust form to your device, and access it anytime from the 'My documents' section in your account.

Creating an irrevocable trust has never been easier with US Legal Forms. Their extensive library and supportive resources allow you to ensure your legal documents are accurate and compliant.

Don't wait any longer—start your estate planning today with US Legal Forms, and gain peace of mind knowing your assets are secured.

Form popularity

FAQ

Recent changes in tax laws have introduced updated rules regarding irrevocable trusts, primarily addressing how income and distributions are treated for tax purposes. These changes can impact estate planning strategies significantly. Staying informed about these updates is vital, and resources like USLegalForms can provide the latest guidance on managing an irrevocable trust effectively.

While an irrevocable trust itself typically does not need to be filed, any income generated may require tax filings. Therefore, it is essential to keep accurate financial records and comply with tax regulations. Using resources from platforms like USLegalForms can streamline this process and ensure legal adherence.

The IRS has specific guidelines concerning irrevocable trusts, primarily focusing on taxation and asset protection. Generally, any income generated by the trust is taxed at the trust’s tax rate, which is often higher than individual rates. It's crucial to understand these rules to properly manage tax obligations for irrevocable trusts.

In many scenarios, an irrevocable trust does not need to be filed with the court. However, state laws vary, and some jurisdictions require registration. To ensure compliance and take advantage of the benefits, consider consulting a legal professional or using platforms like USLegalForms for assistance.

If an irrevocable trust is not funded, it cannot serve its intended purpose of protecting assets and ensuring their distribution according to your wishes. Essentially, the trust becomes ineffective since it holds no assets. To maximize the benefits of an irrevocable trust, it is crucial to transfer assets into it as soon as possible.

To establish an irrevocable trust, start by consulting with a qualified estate planning attorney who can guide you through the process. This attorney will help you draft the trust document to reflect your wishes and create a strategy tailored to your needs. After finalizing the trust, you will fund it by transferring your chosen assets, ensuring they align with your estate planning objectives.

Choosing not to establish an irrevocable trust can stem from the inability to modify the terms once set. This lack of flexibility can be a drawback for individuals who anticipate changes in life circumstances or financial situations. Furthermore, if you need full control over your assets, you might prefer alternative estate planning solutions that offer greater adaptability.

When considering an irrevocable trust, you should avoid placing certain assets in it, such as retirement accounts and vehicles. Additionally, assets that may require immediate liquidity for expenses or those that could incur high maintenance costs may not be ideal. It's essential to evaluate your situation and consult with a legal expert to ensure the irrevocable trust serves your financial goals effectively.

Filling out an irrevocable trust requires careful attention to detail. Start by identifying the grantor, trustee, and beneficiaries. Next, clearly state the assets to be included in the trust. Platforms like US Legal Forms offer step-by-step guidance, making the process easier and ensuring your trust is filled out correctly.

The biggest mistake parents often make when setting up an irrevocable trust fund is failing to clearly define the terms and conditions. Without precise instructions, beneficiaries may face confusion regarding their benefits. Additionally, overlooking tax implications can lead to unexpected liabilities. Consulting with a legal expert can help prevent these issues.