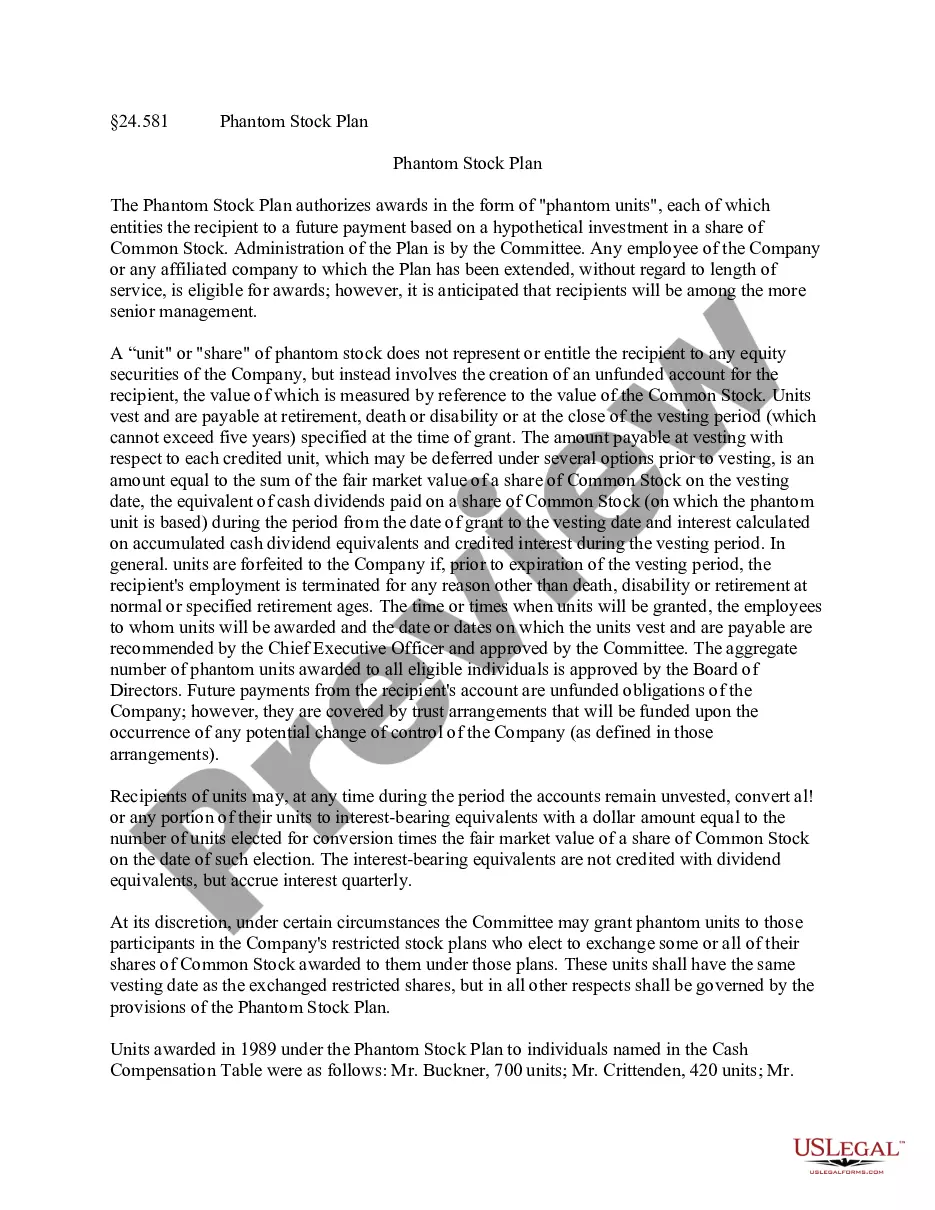

Revocation Trust Trustee For Foreign

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Revocation Of Trust And Acknowledgment Of Receipt Of Notice Of Revocation By Trustee?

Whether for commercial intentions or personal affairs, everyone must confront legal circumstances sooner or later in their lives.

Completing legal paperwork requires meticulous care, starting with selecting the appropriate form template.

- For instance, if you choose an incorrect version of a Revocation Trust Trustee For Foreign, it will be rejected upon submission.

- Thus, it is vital to have a trustworthy source of legal documents like US Legal Forms.

- If you need to acquire a Revocation Trust Trustee For Foreign template, follow these straightforward steps.

- Obtain the sample you require using the search bar or catalog navigation.

- Review the information of the form to ensure it aligns with your situation, state, and county.

- Click on the form's preview to examine it.

- If it is the wrong document, return to the search function to find the Revocation Trust Trustee For Foreign sample you need.

- Download the template when it meets your criteria.

- If you possess a US Legal Forms account, simply click Log in to access previously saved templates in My documents.

- If you do not have an account yet, you can acquire the form by clicking Buy now.

- Choose the appropriate pricing option.

- Complete the account registration form.

- Select your payment method: you can utilize a credit card or PayPal account.

- Choose the document format you prefer and download the Revocation Trust Trustee For Foreign.

- Once downloaded, you can fill out the form using editing software or print it and complete it by hand.

- With a vast US Legal Forms catalog available, you will never need to waste time searching for the suitable sample across the web.

- Utilize the library's user-friendly navigation to find the correct template for any situation.

Form popularity

FAQ

While you can choose a non-citizen trustee, you should look for someone who is, at minimum, a resident of the United States to be your trust's fiduciary. You want to avoid the risk of your trust being classified as a foreign trust for federal or California tax purposes.

The trustee can be an individual, a corporate trustee, or a combination of both. Naming a trusted family member has some advantages, but a corporate trustee has expertise that a family member typically doesn't have.

Interest income earned by the trust is deductible if distributed to a foreign beneficiary but because the beneficiary is a nonresident alien, he will not be subject to U.S. income tax on the distribution. Therefore, the income is not subject to withholding tax (see Rev. Rul.

To pass the control test, your trustee cannot be both a non-citizen and non-resident. If they are, then your trust will likely fail this requirement and be considered foreign for tax and other purposes.

Foreign nongrantor trusts All trusts that are not grantor trusts are considered nongrantor trusts for US purposes. Foreign nongrantor trusts are not generally subject to US tax, unless the trust earns US source or effectively connected income.