Discharge Unsecured Debt

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

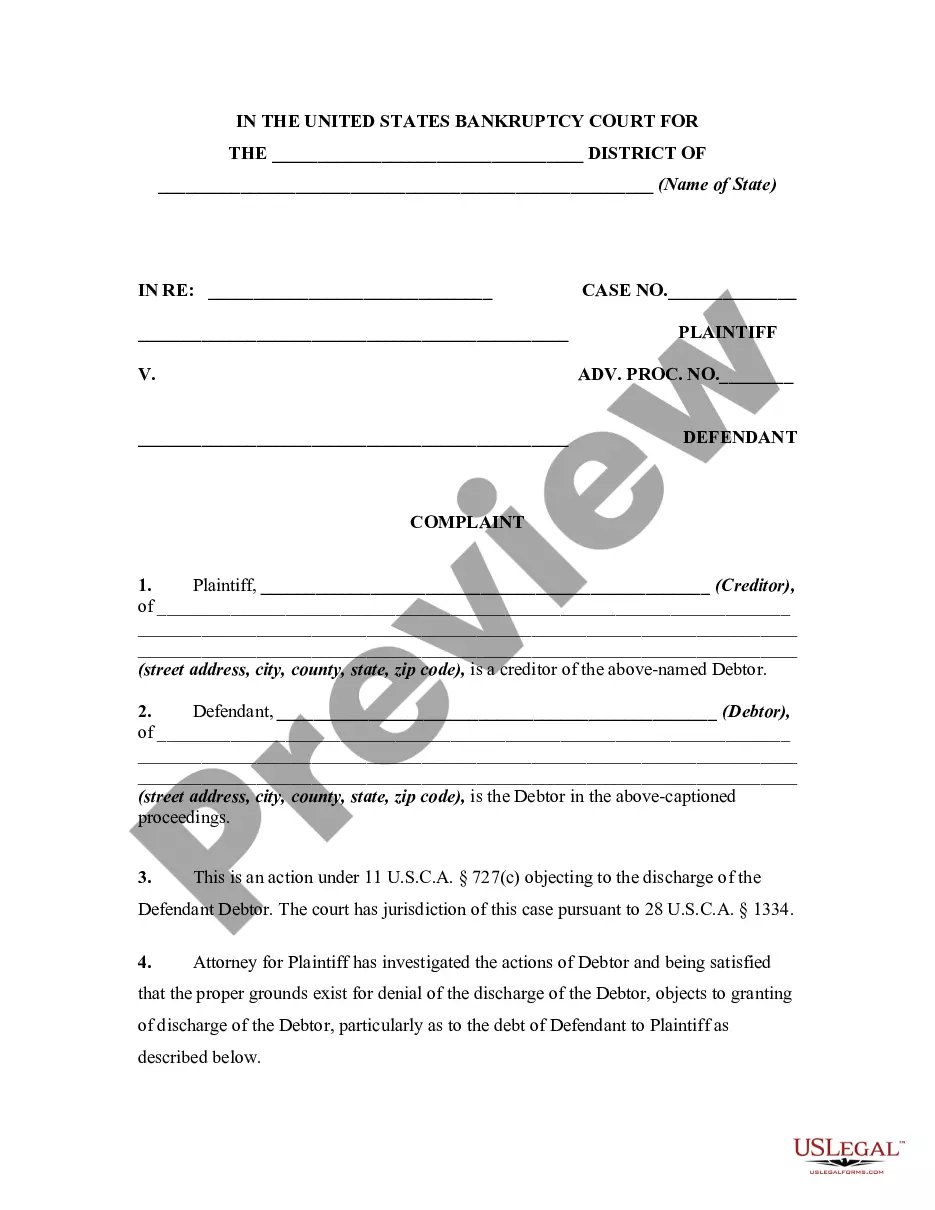

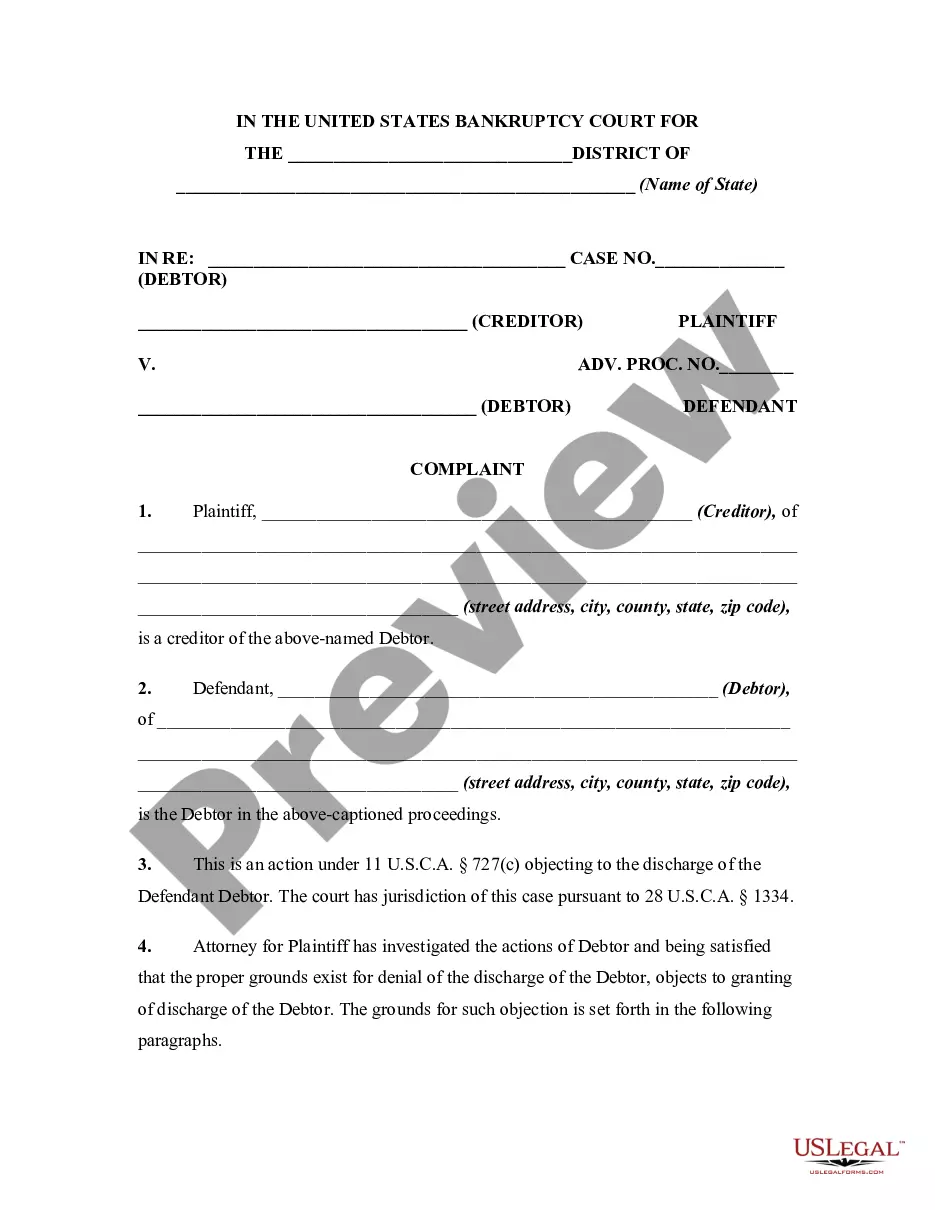

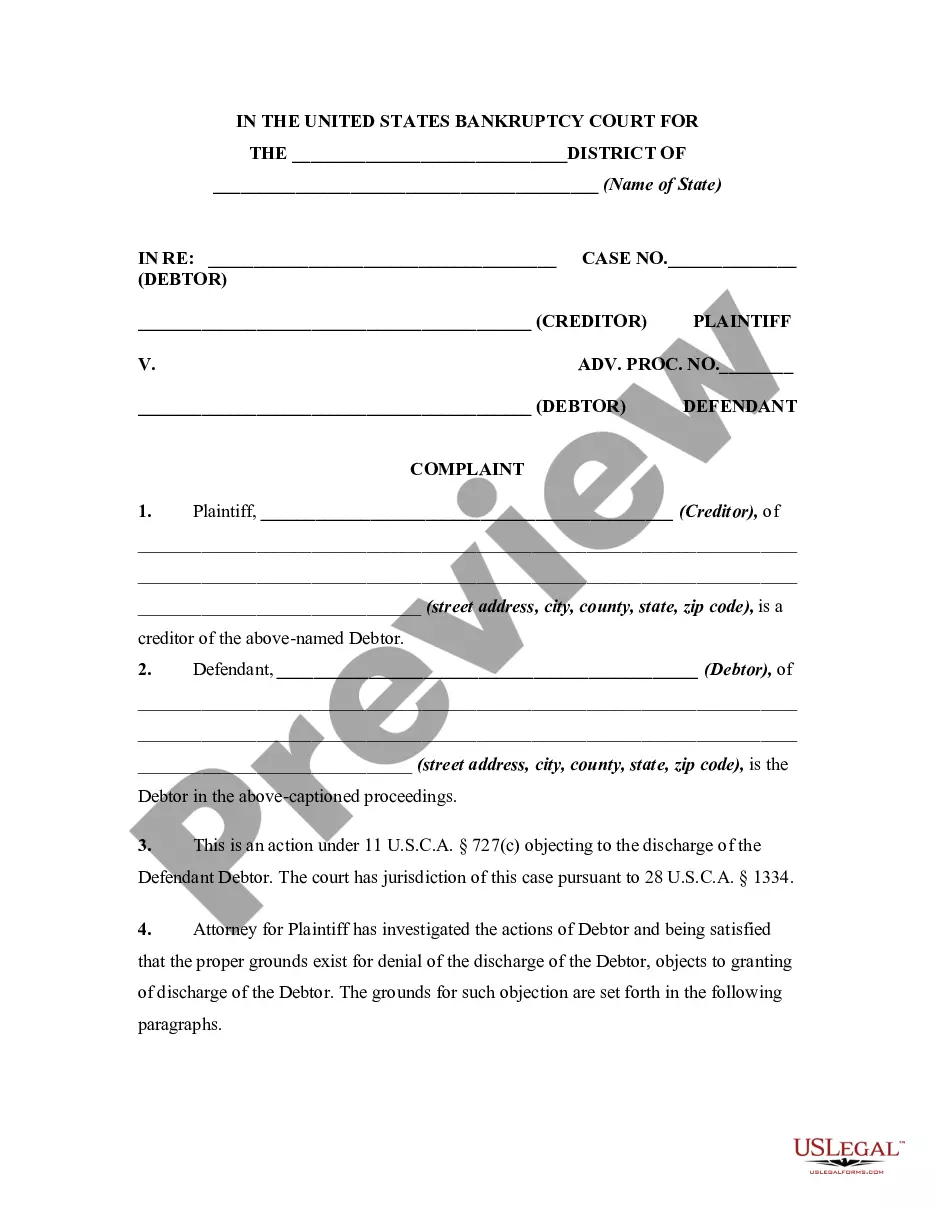

How to fill out Complaint Objecting To Discharge In Bankruptcy Proceedings For Concealment By Debtor And Omitting From Schedules Fraudulently Transferred Property?

- For existing users, log in to your account and locate the necessary form template. Ensure your subscription remains valid and renew if necessary.

- For first-time users, start by checking the Preview mode and form descriptions to confirm you've selected the right document to suit your local jurisdiction requirements.

- If any inconsistencies arise, use the Search tab at the top of the site to find an alternative template that matches your needs.

- Proceed to purchase by clicking the Buy Now button, choosing a subscription plan that best fits your needs. Also, create an account for enhanced access.

- Complete your purchase by entering your payment details via credit card or PayPal to finalize your subscription.

- Download your completed form to your device, ensuring easy access anytime through the My Forms section of your profile.

By leveraging US Legal Forms, you enjoy a robust collection of legal documents, often more extensive than competitors, giving you a significant advantage in achieving your financial goals.

Empower yourself today to discharge unsecured debt and simplify your legal paperwork. Visit US Legal Forms to get started!

Form popularity

FAQ

If your Chapter 13 case is dismissed, any unsecured debt that was part of the bankruptcy process becomes due immediately. This means you will need to resume regular payments to your creditors without any assistance from the bankruptcy court. Thus, understanding what it means to discharge unsecured debt is crucial, as a dismissal can leave you responsible for all debts accrued before filing. Services like uslegalforms can assist you in navigating these complexities.

Certain debts cannot be discharged in Chapter 13 bankruptcy, including some tax debts, student loans, and child support obligations. Secured debts, like mortgage or car loans, also remain intact, as they are tied to specific collateral. It is important to recognize that while you can discharge unsecured debt, other specific debts will continue to require your attention. Consulting uslegalforms can guide you through understanding which debts remain.

In Chapter 13 bankruptcy, unsecured debt is managed through a repayment plan that lasts typically three to five years. During this period, you make monthly payments to a trustee, who then distributes the funds to your creditors. While you may not completely discharge unsecured debt, this plan allows for reduced payments based on your income and living expenses. As a result, you can potentially learn how to discharge unsecured debt more effectively over time.

Certain types of debt cannot be discharged, even through bankruptcy. For example, most student loans, child support, and certain tax debts are typically not eligible for discharge. This means that if you are looking to discharge unsecured debt, you should be aware that these obligations will remain following the bankruptcy process. Understanding these exclusions is vital for effective debt management.

To legally discharge unsecured debt like credit card debt, you can explore several options. One effective method is to file for bankruptcy, which can provide a fresh start by eliminating your eligible debts. Alternatively, you might consider debt negotiation or settlement, where you work with creditors to reduce the amount you owe. Platforms like US Legal Forms offer resources to help you navigate these processes and understand how to discharge unsecured debt effectively.

To remove unsecured debt from your credit report, you first need to settle or discharge the debt. Once resolved, the creditor should update your credit report to reflect this change. Additionally, using services like US Legal Forms can help manage this process, ensuring that your efforts to discharge unsecured debt are documented correctly.

To wipe out unsecured debt, start by evaluating all your outstanding debts, then consider your options. You may file for bankruptcy or negotiate with creditors to settle for less than what you owe. Engaging a reliable service like US Legal Forms can provide guidance and help you discharge unsecured debts successfully.

Wiping out unsecured debt involves several steps, mainly through legal pathways such as bankruptcy or debt negotiation. By filing for Chapter 7 bankruptcy, you can potentially discharge unsecured debts like credit card balances. It's essential to work with professionals who can guide you through the process effectively, including platforms like US Legal Forms that simplify the necessary documentation.

Certain debts cannot be discharged through bankruptcy. Specifically, student loans and most tax obligations cannot be erased. However, understanding how to manage these debts is crucial. You can explore options to handle other types of debt and discharge unsecured debt where applicable.