Refund for Returned Merchandise

What this document covers

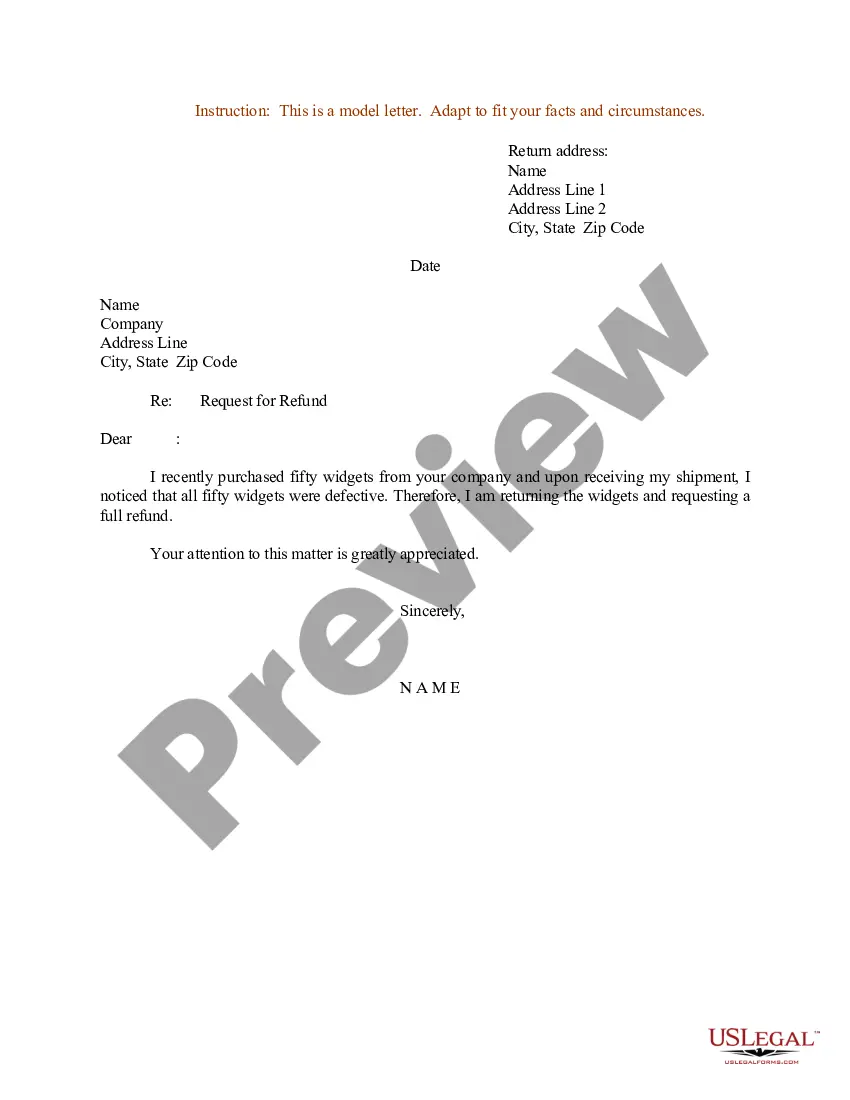

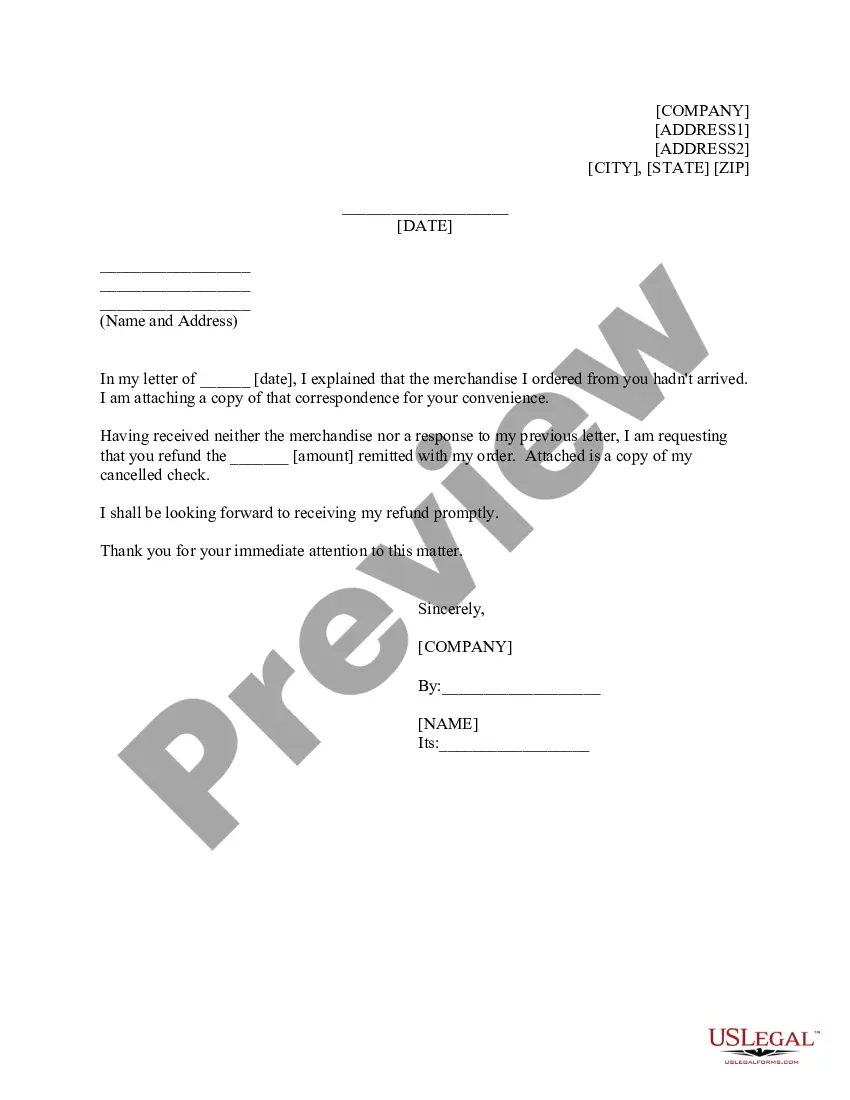

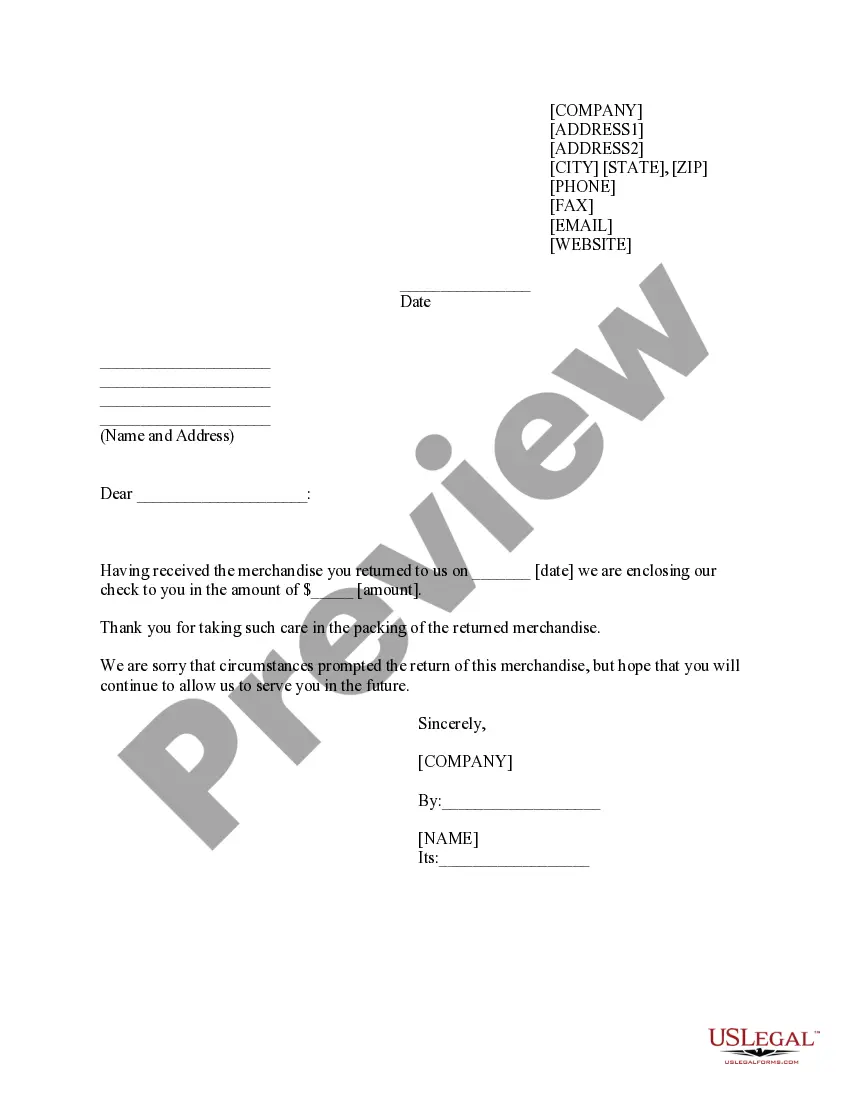

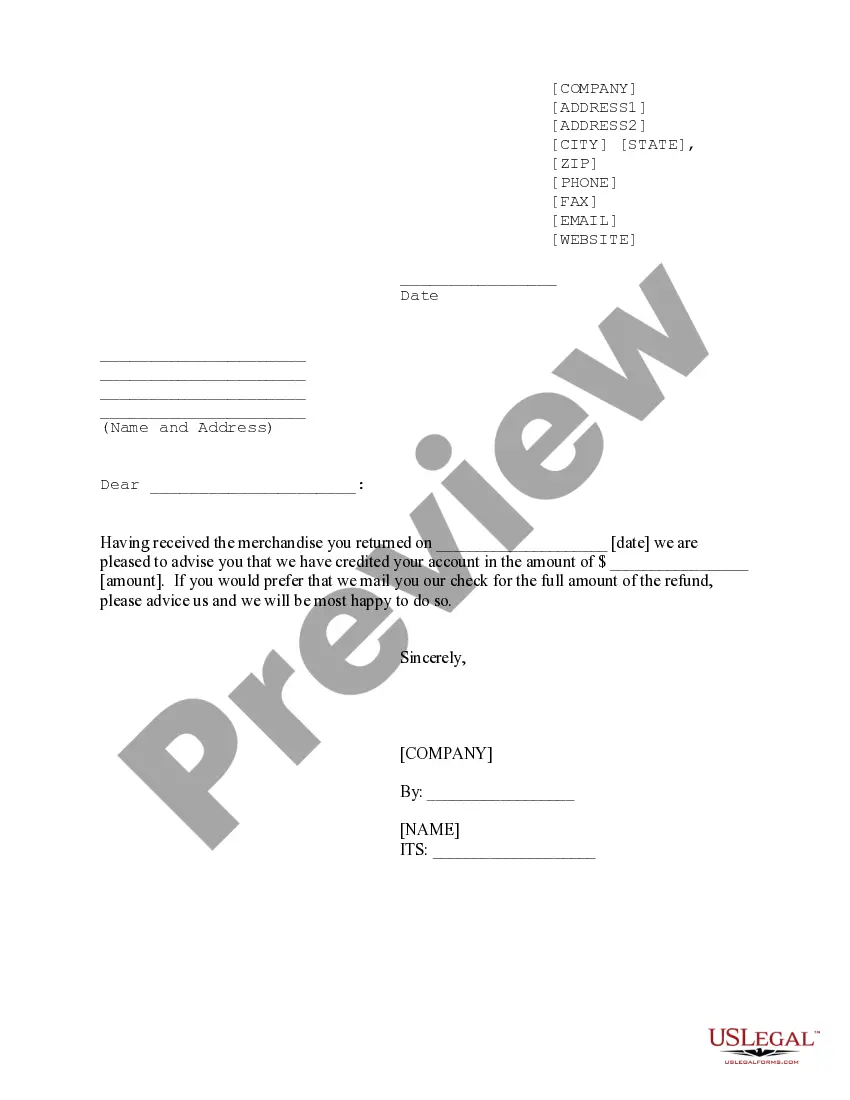

The Refund for Returned Merchandise form is a legal document used by businesses to process refunds for returned items. It serves as confirmation to the customer that their returned product has been received and that a refund is being issued. This form is particularly important for businesses to comply with consumer purchase refund laws that vary by state, ensuring transparency in refund practices.

Key parts of this document

- Date of return

- Customer's name and address

- Amount refunded

- Company representative's printed name and signature

- Title of the person issuing the refund

- Company's name and email address

Situations where this form applies

This form should be used when a customer returns merchandise and is entitled to a refund. It is applicable in situations where the store has a clear refund policy, and the customer meets the conditions specified, such as providing an original receipt or returning the item within a specified time frame. Utilizing this form helps maintain good customer relations and clear communication regarding refund transactions.

Intended users of this form

- Retail businesses that sell merchandise

- E-commerce companies that offer return policies

- Service providers that allow for refunds on products or services

- Any entity that seeks to comply with state consumer refund laws

How to prepare this document

- Enter the date of the refund transaction at the top of the form.

- Fill in the customer's name and their address details.

- Add the amount being refunded to the customer.

- Have a company representative sign the form and provide their printed name and title.

- Include the company's name and a contact email address for any inquiries.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. Ensure to check your state regulations to confirm whether any additional actions are necessary.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to sign the form or provide a printed name.

- Not including the refund amount or incorrectly calculating it.

- Omitting necessary customer information, such as contact details.

- Not providing a clear explanation of return policies related to the refund.

Advantages of online completion

- Convenient access to download and customize the form as needed.

- Editable format that allows businesses to tailor the refund details quickly.

- Reliable legal language drafted by licensed attorneys to ensure compliance.

Legal use & context

- This form provides written proof of the refund transaction.

- It helps protect businesses by documenting the return and refund process.

- Proper use of the form can ensure compliance with state-specific refund laws.

Main things to remember

- The Refund for Returned Merchandise form is essential for processing refunds to customers.

- It must include specific details such as the refund amount, customer information, and signatures.

- Using this form ensures compliance with state laws regarding consumer refunds.

Looking for another form?

Form popularity

FAQ

The Refund for Returned Merchandise form is a business document used to process refunds for items customers return. It confirms the return was received and that a refund is being issued. It is used when a store has a clear refund policy and the customer meets conditions such as presenting the original receipt or returning within the stated time frame, helping to document compliance with state refund rules.

Yes, the form records a refund when a returned item meets the store’s policy and eligibility. It captures the date of return, the amount refunded, the customer’s name and address, and the company representative’s printed name and signature. The actual refund depends on policy, but the document provides formal confirmation that a refund is issued.

A valid reason for a refund depends on the store’s policy and the return conditions, not the form itself. The Refund for Returned Merchandise form does not list reasons; it documents the refund once eligibility is met. It records the date of return, the amount refunded, the customer’s name and address, and the company representative’s details to support state-wide compliance.

The form documents refunds for returns that qualify under a store’s policy; it does not specify exclusions. Whether an item can be refunded depends on the business policy. The form is used to record refunds when eligibility is met and to provide a written record of the date of return, amount refunded, customer and issuer details.

Reasons for a refund are defined by the store’s policy and the terms of the return, not by the form alone. The Refund for Returned Merchandise form does not enumerate reasons; it records the refund transaction after eligibility is confirmed and includes the date of return, amount refunded, customer information, and issuer details to document the payment.

This form targets returned merchandise across multiple states and requires a specific set of fields: date of return, customer name and address, amount refunded, and the company representative’s printed name and signature, plus their title and contact. This focused checklist creates a clear, verifiable record of the refund transaction and aligns with multi-state consumer refund expectations.