Consignment Agreement In Arabic In Nassau

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

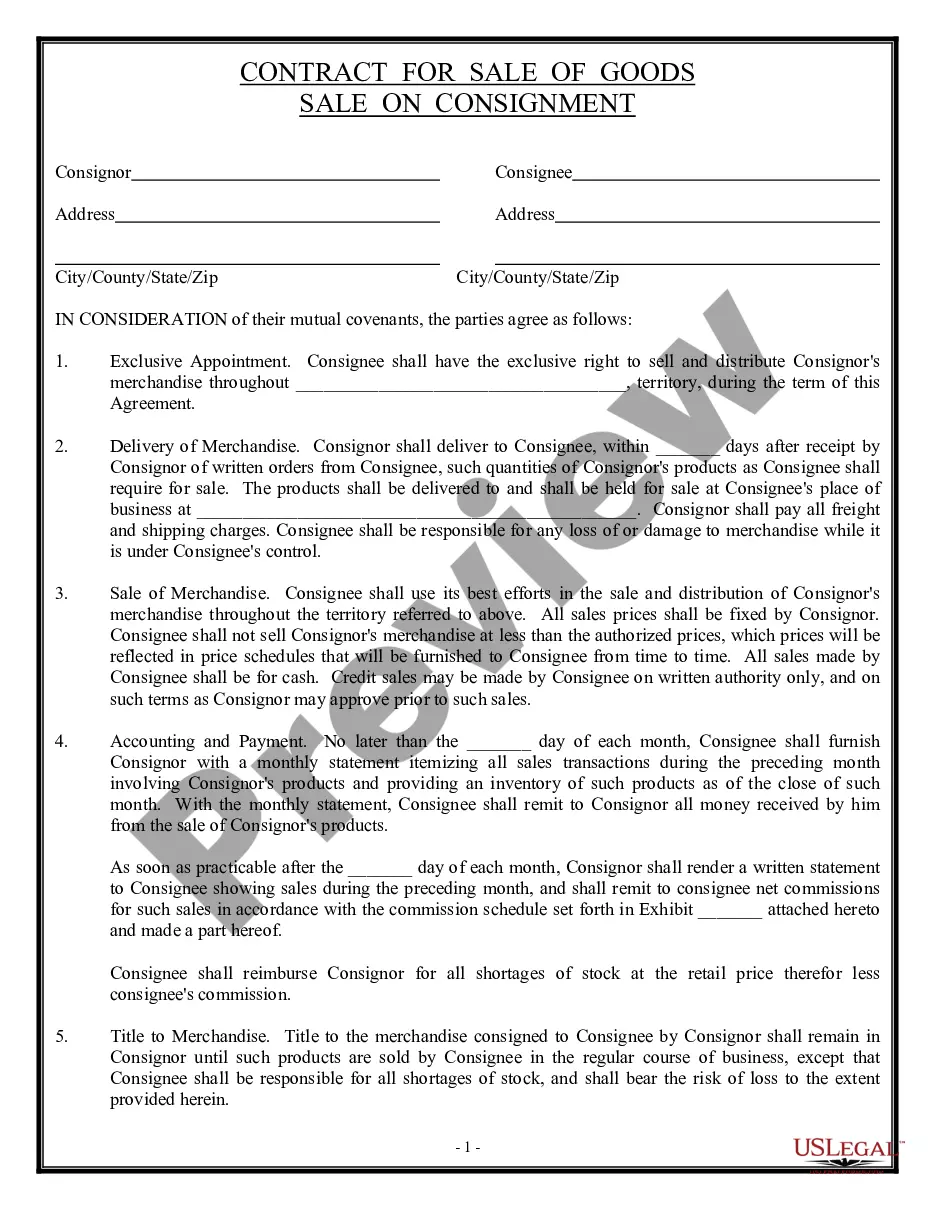

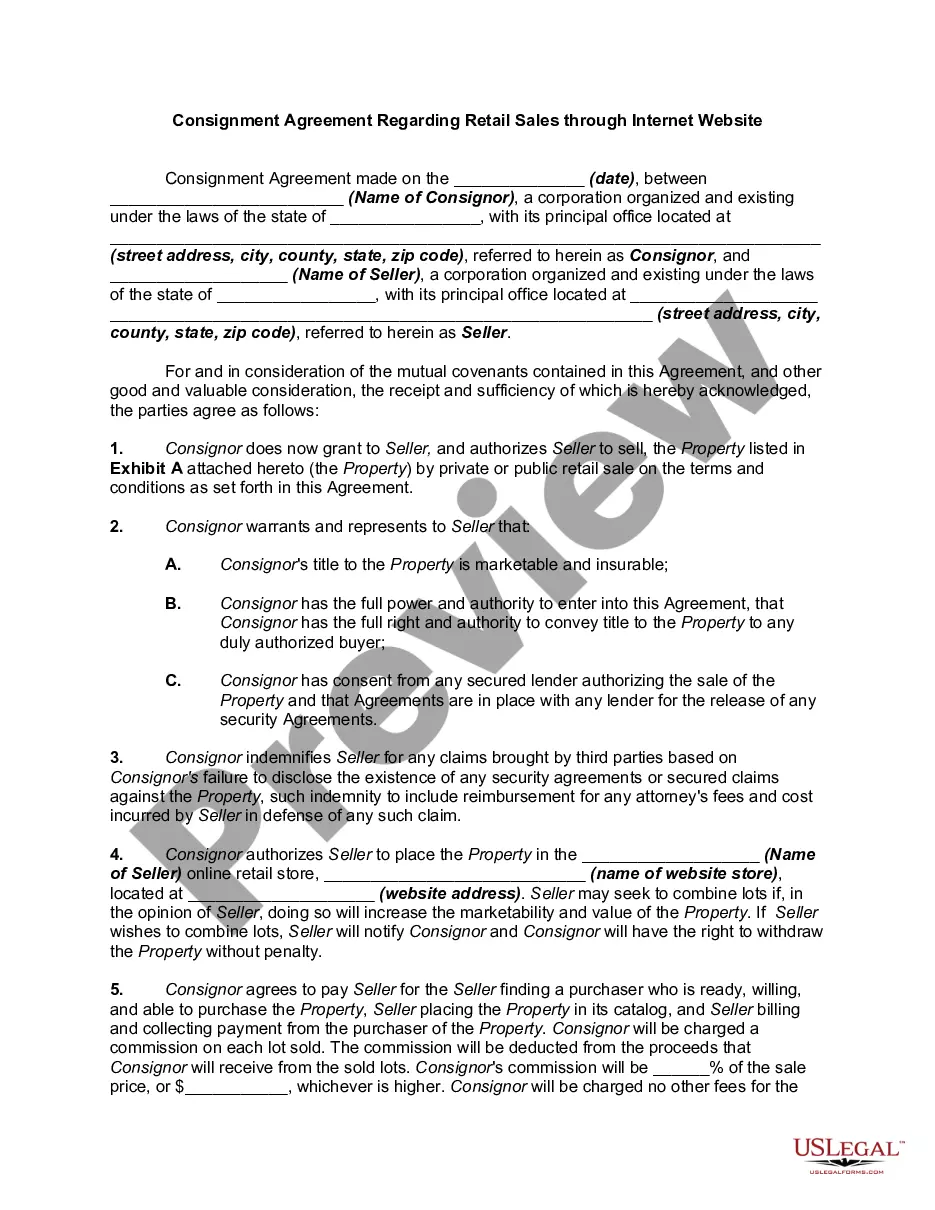

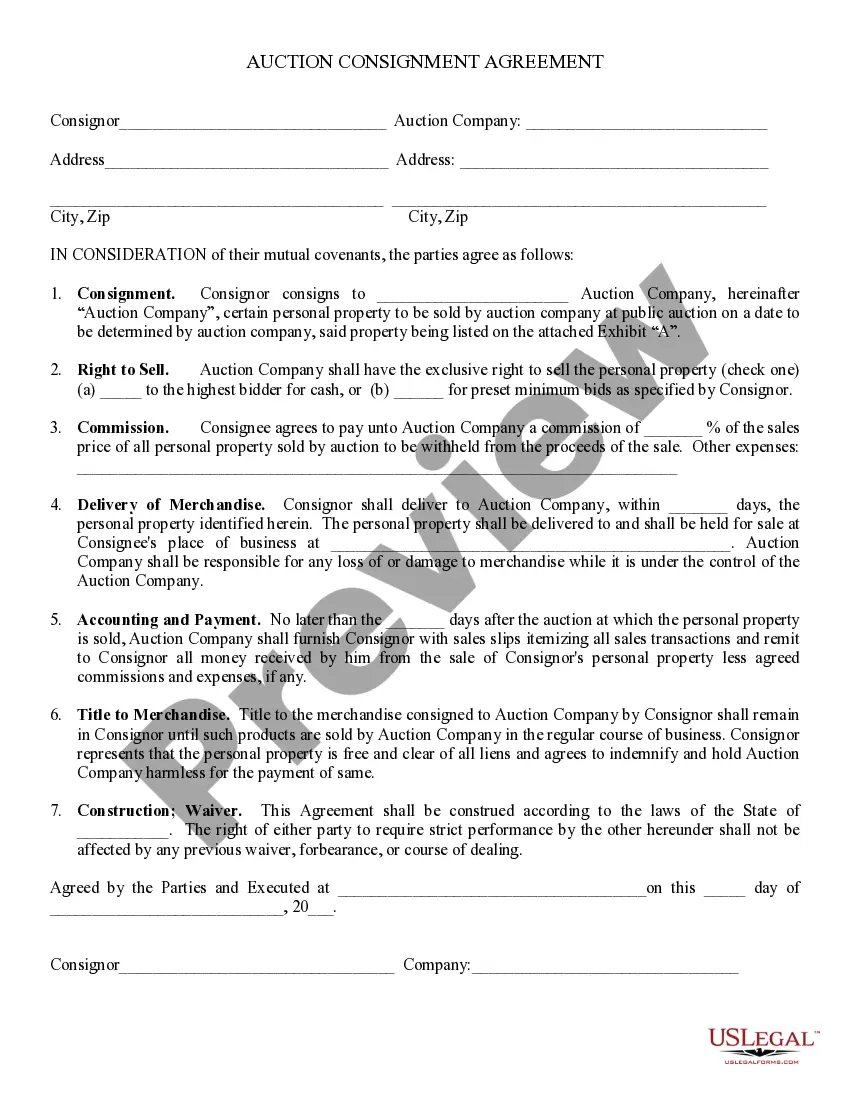

A consignment agreement, to be used where the seller (consignor) wishes to place goods on consignment before they are resold or used by the buyer (consignee). Goods will be stored at a facility or warehouse, under the control of the consignor, the consignee, or a third party.

Consignor records the consignment sales and expenses journal entry. When the consignor receives the Account Sales Report from the consignee, the consignor then completes the consignment accounting. The journal entry accounts for the sales and expenses of the consignment inventory. No entry is made by the consignee.

Generally, though, until substantially all the risks and rewards of ownership of the consignment stock have been transferred to the dealer, the goods are treated as inventories of the manufacturer. There are some entities that have arrangements with a supplier (such as a manufacturer) who supplies goods to a dealer.

Consigned inventory is typically not recorded as an asset on the consignee's balance sheet until it is sold. Instead, it is often disclosed in the financial statements' footnotes or the inventory disclosure section.

The two types of consignment are: Outward Consignment: When goods are sent from one country to another for sale, the consignment is called outward consignment. Inward Consignment: When the goods are sold domestically for sale then it is called inward consignment. X Sent some goods to Y for sale.

The accounting treatment of consignment inventory under IAS-2 ensures accurate recognition and measurement by establishing clear principles for ownership and valuation. Consigned goods remain on the consignor's financial statements until sold, while the consignee records only commission or fees earned.