Form Lis Pendens Foreclosure Nj In Phoenix

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

File a request with the court to remove the lis pendens. Provide the legal reasons the lis pendens is improper, offering proof, for example, that the lis pendens affects real estate that is not connected to the litigation. If the lawsuit is frivolous and merely intended to harass the property owner, offer proof.

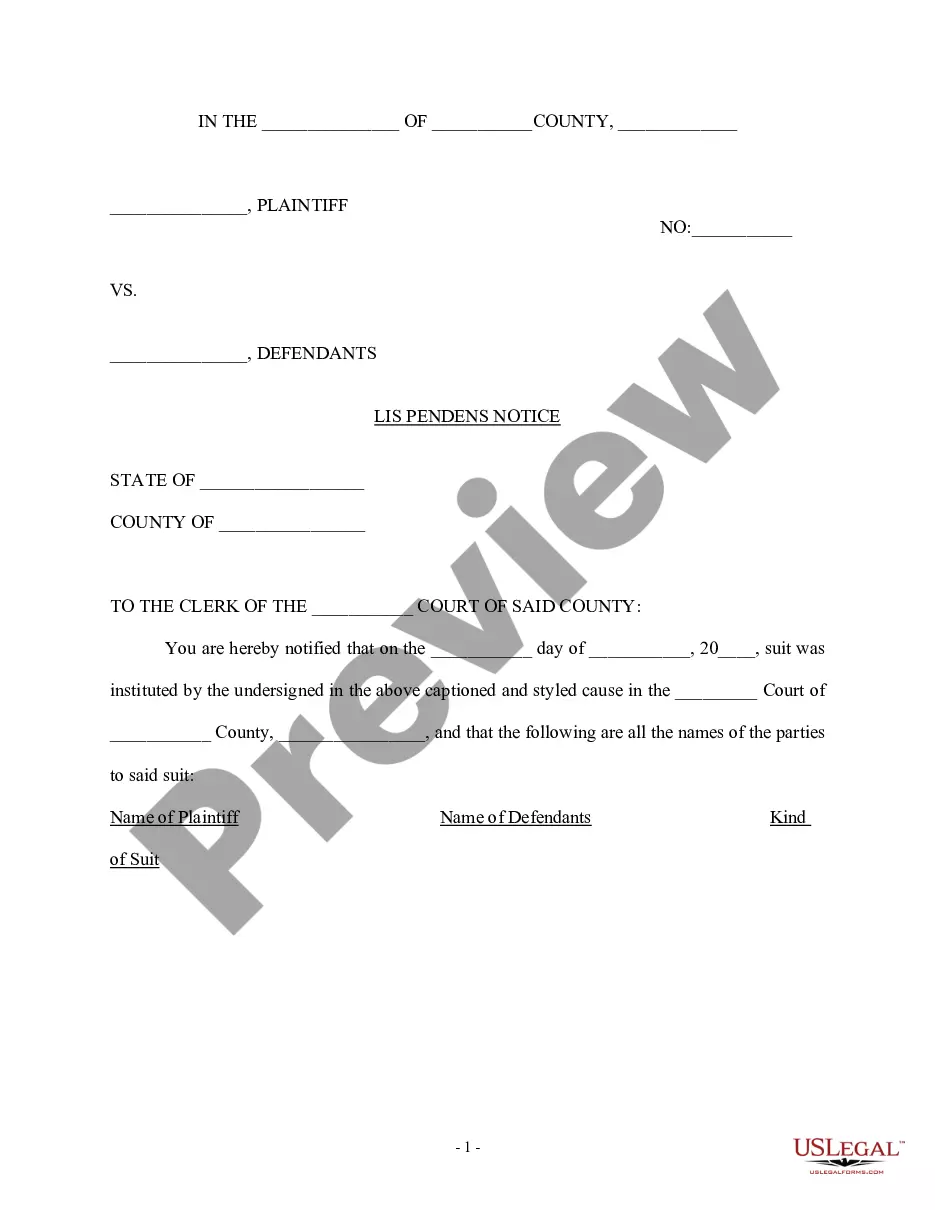

The Lis Pendens is a public notification that the property is being foreclosed upon. If the homeowner attempts to sell the property or get a second mortgage, the title search will reveal the Lis Pendens and notify any interested party that the property's title is in question due to the pending foreclosure.

The Lis Pendens is a public notification that the property is being foreclosed upon. If the homeowner attempts to sell the property or get a second mortgage, the title search will reveal the Lis Pendens and notify any interested party that the property's title is in question due to the pending foreclosure.

Notice of a Nonjudicial Foreclosure To officially start a nonjudicial foreclosure in Arizona, the trustee records a notice of sale in the land records. The sale date can't be any sooner than 91 days after the date the trustee records the notice. (Ariz.

No notice of lis pendens shall be effective after five years from the date of its filing.

The purpose of a notice of lis pendens is to give the public notice that a lawsuit is pending that affects title to real property so as to preserve the plaintiff's right to obtain title if ordered by the Court.

Once the complaint is filed, it enters a Lis pendens, meaning a suit is pending. The lender becomes the plaintiff, and the debtor becomes the defendant in the court record. The case receives a docket number. The plaintiff must serve the defendant with the foreclosure complaint.

No notice of lis pendens shall be effective after five years from the date of its filing.

The Fair Foreclosure Act aims to prevent wrongful foreclosures by requiring lenders to ensure that homeowners are fully informed and given every opportunity to retain their homes.

You can only be foreclosed on after you have not made payments for 120 days. Since payments are generally made every 30 days, this means that your property cannot be foreclosed on until you have missed four mortgage payments.