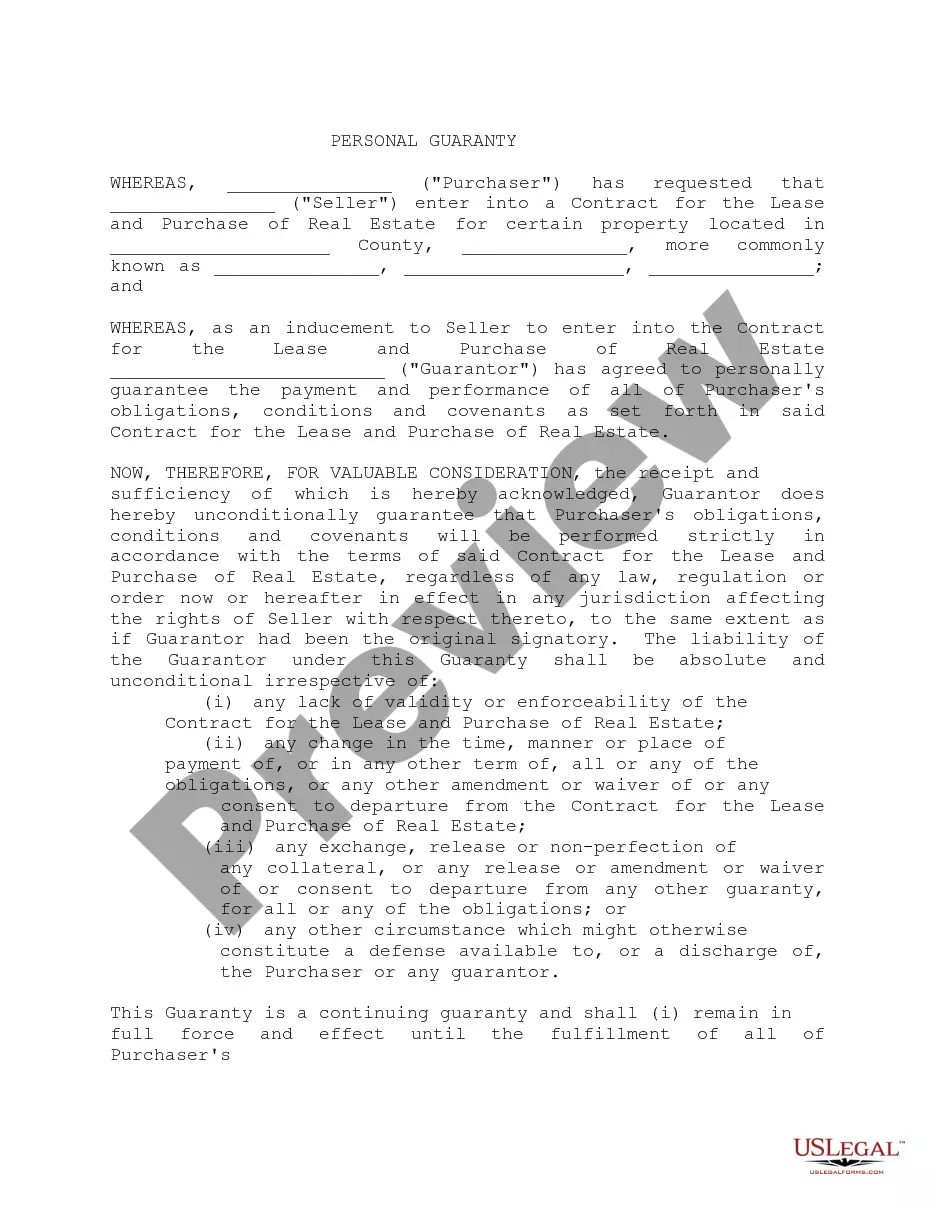

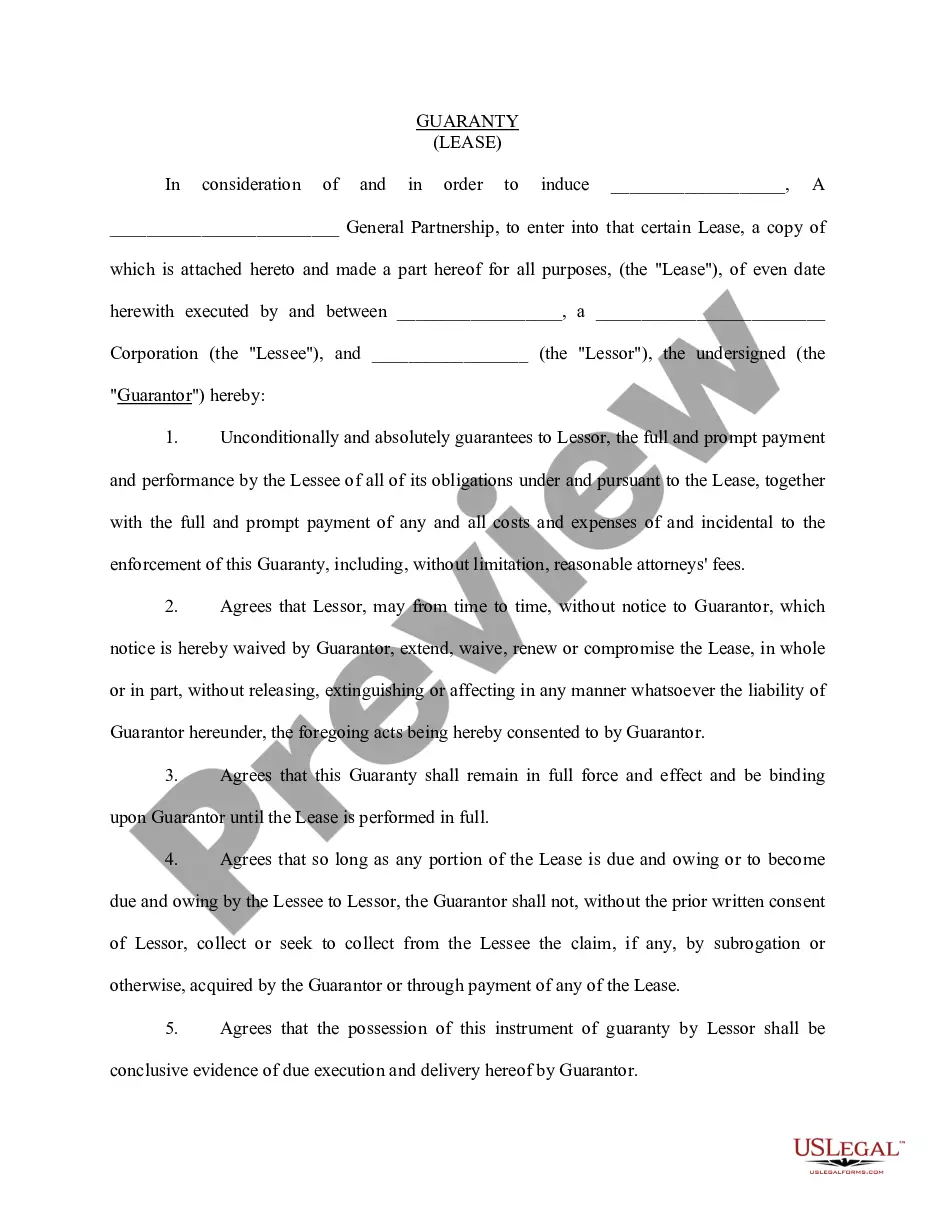

Alabama Cosigner For Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Alabama Guaranty Attachment To Lease For Guarantor Or Cosigner?

How to obtain professional legal documents that comply with your state laws and create the Alabama Cosigner For Mortgage without hiring an attorney.

Numerous online services offer templates for various legal scenarios and formal requirements. However, it can be time-consuming to ascertain which of the available examples meet both your use case and legal standards.

US Legal Forms is a trusted platform that assists you in locating official documents prepared in accordance with the latest updates in state law, helping you save on legal fees.

If you do not have an account with US Legal Forms, follow the instructions below: Check the page you've opened to see if the form meets your requirements. Use the form description and preview options, if applicable. Search for another template in the header specifying your state, if needed. Once you find the relevant document, click the Buy Now button. Choose the most suitable pricing plan, then Log In or register for an account. Select the payment option (by credit card or through PayPal). Pick the file format for your Alabama Cosigner For Mortgage and click Download. The downloaded templates will be saved for your use: you can always access them in the My documents section of your profile. Subscribe to our service and prepare legal documents independently like a seasoned legal professional!

- US Legal Forms is not just a typical online library.

- It consists of over 85k verified templates for diverse business and personal situations.

- All documents are categorized by field and state to streamline your search process.

- It also features powerful tools for PDF editing and electronic signatures, allowing users with a Premium subscription to conveniently complete their forms online.

- Acquiring the necessary documentation requires minimal time and effort.

- If you already possess an account, Log In and confirm your subscription is active.

- Download the Alabama Cosigner For Mortgage by clicking the appropriate button next to the file title.

Form popularity

FAQ

For a cosigner mortgage, lenders typically prefer a credit score of at least 620. However, your mortgage approval also depends on the primary borrower's financial situation. An Alabama cosigner for mortgage with a higher credit score can significantly improve your chances of approval and lower interest rates. Always check with your lender for specific requirements.

Yes, adding another person to an existing mortgage is possible. You will need to involve your lender and often complete a refinancing process or modification to include the new borrower. An Alabama cosigner for mortgage can be a helpful option here, as they can share financial responsibility. Make sure to clarify how this change affects your mortgage terms before proceeding.

Cosigning for an Alabama cosigner for a mortgage can be a tricky decision, especially if you're doing it for a friend. If your friend struggles to make payments, your credit score and financial stability may take a hit. Trust and open communication are essential before entering this kind of agreement. Understanding both parties' financial situations can lead to a more informed decision.

To act as an Alabama cosigner for a mortgage, you typically need to meet certain requirements. Lenders usually ask for a strong credit score, a stable income, and a good debt-to-income ratio. These factors assure lenders that you can support the primary borrower in making payments. Always review the specific requirements with your lender for accurate information.

To protect yourself as an Alabama cosigner for mortgage, maintain open communication with the primary borrower about finances and payments. Consider having a written agreement that outlines responsibilities and expectations. You might also want to monitor payments closely and set reminders for upcoming due dates to avoid late payments. Utilizing services like USLegalForms can help clarify agreements and protect your interests.

To become an Alabama cosigner for mortgage, certain eligibility criteria must be met. Typically, a cosigner should possess good credit, stable income, and a proven financial history. Lenders often require documentation to verify these factors, which helps ensure the borrower can manage the mortgage responsibly. Understanding these requirements can help you prepare effectively.

Generally, an Alabama cosigner for mortgage does not automatically go on the title of the property. The title typically includes only the primary borrower unless both parties agree otherwise. However, some situations allow a cosigner to be added to the title, which should be deliberated before closing. It is essential to consult legal experts or real estate professionals for personalized advice.

Adding someone to your mortgage typically requires a formal process through your lender. In most cases, you cannot add a cosigner simply by signing a document; instead, it may necessitate a refinancing or remortgaging. Consulting with your lender can clarify the specific steps and requirements involved in adding an Alabama cosigner to your mortgage.

To get approved for a cosigner, you need to demonstrate the financial stability of both parties to the lender. The Alabama cosigner should provide their income, credit history, and debt information, which will be evaluated alongside your own. It’s wise to communicate fully with your cosigner about their role in the mortgage process to avoid any surprises along the way.

Finding an Alabama cosigner for a mortgage can be straightforward, depending on your personal connections. Typically, a cosigner needs to have a strong credit history and stable income. If you approach someone you trust, like a family member or close friend, you may secure a cosigner without too much difficulty. Just ensure they understand the responsibilities involved.