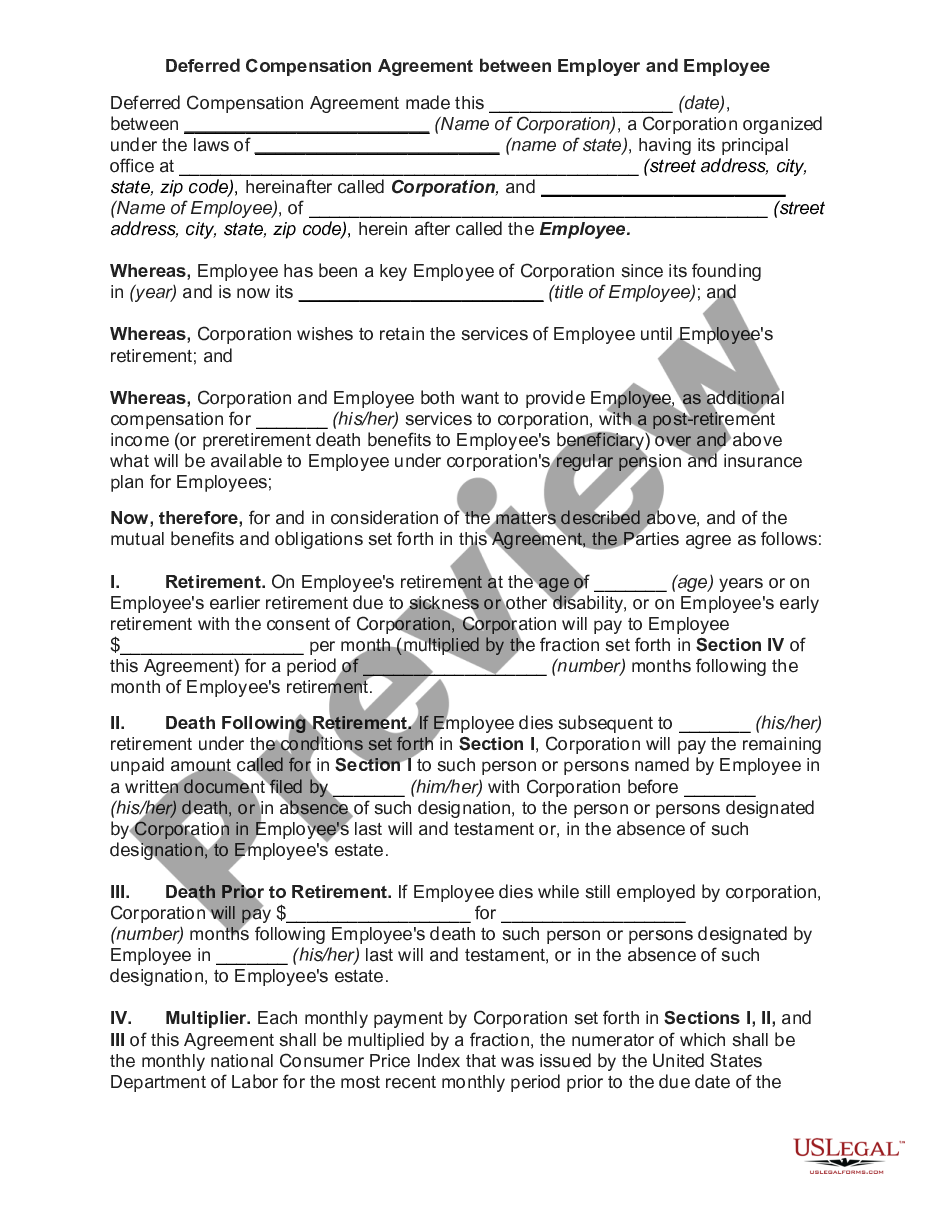

Deferred Compensation Agreement by First Florida Bank, Inc. for Key Employees

About this form

The Deferred Compensation Agreement by First Florida Bank, Inc. for Key Employees is a legal document that allows eligible employees to defer a portion of their Phantom Share Awards under the First Florida Banks, Inc. Book Value Phantom Stock Plan. This agreement helps key employees manage their compensation by postponing income to a future date, potentially allowing for tax advantages. It differs from other forms of compensation agreements as it specifically addresses the deferral of phantom stock awards and provides detailed terms for administration and investment options.

Form components explained

- Effective date of the agreement and conditions of validity.

- Administration guidelines by the Phantom Stock Plan Committee.

- Eligibility criteria for participating employees.

- Details on the timing of the deferral election and available percentage options.

- Conditions for crediting deferred awards and investment options available.

- Guidelines for distribution upon various termination scenarios including retirement and disability.

- Restrictions on the transfer of benefits and continuation provisions for the agreement.

When to use this form

This form should be used when key employees of First Florida Bank, Inc. wish to defer their Phantom Share Awards under the specified plan. This may be particularly relevant during annual performance evaluations or as part of a compensation package that includes phantom stock options. Employees might also utilize this agreement when planning for retirement or seeking to enhance their long-term financial strategies.

Who should use this form

- Key employees of First Florida Bank, Inc. identified for participation in the Book Value Phantom Stock Plan.

- Employees looking to defer a portion of their Phantom Share Awards for tax benefits or long-term investment.

- Human resources and financial managers involved in structuring compensation arrangements for eligible staff.

Completing this form step by step

- Review the agreement thoroughly to understand terms and conditions.

- Identify if you meet the eligibility requirements as a key employee.

- Make an election to defer a percentage of your Phantom Share Awards when such shares are granted.

- Submit your deferral election in writing to the Phantom Stock Plan Committee as instructed within the form.

- Select how you prefer your deferred compensation account to be invested.

- Keep a copy of the signed agreement for your records.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. It is advisable to check applicable regulations to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to submit the deferral election on the day Phantom Shares are granted.

- Not understanding the investment options available for deferred amounts.

- Neglecting to read the terms regarding distribution of deferred funds upon employment termination.

- Confusing the eligibility criteria for participation in the agreement.

Why use this form online

- Convenience of downloading the agreement from anywhere at any time.

- Editability allows you to fill in your details easily before printing.

- Access to a reliable template drafted by licensed attorneys, ensuring you meet legal standards.

- User-friendly format that guides you through each section step-by-step.

- The agreement is a legally binding document that outlines the terms of deferred compensation.

- It provides guidelines on the rights and obligations of both the employee and the employer.

- It's essential to follow the terms closely to ensure enforceability and compliance with tax regulations.

Quick recap

- The Deferred Compensation Agreement allows for tax deferrals on certain compensation.

- Employees must elect to defer at the time of Phantom Shares grant.

- Clear guidelines exist for how and when deferred amounts are distributed.

Looking for another form?

Form popularity

FAQ

A deferred compensation plan withholds a portion of an employee's pay until a specified date, usually retirement. The lump-sum owed to an employee in this type of plan is paid out on that date. Examples of deferred compensation plans include pensions, retirement plans, and employee stock options.

Deferred compensation plans are funded informally. There is essentially just a promise from the employer to pay the deferred funds, plus any investment earnings, to the employee at the time specified. In contrast, with a 401(k) a formally established account exists.

More In Retirement Plans A 457(b) plan's annual contributions and other additions (excluding earnings) to a participant's account cannot exceed the lesser of: 100% of the participant's includible compensation, or. the elective deferral limit ($19,500 in 2020 and in 2021).

The 457(b) deferred compensation plan is a retirement plan offered by the State of Florida, created to allow public employees like you to put aside money from each paycheck toward retirement.Here are some frequently asked questions about deferred comp plans: What sets a 457(b) apart from other retirement plans?

The amount you can defer (including pre-tax and Roth contributions) to all your plans (not including 457(b) plans) is $19,500 in 2020 and in 2021 ($19,000 in 2019).

Money saved in a 457 plan is designed for retirement, but unlike 401(k) and 403(b) plans, you can take a withdrawal from the 457 without penalty before you are 59 and a half years old.There is no penalty for an early withdrawal, but be prepared to pay income tax on any money you withdraw from a 457 plan (at any age).

Examples of deferred compensation include retirement, pension, deferred savings and stock-option plans offered by employers. In many cases, you do not pay any taxes on the deferred income until you receive it as payment. Deferred compensation plans come in two types qualified and non-qualified.

If your deferred compensation comes as a lump sum, one way to mitigate the tax impact is to "bunch" other tax deductions in the year you receive the money. "Taxpayers often have some flexibility on when they can pay certain deductible expenses, such as charitable contributions or real estate taxes," Walters says.

You can take the distribution in a lump sum or regular installments, paying tax when you receive the income. You can also arrange to withdraw some of it when you anticipate a need, such as paying for your kids' college tuition. While the IRS has few restrictions, your employer will probably have their own rules.