Information Sheet - When are Entertainment Expenses Deductible and Reimbursable

About this form

This form, titled "Information Sheet - When are Entertainment Expenses Deductible and Reimbursable," is a comprehensive guide that outlines the circumstances under which entertainment expenses can be claimed as deductions or reimbursed. It differs from similar forms by specifically targeting the deductibility of entertainment costs in various business contexts, providing clarity for businesses and individuals alike.

Main sections of this form

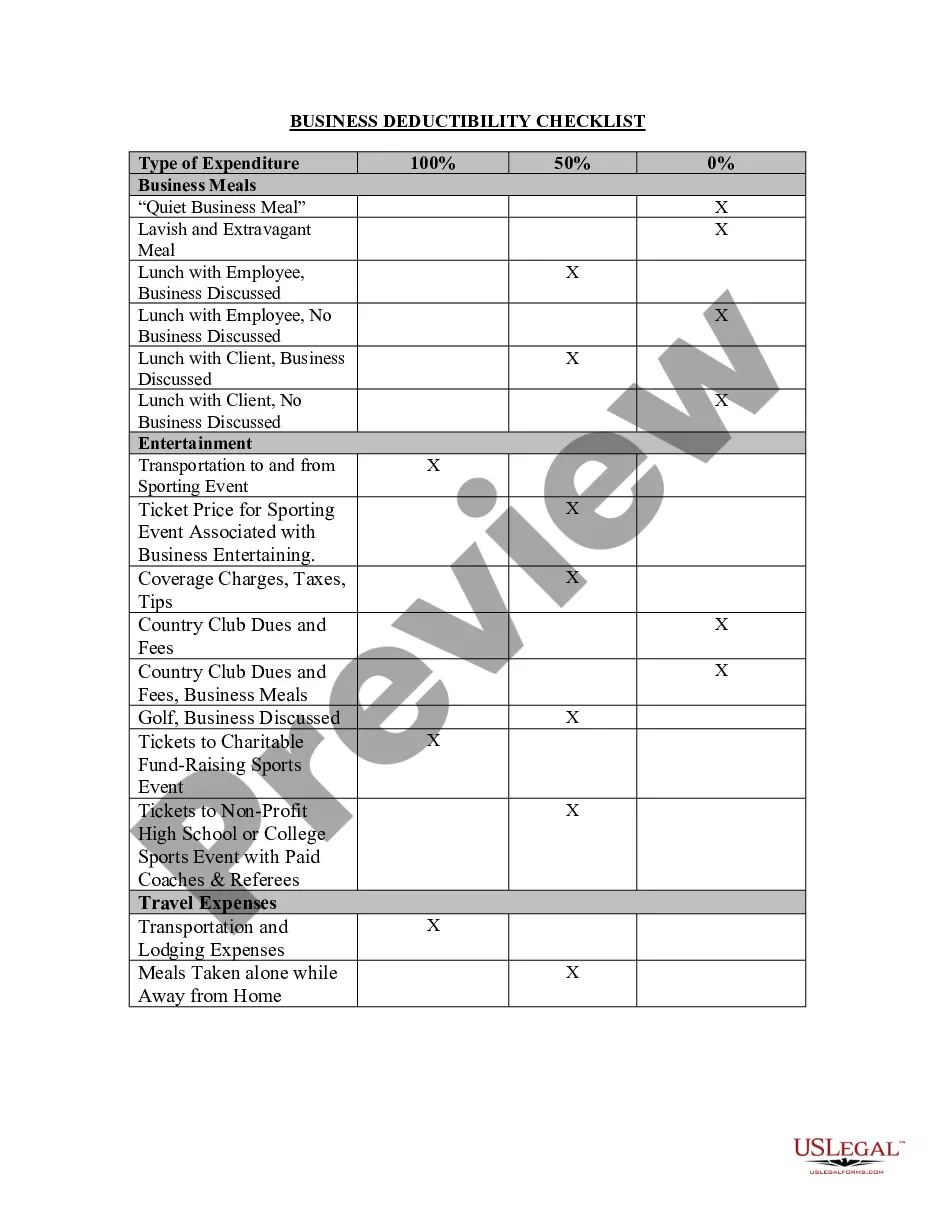

- Definition of entertainment expenses and how they generally apply in business contexts.

- Explanation of what constitutes ordinary and necessary expenses for deductibility.

- Details on the Directly-Related Test and Associated Test to determine if expenses can be deducted.

- Important rules regarding lavish or extravagant expenditures, and the limitations on reimbursed entertainment costs.

- Information on potential pitfalls when claiming these expenses.

When to use this document

This information sheet should be used when businesses seek to understand the specific conditions under which they can treat entertainment expenses as deductible or reimbursable. It is particularly useful during tax preparation or financial audits when clarity on expense categorization is crucial.

Who this form is for

- Business owners looking to optimize their tax deductions related to entertainment expenses.

- Accountants and tax professionals assisting clients with expense categorizations.

- Employees responsible for submitting expense reports related to client entertainment.

How to complete this form

- Read the definitions of entertainment and ordinary/necessary expenses carefully.

- Assess whether your entertainment expense meets the criteria outlined in the Directly-Related Test.

- Consider the circumstances of the expense to ensure they are not deemed lavish or extravagant.

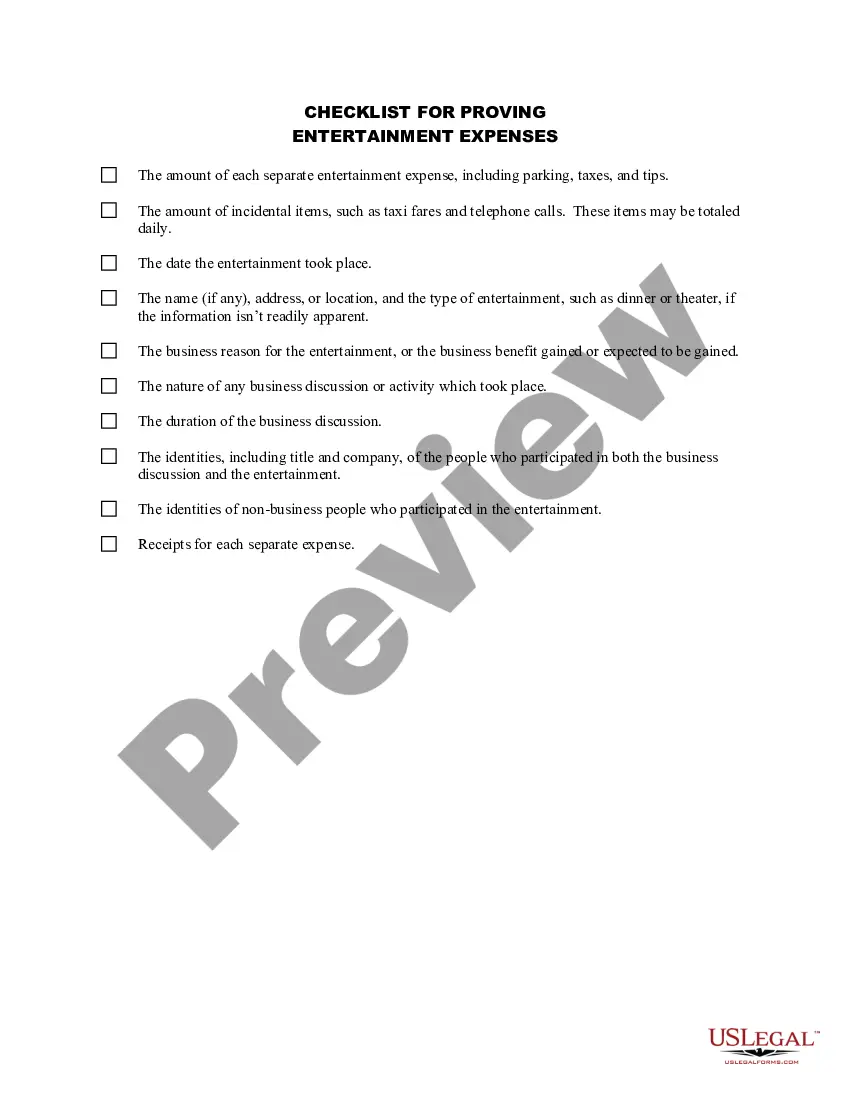

- Document your rationale for deducting or seeking reimbursement for the entertainment costs.

- Review relevant regulations to ensure compliance with both federal and state tax laws.

Notarization guidance

This form does not typically require notarization unless specified by local law.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Confusing personal entertainment costs with business-related ones.

- Failing to properly document the business purpose of the entertainment.

- Claiming expenses that exceed the prescribed limits without justification.

Advantages of online completion

- Immediate access to current legal guidance on entertainment expense deductibility.

- Easy-to-use format that can be saved and modified for individual business needs.

- Reliability from documents created by licensed attorneys knowledgeable in tax law.

Legal use & context

- The IRS requires clear documentation for claiming entertainment expenses.

- Entertainment expenses must pass specific tests to qualify for deductions.

- Employers should be aware of tax implications when reimbursing employees for entertainment costs.

- Non-compliance may lead to penalties or disallowed expense claims during audits.

Main things to remember

- Not all entertainment expenses are deductibleâspecific criteria must be met.

- Documentation is critical for substantiating entertainment deductions.

- Consulting a tax professional can provide clarity on complex situations.

Looking for another form?

Form popularity

FAQ

The allowable amount of meal and entertainment expenses you are allowed to deduct on your Schedule C is determined by the line of work you are in. For most taxpayers, the IRS allows you to deduct 50% of your business meals and entertainment expenses, including meals incurred while away from your home on business.

As a small business owner, you may entertain clients or customers. While this is often a business necessity, the costs can really add up. You'll be glad to know that the IRS allows you to take a deduction for 50 percent of your qualifying business meal entertainment expenses.

With the ratification of the 2018 Tax Cuts and Jobs Act, you can now only deduct the cost of meals and beverages; any other costs associated with entertaining are no longer deductible. That means you cannot deduct the price of concert tickets, rounds of golf and other activities you may use to schmooze clients.

Although entertainment expenses cannot be offset against your company's Corporation Tax bill, they are a legitimate business expense and represent a more tax-efficient way of paying for entertainment costs than using your personal post-tax income.

The IRS on Wednesday issued final regulations (T.D. 9925) implementing provisions of the law known as the Tax Cuts and Jobs Act (TCJA), P.L. 115-97, that disallow a business deduction for most entertainment expenses.Issued on Meal and Entertainment Expense Deductions, JofA, Feb. 24, 2020).

Your business can deduct 100% of food, beverage, and entertainment expenses incurred for recreational, social, or similar activities that are incurred primarily for the benefit of employees other than certain highly compensated employees (for example, food and beverages and entertainment at company picnics or company

Entertainment allowance is fully taxable for all private sector employees. However, government employees are eligible for exemption if the allowance is included in the gross salary.

Under the new tax law, businesses can't deduct most entertainment expenses anymore. Businesses will be impacted in a number of ways this year under the Tax Cuts and Jobs Act, which lowers individual and corporate tax rates, among other revisions.