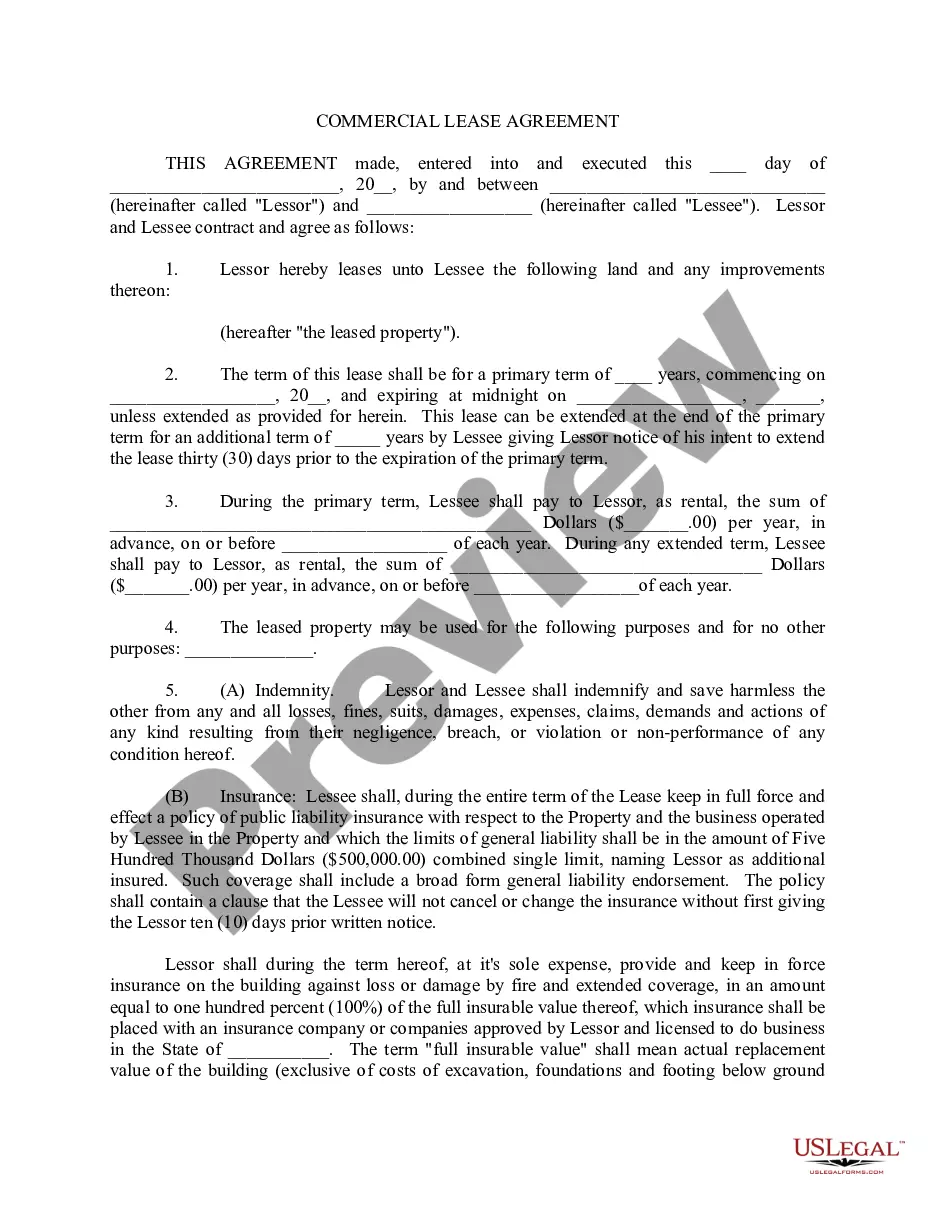

Tenant Improvement Allowance Accounting For Lessor

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The accounting rules for leasehold improvements stipulate that these costs must be capitalized rather than expensed immediately. Under tenant improvement allowance accounting for lessor, these assets are depreciated according to their useful life or the term of the associated lease. It is crucial to follow GAAP guidelines and stay updated with any changes in regulations. For accurate and efficient management, platforms like USLegalForms offer resources and tools to assist you in adhering to these accounting rules.

Leasehold improvements are recorded as long-term assets on the balance sheet. In tenant improvement allowance accounting for lessor, these costs should be capitalized and amortized over the lease term or the life of the improvement. This method reflects the usage of the asset over time and helps maintain accurate financial statements. Utilizing accounting software can simplify this recording process and ensure compliance with regulations.

Leasehold improvements for the lessor refer to alterations made to a rental property to meet the needs of a tenant. These improvements can include installation of new fixtures, walls, or electrical systems. It is important to understand tenant improvement allowance accounting for lessor, as these enhancements can impact the value of the property and the lease agreement. These improvements often help attract and retain tenants, creating a win-win situation for both parties.

Leasehold improvements should be properly classified as assets on the balance sheet. For tenant improvement allowance accounting for lessor, these improvements are typically capitalized and depreciated over the useful life of the asset or the remaining lease term, whichever is shorter. This ensures accurate financial reporting and compliance with accounting standards. Always consult with an accounting professional to ensure proper treatment specific to your situation.

In FRS 102, lease incentives must be accounted for as a reduction in income over the lease period. The lessor should spread the value of the incentives across the remaining lease duration to reflect a fair representation of income. By integrating tenant improvement allowance accounting for lessor, you maintain clarity and accuracy in your financial reporting.

A lessor accounts for a lease by recognizing the lease income over the term of the lease. They must record the leased asset on their balance sheet initially and track any accrued income. Following the guidelines for tenant improvement allowance accounting for lessor, the lessor adjusts the income recognized based on any lease incentives provided to the lessee.

To report tenant improvement allowance, you should include it in your financial statements as part of your lease agreement disclosures. This information will facilitate transparency about financing arrangements and lease incentives. Use a systematic approach to tenant improvement allowance accounting for lessor to ensure thorough and accurate reporting.

A lessor typically accounts for leasehold improvements by capitalizing the costs and depreciating them over the useful life. This approach aligns with tenant improvement allowance accounting for lessor, promoting accurate reporting. It is important to track these costs to maintain a clear financial overview and comply with accounting principles.

Tenant improvement allowance should generally be recorded in the balance sheet as a deferred liability or in the asset section, depending on the nature of the arrangement. Recording it properly ensures accurate representation in financial statements, helping both lessors and lessees understand their financial obligations clearly. Correct tenant improvement allowance accounting for lessor aids in compliance with accounting standards.

Lessors should recognize lease incentives as a reduction in rental income over the lease term. This accounting treatment aligns with tenant improvement allowance accounting for lessor, providing transparency in financial statements. By spreading out the incentive, lessors can give a clearer picture of their income and expense over time.