Partnership Interest

What is this form?

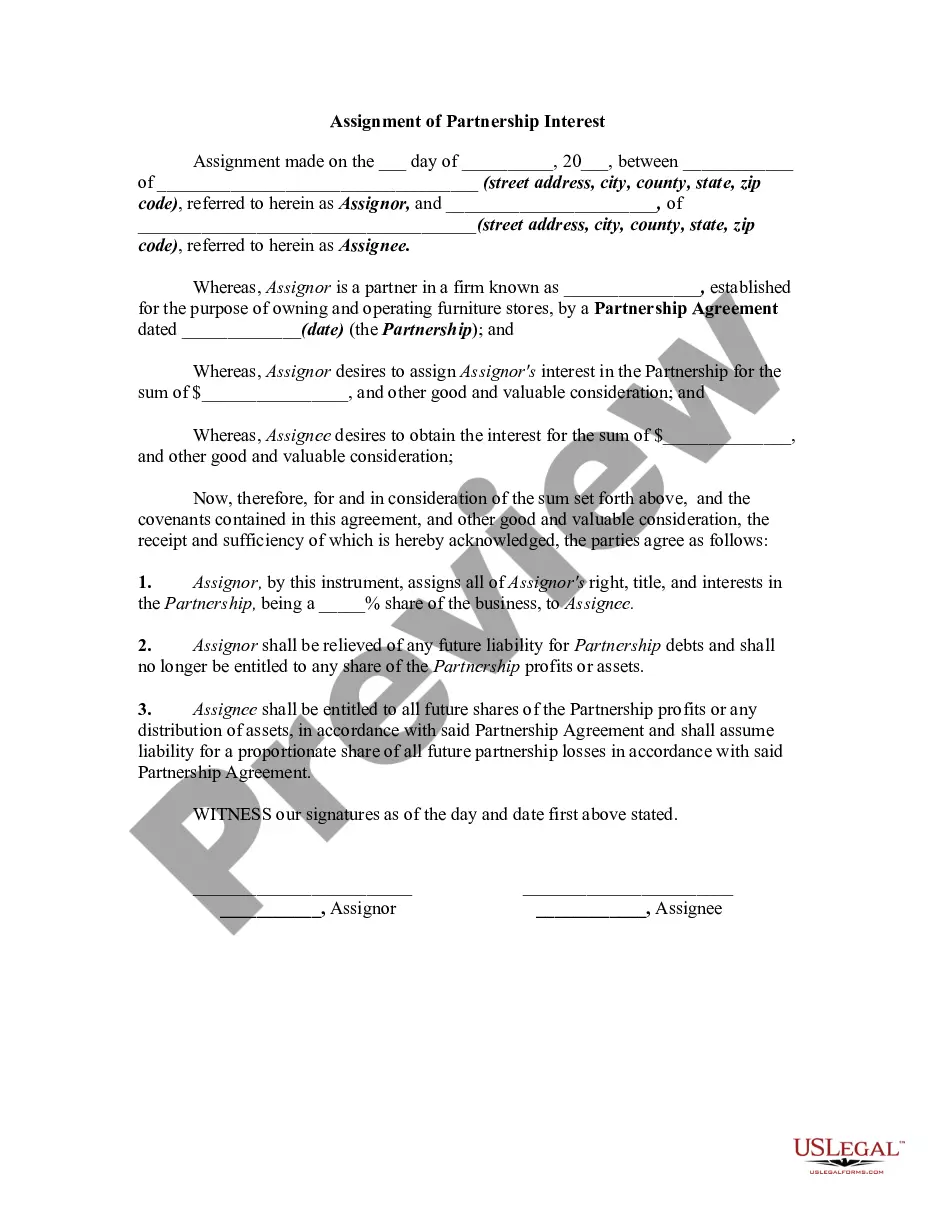

The Partnership Interest form is a legal document that facilitates the assignment of a partner's interest in a partnership to another party. This form is essential for legally transferring partnership rights and responsibilities, allowing the assignor to be relieved of future partnership liabilities. Unlike other partnership agreements, this form specifically addresses the transfer of ownership interests between partners.

Form components explained

- Details of the assignor and assignee, including addresses.

- A description of the partnership and the assignment terms.

- Specific percentage of interest being assigned.

- Relief from future liabilities for the assignor.

- Entitlements of the assignee regarding partnership profits and losses.

When to use this form

This form is used when a partner in a law firm or any other type of partnership wishes to transfer their partnership interest to another person. It is applicable in situations such as retirement, engaging in another business venture, or altering partnership dynamics. By using this form, both parties can ensure that liabilities and profit distributions are clearly defined.

Intended users of this form

- Partners in a law firm looking to sell or transfer their partnership interest.

- Individuals seeking to acquire a share of a partnership.

- Law firms wanting to outline the terms of partnership interest assignments.

Instructions for completing this form

- Identify the parties involved by filling in the names and addresses of the assignor and assignee.

- Specify the name of the partnership and the relevant details about the business.

- Indicate the percentage of the partnership interest being assigned.

- Enter the consideration amount and payment terms agreed upon between the parties.

- Obtain the necessary signatures from both the assignor and assignee, along with the endorsement of remaining partners.

Does this form need to be notarized?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to clearly state the percentage of interest being assigned.

- Not including the signatures of remaining partners, which may invalidate the agreement.

- Omitting or incorrectly filling out the terms of consideration.

Benefits of completing this form online

- Convenient access to legal documents from anywhere, without the need for in-person visits.

- Editable templates allow for customization to fit specific needs.

- Reliability of professionally drafted legal forms ensures adherence to legal standards.

Main things to remember

- The Partnership Interest form is essential for legally transferring partnership rights.

- Be clear about terms to avoid conflicts regarding liabilities and profit distributions.

- Always check local laws for any specific requirements related to partnership assignments.

Looking for another form?

Form popularity

FAQ

A transfer of partnership interest happens when a business partner relinquishes their ownership rights and responsibilities to another individual or company.

The securities laws define security to include an investment contract and general partnership interest could be considered an investment contract.

Transfer of interest or we can say ownership is possible in case of business as you can transfer your business to any other person with some legal formalities, if applicable. On the other hand, in case of profession, you can not transfer your professional certificate to someone else.

If a partner's entire interest in a partnership is liquidated or redeemed, he or she recognizes gain to the extent any money or marketable securities received exceeds his or her basis in the partnership interest immediately before the distribution ( Code Sec.

A partner's interest in a partnership is considered personal property that may be assigned to other persons. In addition, an assignment of the partner's interest does not give the assignee any right to participate in the management of the partnership.

The federal income tax rules for partnership payments to buy out an exiting partner's interest are tricky, but they also open up tax planning opportunities. Payments made by a partnership to liquidate (or buy out) an exiting partner's entire interest are covered by Section 736 of the Internal Revenue Code.

A partner can transfer his interest so as to substitute the transferee in his place as the partner, without the consent of all the other partners; a member of company cannot transfer his share to any one he likes.

The gift of a partnership interest generally does not result in the recognition of gain or loss by the donor or the donee. A gift is, however, subject to gift tax unless the gift qualifies for the annual gift tax exclusion or reduces the donor's lifetime gift tax applicable exclusion amount.