Credit and Your Consumer Rights

Understanding this form

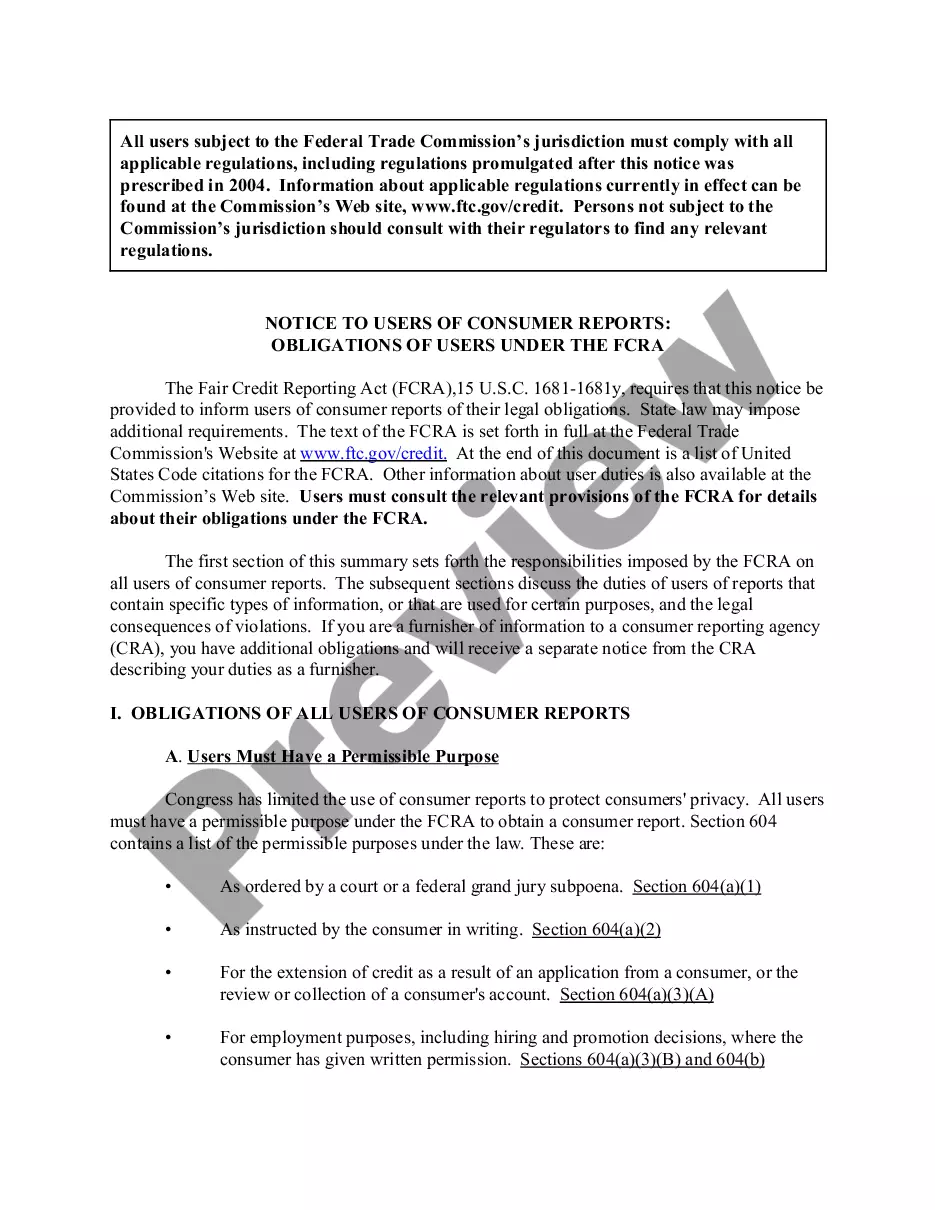

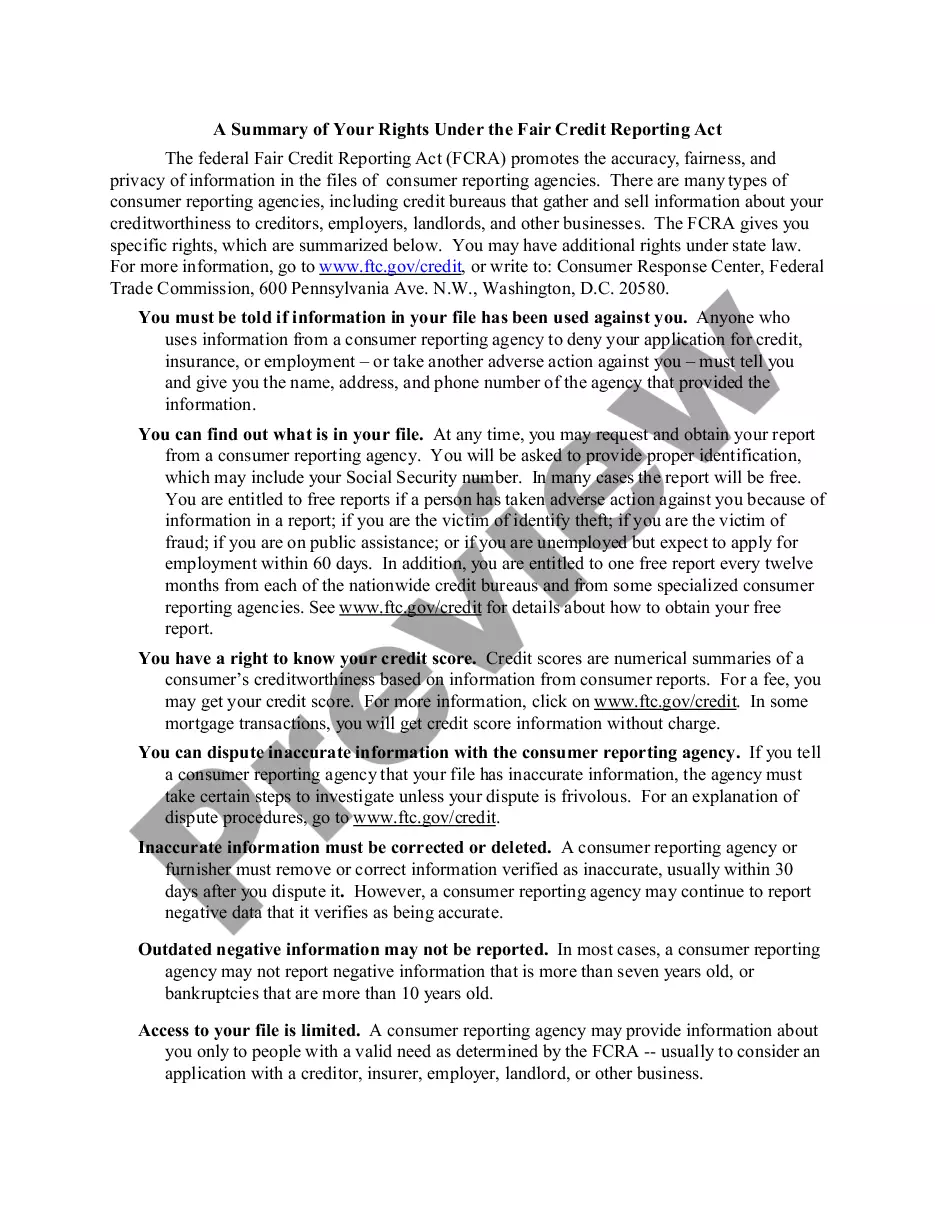

The "Credit and Your Consumer Rights" form provides individuals with essential information about their rights related to credit, as outlined by the Federal Trade Commission. This form helps you understand your rights and protections when dealing with credit reporting agencies and creditors. Unlike other credit-related forms, this one specifically focuses on consumer rights and the legal protections you have under various laws, such as the Fair Credit Reporting Act and the Fair Debt Collection Practices Act.

Main sections of this form

- Overview of your credit report and rights to access it.

- Explanation of the Equal Credit Opportunity Act and protections against discrimination.

- Guidelines for disputing inaccuracies in your credit report.

- Debt collection rights under the Fair Debt Collection Practices Act.

- Strategies for resolving credit issues and managing your debts.

Common use cases

This form is beneficial in various situations, such as when you wish to understand your rights related to credit reporting, experience issues with inaccurate information on your credit report, face discrimination when applying for credit, or wish to dispute charges or errors in credit billing statements. It serves as a comprehensive guide to navigating credit-related challenges effectively.

Who this form is for

- Consumers concerned about their credit reports and ratings.

- Individuals facing credit issues or disputes.

- People applying for credit, insurance, or employment who want to understand their rights.

- Those dealing with debt collectors and seeking to understand their consumer rights.

Instructions for completing this form

- Review the information carefully to understand your rights regarding credit reporting and debt collection.

- Identify any specific credit issues you are facing that require action or dispute.

- Gather documentation, such as credit reports and statements, to support any claims or disputes.

- Follow the guidelines provided to dispute inaccuracies or discrepancies.

- Contact creditors or credit reporting agencies as necessary, using the information outlined in the form.

Is notarization required?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Ignoring errors on credit reports instead of actively disputing them.

- Failing to request free credit reports annually as allowed under federal law.

- Not understanding the details of adverse action notices from creditors.

- Overlooking timelines for disputing inaccuracies or errors.

Advantages of online completion

- Easy access to accurate and comprehensive information from the Federal Trade Commission.

- Convenient download options for personal records and future reference.

- The ability to stay informed about consumer rights and protections.

- Access to practical tips for managing credit issues effectively.

Key takeaways

- Understand your rights regarding credit reporting and debt collection.

- Utilize available resources to dispute inaccuracies on your credit report.

- Be aware of protections against discriminatory practices in credit applications.

- Stay proactive in resolving credit-related issues to maintain financial health.

Looking for another form?

Form popularity

FAQ

Credit reports will exclude medical debt collections under $500. Starting January 1, 2023, the consumer credit-reporting bureaus ? Equifax, Experian, and TransUnion ? will no longer add medical debt less than $500 to credit reports. Amounts of $500 or more may still show up and can impact your credit score.

On Tuesday, the three major credit bureaus ? Equifax, Experian, and TransUnion ? announced that medical collections with balances of $500 or less would no longer appear on consumer credit reports.

As of November 30, 2021, an amendment to Regulation F, which implements the FDCPA, says that a debt collector can't report a debt to the three major credit reporting agencies, Equifax, Experian, and TransUnion, before first contacting the consumer. The debt collector must: speak to the consumer in person or by phone or.

Refrain from reporting old credit information, usually more than seven to ten years old. limit disclosure of your credit file to third parties who have a legitimate need, such as a creditor, landlord, or employer, and. withhold disclosure of your credit information to employers unless you consent.

The applicable laws include the Truth in Lending Act, the Fair Credit Reporting Act, the Equal Credit Opportunity Act, the Fair Credit Billing Act, the Fair Debt Collection Practices Act, the Electronic Funds Transfer Act, and the Fair and Accurate Credit Transactions Act.

They have also taken steps to remove all medical collections under $500. This last step went into effect on April 11, 2023, and with this change, it's estimated that roughly half of those with medical debt on their reports will have it removed from their credit history.

Consumer Credit and the Removal of Medical Collections from Credit Reports. The three nationwide consumer reporting companies announced the removal of medical collections under $500 from consumer credit reports on April 11, 2023.

Fair Credit Billing Act This amendment allows consumers to dispute credit card errors. It also requires lenders to provide credit card statements at least 21 days before payments are due to give you the opportunity to review your credit card statement and dispute any errors.